A year ago, the “SanDisk” brand was better known for the kinds of products you buy at a Best Buy on a whim … a memory card brand, not a market-melting AI stock.

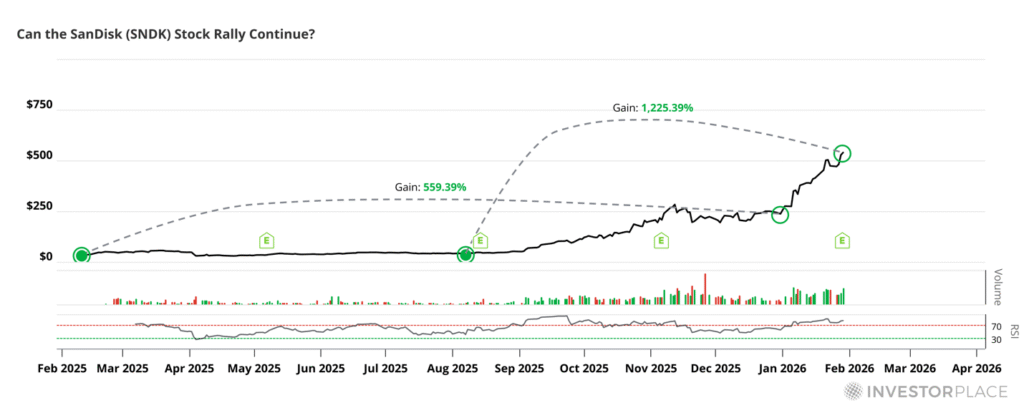

Then Wall Street watched that “boring” storage name turn into a full-blown superstock. In 2025, SanDisk (SNDK) delivered a jaw-dropping 559% return, the best performance in the S&P 500. And from its post–spin-off debut near $36 to a recent close above $500, the newly independent company has not just doubled or tripled …it’s surged well over 1,000% at its peak.

So what happened?

One answer explains nearly everything: If there’s no memory, there’s no AI.

Just like that, “storage” stopped being a commodity and started looking like the next bottleneck in the AI supply chain.

Why Is SanDisk Stock Soaring?

Because AI data centers are eating through flash memory at a time when supply is tight, pushing NAND prices higher. That pricing squeeze is sending SanDisk stock soaring on the back of record earnings momentum.

That’s the simple version, and it’s the one most investors missed until the stock was already up 10x.

The longer version tells the tale of a “perfect storm” forming in the memory market:

- AI demand surged, especially from hyperscale data centers that require massive pools of fast storage for model training and, increasingly, inference workloads.

- NAND flash supply tightened after years of industry belt-tightening and cautious capacity expansion, creating meaningful pricing power for suppliers.

Put those together and you get what markets love most: scarcity plus necessity with pricing power as the result.

SNDK Stock: Record-Breaking Performance That’s Hard to Ignore

SanDisk stock isn’t merely trending higher … it’s “mooning” like a meme stock, but with real fundamentals underneath the move.

At its peak, SanDisk was up roughly 1,600% from its February 2025 spin-off price. Even after that run, analysts are still slapping major targets on SNDK shares, including a price target as high as $1,000.

This is not just happening to SanDisk stock either. Memory and storage stocks across the board have caught fire, a sign this isn’t a single-stock mania so much as a broader repricing of “data infrastructure” in the AI era.

Even Micron (MU), long viewed as a classic cyclical, has seen margins explode during the recent memory upswing, with reports noting gross margin jumping from ~38% to ~56%. Yet SanDisk stands out as the clearest “poster child” of the memory “supercycle” theme.

No AI Boom Without Memory Infrastructure

Contrary to popular belief, AI isn’t just about compute … it’s compute, data, and the ability to move and store that data fast enough to be useful.

Training frontier models requires massive datasets. But the next phase – deploying AI everywhere – can be even more storage-hungry in a different way, because inference at scale creates relentless demand for fast, accessible “working memory.”

