Listen to the audio version of this article (generated by AI).

Key Points

- Micron’s record-breaking earnings reaffirmed that AI spending remains strong, lifting semiconductor stocks and underscoring the importance of high-bandwidth memory in AI infrastructure.

- A global memory shortage has given Micron significant pricing power, with production sold out into 2027 and long-term contracts securing future revenue.

- Despite short-term volatility tied to higher consumer-electronics prices, Micron’s dominant position in AI memory makes it a key player shaping the future of the semiconductor industry.

Micron Technology (MU) may have become the world’s most important technology company following its June 24 blowout earnings report.

No, it’s not the richest tech business. There are nine pure technology businesses with market capitalizations higher than Micron’s $1.304 trillion (as of midday June 30).

And Micron’s nearly $1,156 stock price isn’t even the highest within the memory sector. Sandisk (SNDK), at roughly $2,090 per share, nearly doubles Micron’s price.

But Micron essentially controls the entire memory industry – and arguably the artificial-intelligence (“AI”) industry as well – because of the simplest principle in economics… supply and demand.

Right now, high-bandwidth memory (“HBM”) is the most important piece of the larger AI puzzle, and it continues to transform and dominate the markets.

Why? Because it’s the bottleneck. Every tech company with its hands in AI (which is most of them) needs massive amounts of HBM to build its components or run its data centers.

Except there’s not enough memory to go around, thus the bottleneck. And that limited supply gives Micron and other memory manufacturers all the leverage they need to control pricing and dictate the market.

Given that Micron is the only major American memory producer able to compete on the world stage with the likes of South Korean memory giants Samsung Electronics and SK Hynix, it wields considerable pricing and supply power, capable of bringing the entire AI and tech industries to their knees. And last week’s earnings news illustrated why.

Micron’s Blowout Earnings Helped Lift Chip Stocks

Micron reported its fiscal third-quarter 2026 earnings last Wednesday. The impact on the market was immediate.

Not only did its own stock price surge 16% higher the next day, but the blowout results also elevated chip stocks – which had just suffered a huge sell-off – such as Intel (INTC), Advanced Micro Devices (AMD), Marvell Technology (MRVL), and Qualcomm (QCOM), which all saw modest increases. Nvidia (NVDA) didn’t enjoy the same bump (its stock dipped roughly 1.6% the following day), but the chip bellwether is poised to benefit from Micron’s success as well.

How exactly does Micron’s earnings report benefit these chipmakers? Besides Qualcomm, each of those companies integrates Micron’s HBM into their AI accelerators. So, when Micron is breaking revenue records, it’s because the company is delivering the memory the chipmakers need to make their products and sell them to data centers.

Plus, Micron’s outstanding quarter showed the world that AI spending is still hitting record levels. That helped calm recent investor fears that the AI boom was about to go bust.

Here are some of the many highlights of Micron’s fiscal third-quarter earnings call:

- The company’s $41.5 billion in revenue was a 74% quarter-over-quarter gain and a year-over-year gain of 346%.

- Net income grew by 1,398% year over year, from $1.89 billion to $28.24 billion.

- Dynamic random-access memory (“DRAM”) drove the quarter, with $31.3 billion in sales, which accounted for 76% of the quarter’s revenue. NAND flash memory sales totaled $9.9 billion.

- Micron’s Cloud Memory Business Unit (“CMBU”) earned a record $13.8 billion during the third quarter and represented one-third of the company’s total revenue. CMBU gross margins were 83%.

- The company’s Core Data Center Business Unit (“CDBU”) also set a company record with $11.5 billion in revenue and staggering 87% gross margins. Micron’s Mobile and Client Business Unit (“MCBU”) put up identical revenue and gross margin numbers to CDBU as well.

- Even Micron’s Automotive and Embedded Business Unit (“AEBU”) set a record, with $4.6 billion in revenue, accounting for 11% of total company revenue.

Other numbers of note include an 84.9% overall gross margin, $33.68 billion in operating income, $28.86 billion in non-GAAP (generally accepted accounting principles) net income, $25.39 billion in GAAP cash from operations, $25.11 diluted earnings per share (“EPS”), $25.4 billion in cash flow from operations, and $18.3 billion in free cash flow.

