Key Points

- The AI boom is creating a major memory and storage shortage, driving soaring demand for DRAM, NAND flash memory, SSDs, and hard disk drives while pushing consumer electronics prices higher.

- SanDisk, Western Digital, and Seagate Technology are benefiting from explosive AI infrastructure growth as hyperscalers and data centers race to secure high-capacity storage and memory solutions.

- With memory demand expected to remain elevated through 2026 and beyond, AI-focused memory and storage companies are emerging as key “pick-and-shovel” investment plays tied to the expansion of global data centers and AI infrastructure.

Micron Technology (MU) has made plenty of headlines this year… and understandably so.

On March 16, the memory chip giant announced that it had completed its $1.8 billion acquisition of a chipmaking plant in Taiwan from Powerchip Semiconductor Manufacturing, which I covered back in January.

But with that news came the announcement that Micron is planning to build another chipmaking facility on the same site. According to research firm TrendForce, this will increase Micron’s global capacity by roughly 10% starting around the second half of 2027.

But Micron isn’t the only AI memory stock worth watching right now – and the reason why has everything to do with demand.

The ability to increase memory production is critical, as the AI industry’s massive boom has led to a drastic demand for – and shortage of – memory… especially for consumer electronic devices like smartphones, gaming consoles, and laptops.

Not just AI memory chips either. Other types of memory and storage are needed – like hard disk drives (“HDDs”) and flash memory – to keep up with demand.

And that demand is fantastic news for memory tech manufacturers like SanDisk (SNDK), Western Digital (WDC), and Seagate Technology (STX).

Why AI Is Driving Memory and Storage Demand

The rise of AI has flipped technology on its head. As more businesses continue to adopt AI and fold it into their daily operations, the demand for AI increases.

And when that demand increases, so does the need for more expansive AI infrastructure.

That infrastructure primarily comes in the form of data centers, which are popping up across the globe in record numbers. Between 2026 and 2030, the worldwide data center sector is projected to expand at a 14% compound annual growth rate (“CAGR”).

All those data centers require tons of memory to operate. Not only the high-bandwidth memory (“HBM”) that delivers faster data transfer rates, consumes less power, and takes up less space than traditional double data rate (“DDR”) dynamic random-access memory (“DRAM”), however.

But also, that very DRAM, which data centers’ CPU-based servers need in mass quantities. In fact, the Wall Street Journal estimates that data centers will use more than 70% of all high-end DRAM production in 2026.

That’s great news for data center operators. Not so much for manufacturers and retailers of phones, tablets, laptops, and other consumer electronics that literally can’t operate without DRAM.

The AI-Driven Memory Shortage Is Raising Prices

With major memory tech companies focusing their capacity on HBM and higher-end DRAM, the production of consumer DRAM used for everyday electronics has decreased.

The combined demand for high-end DRAM for data centers and the limited supply of consumer DRAM are driving overall DRAM prices sky high… which points to the start of a new memory supercycle.

And this supercycle will raise consumer electronics prices and impact sales.

In January, TrendForce predicted that smartphone production would drop 7% for 2026… and that prices would rise for both Android and Apple phones. Gartner forecasts smartphone shipments will drop by nearly 8.5%.

As for laptop shipments, TrendForce forecasts point to a decrease of more than 5%; Gartner is predicting a 10.4% shipment decrease. Similarly, gaming console shipments could drop by more than 4% year over year.

Unfortunately, for consumers, retailers, and makers of electronics, memory’s huge demand and lack of supply mean DRAM price increases of more than 70% in 2026.

That will be passed down to shoppers, who can expect smartphone prices to rise an estimated 14% to a record high of $523… as well as the extinction of the sub-$100 phone. This could cause smartphone sales to decline by nearly 13% this year.

Computer vendors are facing a similar scenario. Major computer makers like Dell Technologies (DELL), HP (HPQ), Lenovo, Acer, and Asus are predicting price increases of up to 30% during the second half of the year.

These developments will undoubtedly impact consumers, who must decide whether to pay more for new devices or opt to avoid the sticker shock altogether. As a result, the consumer electronics industry is likely to watch its margins and order volumes shrink.

It’s also pushing tech companies and data center operators to explore other types of memory solutions.

Why Flash Memory, SSDs, and Hard Disk Drives Are Critical to AI Infrastructure

NAND flash memory, a non-volatile storage technology that retains data without power, is poised to explode in 2026. The technology – which has been primarily used in solid-state drives (“SSDs”), USB drives, and smartphones – has recently become a critical component of AI infrastructure.

Once used for general data storage, NAND flash memory and its high-capacity, high-speed storage capabilities are now coveted by AI data center operators for the memory’s performance alongside AI graphics processing units (“GPUs”) related to AI inference (running AI models).

NAND flash memory is also a space-saving solution for data centers. With 3D NAND technology, hundreds of layers of cells can be stacked vertically. This substantially increases storage density while consuming minimal space.

It also offers efficiency, as NAND flash memory uses less power than typical mechanical drives. This lowers energy consumption while improving heat dissipation, which is critical in data centers.

SSDs equipped with NAND technology are also proving their worth in AI data centers thanks to their fast read/write speeds, low latency, and quicker caching. That all adds up to faster and improved AI inference and training.