At CES 2026, Nvidia (NVDA) CEO Jensen Huang put it bluntly, calling storage a “completely unserved market” and suggesting it could become “the largest storage market in the world.” In his view, storage would effectively holdthe working memory of the world’s AIs.

Nvidia isn’t just flapping its gums, either. It has announced infrastructure aimed directly at “context memory” for inference … a clue that the industry is treating storage as a first-class AI bottleneck.

That’s the key idea: When the plumbing behind a megatrend becomes a strategic component, the suppliers don’t get paid like suppliers anymore … they get paid like what they are: critical infrastructure.

Why Data Deluge Is a Lasting Trend for SanDisk Stock

The big question for SNDK stockholders and prospective buyers is: Could this be hype?

Sure, some of it always is.

But the bigger driver isn’t hype … it’s that the physical world is generating and consuming more data every year, and AI is accelerating that curve.

- IDC projects AI infrastructure spending, including compute and storage, could reach $758 billion by 2029, underscoring the scale of the buildout.

- JLL expects nearly 100 GW of new data center capacity to be added between 2026 and 2030, effectively doubling the sector’s size over that period.

If the industry is literally doubling data center capacity, it follows that the world will need more memory and storage, not less.

The real question for SNDK stockholders is not “will demand grow?” but “how smooth will that growth be?” and “how quickly will supply respond?”

Which brings us to the other half of SanDisk’s rocket ride …

NAND Flash Shortage: The Perfect Storm for Prices

Memory is famous for cycles, whipsawing between “too much supply” and “not enough,” with pricing swinging violently in response.

What’s unusual about SanDisk’s surge is not the cycle itself, but the timing.

After a brutal downturn in 2022–2023, memory producers slashed capex and constrained output. When inventories finally normalized, supply tightened just as AI demand exploded, creating a textbook supply-demand imbalance.

TrendForce data showed NAND wafer contract prices jumping more than 60% in November 2025 alone, as hyperscaler demand collided with constrained supply.

SanDisk has aggressively leaned into that environment. Reports indicate it raised NAND contract prices by roughly 50%in late 2025. Some high-capacity enterprise NAND products are now expected to double in price in early 2026.

One industry CEO warned that NAND prices have already more than doubled and that tightness could persist into 2027. According to that warning, much of 2026 production is already spoken for.

This is what turns a “commodity” business into a profit engine:

You don’t need to ship dramatically more units. You need pricing power on something customers can’t do without.

In its latest quarter, SanDisk’s profit surged to $803 million, up from $104 million a year earlier. Adjusted EPS hit $6.20, while revenue climbed to $3.03 billion. Forward guidance pointed to another step-change higher. That’s what a shortage looks like in income-statement form.

Even more telling, SanDisk is now pursuing multi-year contracts with firmer pricing, signaling confidence that today’s tight market can translate into longer-lived economics rather than a one-quarter windfall.

That’s not a move you make if you think the cycle is about to roll over quickly.

What Could Go Wrong? Will SanDisk Stock Crash?

SanDisk’s run has been spectacular. But spectacular booms often end in spectacular busts.

1) Memory Cycles: Oversupply Always Lurks

This is the classic risk, a shortage eventually turning into a glut.

If Samsung, SK Hynix/Solidigm, Micron, and others decide to chase market share and ramp capacity aggressively, NAND prices can fall fast.

SanDisk can’t fully control that.

2) AI Demand Could Normalize

AI isn’t going away. But growth rates can cool down.

Right now, spending is driven by a global infrastructure race, with data centers, GPU clusters, and inference deployments all being built out at once. If the market tightens its budget, or if efficiency improvements reduce storage required per workload, demand growth could slow. And markets hate deceleration when a stock is priced for perfection.

3) Competition and Tech Substitution

SanDisk stock is strong, but it’s not alone. Giants like Samsung can be ruthless when incentivized properly, and competition can intensify quickly if pricing attracts new capacity.

At the same time, the storage stack itself is evolving with new memory architectures for AI inference that could change how much “traditional NAND” is needed, or shift which vendors capture the best margins.