Wow. Just wow.

And Micron’s fourth-quarter projections are even more encouraging: roughly $50 billion in revenue, 86% gross margin, and a $31 diluted EPS. Plus, Micron expects its fourth-quarter free cash flow to increase “substantially” and that, “over time,” it will return 100% of its excess cash to shareholders.

With this earnings report, Micron proved that AI is alive and kicking and that its memory products are likely to remain in extremely high demand. And the company proved just how influential it is on the entire market, which has essentially been following its lead.

Memory Shortage: A Double-Edged Sword for the Tech Industry

There’s no doubt that the shortage of HBM for AI and data centers has benefited Micron. In fact, the company has already sold out its entire HBM production capacity through 2026 and into 2027 under multiyear, fixed contracts. And Micron is only able to fulfill roughly half to two-thirds of demand for certain key customers.

As companies like Micron, Samsung, and SK Hynix shift their priorities toward producing the HBM that data centers require to operate, attention moves away from the more consumer-focused DRAM and NAND, resulting in reduced production. In late 2025, Micron decided to leave the consumer market altogether and decrease production of its Crucial-branded solid-state drives and RAM kits.

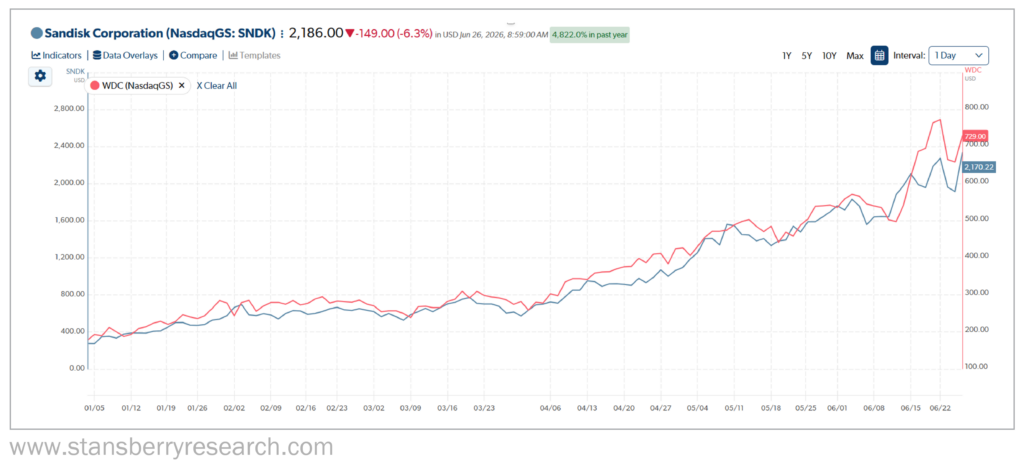

But that demand for HBM – as well as the resulting shift away from consumer memory production – has trickled down to makers of other types of memory, such as Sandisk and Western Digital (WDC).

During Micron’s earnings call on June 24, CEO Sanjay Mehrotra said:

We expect tight conditions to persist beyond calendar [year] 2027 as a result of AI-driven demand across all segments coupled with structural supply constraints… Even as we expect industry supply to improve gradually in 2028, we currently do not have line of sight as to when memory supply will be able to catch up with increasing demand.

Mehrotra’s statement is great news for memory manufacturers. But it’s bad news for the consumer-electronics industry and cash-strapped customers because companies are now paying more for the limited supply of DRAM and NAND memory they need to build their products.

TrendForce’s second-quarter memory forecast projected that DRAM memory contract prices would rise 58% to 63% in the second quarter of 2026 over the previous quarter. The forecast for NAND memory contract prices was a 70% to 75% increase over the previous quarter.

We’re watching that happen in real time.

On June 25, Apple (AAPL) raised the prices of its MacBook Air laptop by $200, its MacBook Pro by $300, the MacBook Neo by $100, iPad Air by $150, and iPad Pro by $200. And Microsoft (MSFT) increased its Xbox game console prices by $100 to $150.

All because of the limited supply and corresponding price surges in memory.

The limited supply and resulting demand directly benefit companies like Sandisk and Western Digital. Not coincidentally, their stock prices have soared on a nearly identical trajectory since the start of the year.