4) Valuation and Hype Risk

After a 10x-plus run, expectations are no longer reasonable; they are demanding. Even the bullish coverage has started to look like a “regime change” in action, with price targets pushed up dramatically higher, including the eye-popping $1,000 call.

That’s a double-edged sword:

- Great if results keep surprising upward

- Dangerous if SanDisk delivers merely “good” instead of “jaw-dropping” earnings

Bottom line: When a stock is crowded, the downside can be violent.

SanDisk’s Edge: Pricing Power, Market Position, and Tech Strengths

For all the macro tailwinds, SanDisk isn’t only riding the wave. It has structural strengths that help explain why it is leading the pack right now.

Take its cost advantage via the Kioxia JV partnership. SanDisk recently extended its joint venture arrangement with Kioxia, the former Toshiba memory business, through 2034, including a multi-year payment structure. This is a sign that both parties expect the manufacturing partnership to remain strategically valuable.

In a world where manufacturing scale and cost per bit determine survival, that kind of locked-in partnership can be an edge.

What’s more, SanDisk stock is flexing its market share muscle in a concentrated industry. The NAND industry is basically an oligopoly. TrendForce data for Q3 2025 shows Samsung leading NAND market share, followed by SK hynix/Solidigm, with Kioxia and SanDisk holding meaningful positions behind them.

In a tight market, being a large, strategically relevant supplier helps volume, but it also adds negotiating power.

SanDisk is also pushing high-end enterprise products tailored to data centers. For example, the company has highlighted its UltraQLC platform and previewed an ultra-high capacity 256TB NVMe enterprise SSD, exactly the kind of “dense storage” hyperscalers care about.

SanDisk’s game plan is to win on performance, density, and reliability where customers are least price sensitive.

All the above – scale, partnership economics, pure-play focus, and enterprise product strength – show up in one place: pricing power.

And pricing power is what turns a memory company from a “cyclical gamble” into an “AI infrastructure compounder,” at least for as long as the supply-and-demand imbalance lasts.

Is SanDisk Stock a Buy After This Epic Rally?

The bull case is straightforward:

- AI infrastructure spending is still ramping

- Storage is being redefined as a bottleneck in inference-era AI

- NAND supply looks constrained, with price spikes and long lead times still being reported

- SanDisk is attempting to lock in economics with firmer, longer contracts

If those conditions persist, SanDisk’s “meme stock” phase could keep going longer than most memory investors are conditioned to believe.

As for the bear case… after a 1,000%-plus move, the easy money is gone.

New buyers aren’t buying for a continuation of extraordinary conditions in a famously cyclical industry. If supply ramps up or demand cools down, the downside could hit SNDK stockholders hard.

When Wall Street starts floating $1,000 price targets, that usually calls for a pause and reevaluation.

Bottom Line: The Rally Can Continue … But Don’t Confuse “Possible” With “Sure Thing.”

Yes, SanDisk stock can keep running. There are real reasons for that, including rising AI-driven storage demand, tightening supply conditions, and SanDisk’s positioning as a scaled supplier with differentiated enterprise products that matter most to hyperscale customers.

But no stock goes straight up forever, especially not one tied to memory cycles. History is clear on that point. Periods of extreme pricing power tend to invite new supply, and when that balance shifts, sentiment can turn quickly.

For long-term investors, the most sensible stance is disciplined patience rather than blind optimism:

- Respect the theme (AI needs memory)

- Respect the cycle (memory booms can flip)

- And respect price (after a 10x run, valuation matters again)

If SanDisk stock sees a fear-driven pullback – the kind that convinces investors the story is broken, that may be exactly when the risk-reward starts to look attractive again.

In other words, SanDisk might not be a “chase it here” stock, but it could absolutely look more compelling on a sharp pullback as a “buy it on the dip” stock.

Editor’s Note: Which stock will the White House buy next?

Insiders in Washington have already bought massive stakes in three tiny resource firms, driving them up as much as 200% overnight. Now, the man who recommended MP Materials before the White House bought (making 100% for his followers) is naming the next stocks he believes the government will target. Get the names and tickers right here – free of charge.