Memory manufacturers are reaping the benefits of AI’s demand. But the companies paying for that memory – if they can even secure it – aren’t quite as fortunate.

Memory Stocks Tumble After Apple and Microsoft Price Increases

The market can turn on a dime. That’s exactly what happened on Friday, June 26, when SK Hynix and Samsung almost singlehandedly tanked the Korean KOSPI index, dropping 8.4% and 5.3%, respectively. The overall KOSPI lost as much as 8% at one point that day.

That led to Micron falling by nearly 7% between Thursday and Friday, one day after it skyrocketed 16% higher. The chart below illustrates exactly when Micron fell off a small cliff on Friday morning.

Why the sudden plunge? Investors and analysts get antsy – almost to the point of paranoia. It’s understandable, since there is an ungodly amount of money at stake.

But it basically boiled down to this: Apple and Microsoft raised their prices in reaction to the soaring cost of the memory their devices need. Those elevated prices spooked investors and analysts, who feared consumers would not buy those devices at higher price points. That sparked concerns about potential lagging demand for memory. After all, if devices aren’t selling, there wouldn’t be as great a need to make so many of them.

Also, how would the memory makers’ customers (the Apples and Microsofts of the world) react to the price hikes knowing they’d have to pass them on to their own customers? Would the relationships sour?

These are among the many things analysts and investors consider, and the drop in memory stock on Friday, June 26 was a direct reflection of that. Overall, the Roundhill Memory ETF (DRAM) – of which 75% of holdings comprise Micron, Samsung, and SK Hynix – stumbled 6.52% lower, accordingly.

Of course, this is probably a minor blip in the bigger picture. Case in point: After dropping 6.1% on Thursday following the price-hike news, Apple rallied on Friday, closing 3.1% higher than the previous day.

Yes, price hikes are concerning and could have long-term implications. But Micron has its HBM business to fall back on – and that’s not going anywhere anytime soon.

AI Demand Keeps Micron in Control of the Market

No stock is bulletproof, especially in the notoriously volatile tech and AI sectors. But Micron is pretty darn close.

Back in April, I wrote an article suggesting Micron could hit $1,000. It blew past that mark on June 1 and climbed as high as $1,255 on June 25.

In late May, I posed the question as to whether Micron could reach $2,500 per share. Bold? Yes. Way off base? It certainly doesn’t seem like it, based on analysts’ most recent price-target adjustments.

On June 25:

- Raymond James Financial increased its target from $1,100 to $1,500.

- RBC Capital raised its price target from $1,200 to $1,500.

- JPMorgan Chase went up to $1,540 from $550.

- KeyBanc’s price target jumped from $600 to $1,600.

- Susquehanna elevated its price target from $1,750 to $2,000.

Micron reaching that $2,500 price I wrote about in May suddenly seems more attainable – especially considering not only its outstanding financials, but also what’s still coming its way.

During the third-quarter earnings call, CEO Mehrotra made the following announcement:

We are excited to announce that we have now signed 16 strategic customer agreements, or SCAs, which we expect will fundamentally transform our business model…

Fourteen of the 16 SCAs that we have signed have a cumulative revenue at minimum price per our contracts of approximately $100 billion over the remaining agreement term… Under the SCAs we have signed so far, we project to receive cash deposits and related financial commitments of $22 billion.

Even with current memory scarcity, Micron is pledging to supply its customers over the next several years under fixed contracts. That’s just smart business. And it guarantees the company hundreds of billions of dollars in revenue for the foreseeable future.

Micron’s stock has reacted positively. The 818% growth it has experienced over the past year is exceptional.

And considering its stranglehold on the American memory industry, as well as its significant backlog, and exceptional earnings, Micron’s steady climb should continue well into the future. That makes Micron arguably the most important tech company in America, if not the world.

Regards,

David Engle

Editor’s Note: Should investors prepare for an AI crash or buy the dips? Analyst and True Wealth editor Brett Eversole just posted a surprising answer. According to Brett’s research, there’s a pattern taking shape that could defy all the worst predictions about a bust. He’s calling it a Melt Up Tsunami. And he’s identified at least a half-dozen stocks that could benefit, including his #1 stock to own right now. He shares the ticker in this new presentation.