So, it’s not surprising that the NAND flash memory market is looking at significant growth. The market is projected to reach roughly $59 billion in 2026, a nearly $3 billion year-over-year increase. By 2031, projections show the NAND market hitting more than $76 billion, with a CAGR of 5.32% during that span.

The same sentiment applies to hard disk drives, of all things. A technology that was recently bordering on obsolescence within the consumer PC market has experienced an astounding resurgence.

The global HDD market is booming, riding the wave of demand for high-capacity, nearline drives for AI, cloud, and data-center storage. In fact, the market is projected to grow from roughly $51.8 billion in 2026 to around $69.7 billion by 2031… a 6.12% CAGR.

Needless to say, this is music to the memory industry’s – and its investors’ – ears.

3 AI Memory Stocks to Watch in 2026 (Not Micron)

1. SanDisk (SNDK): An AI Memory Stock Riding the NAND Wave

As my colleague John Kilhefner perfectly summarized memory’s importance to AI back in February… “If there’s no memory, there’s no AI.”

With the memory chip shortage not expected to improve anytime soon, SanDisk is capitalizing on its position as an AI infrastructure supplier.

John captured the reasons why in his February article:

The longer version tells the tale of a “perfect storm” forming in the memory market:

- AI demand surged, especially from hyperscale data centers that require massive pools of fast storage for model training and, increasingly, inference workloads.

- NAND flash supply tightened after years of industry belt-tightening and cautious capacity expansion, creating meaningful pricing power for suppliers.

Put those together, and you get what markets love most: scarcity plus necessity with pricing power as the result.

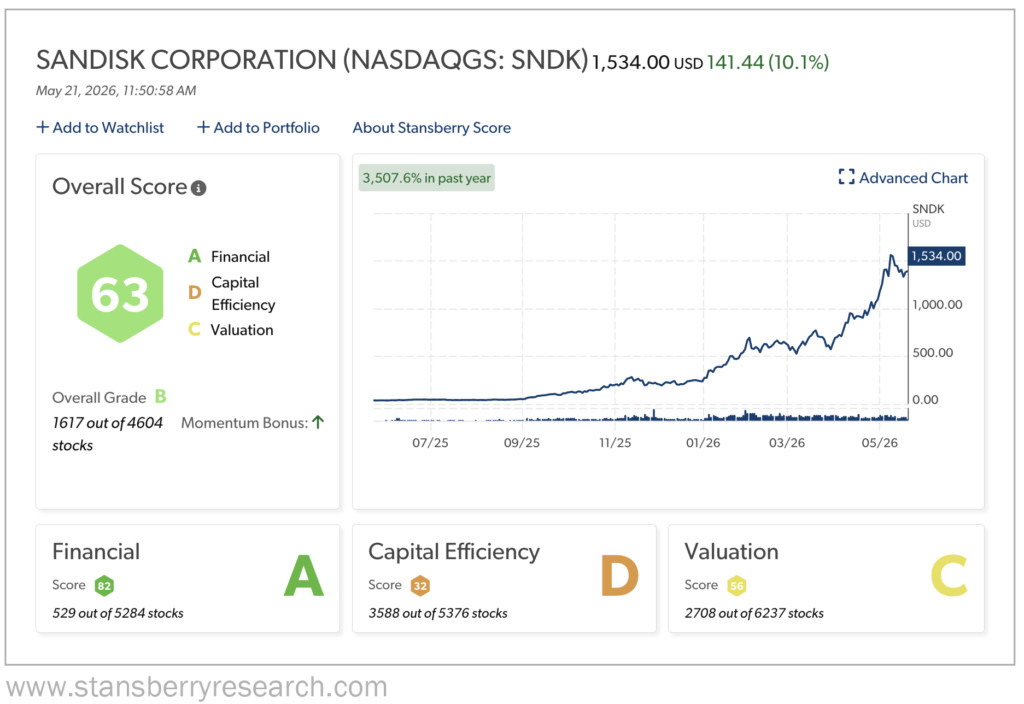

It’s borderline ridiculous how well SanDisk stock has performed since its February 2025 spinoff. SNDK’s beginning price then was roughly $48. Today? Around $1,400. That’s an increase of more than 2,800%. In just 15 months!

SanDisk’s third-quarter 2026 revenue increased roughly 96% sequentially, to $5.95 billion from the second quarter’s $3.03 billion. Those earnings obliterated analyst expectations by $1.2 billion.

This surge was fueled by the company’s mind-boggling 233% sequential increase in data center revenue, driven by strong adoption of SanDisk’s products by AI infrastructure builders, including its Stargate SSD product line. Its edge computing revenue was also a major factor, increasing 118% quarter over quarter.

It also reported operating cash flow of just over $3 billion (up roughly 3 times quarter over quarter) and free cash flow of roughly $2.96 billion – up from $843 million the prior quarter.

The company is expecting even bigger things in Q4, with projected revenue in the $7.75 billion to $8.25 billion range.

SanDisk’s Stansberry Score, which monitors and measures stocks and their long-term potential, rates as somewhat above average, despite its impressive gains.

There are a few reasons why…

- The stock’s huge surge points to signs that investors have already priced in ideal growth scenarios, resulting in extreme valuation. That gives SanDisk very little margin for error.

- Historically, SanDisk’s earnings have been inconsistent. Look no further than last year, when the company spun off from its previous owner, Western Digital. Though SanDisk’s revenue increased by roughly 10.4% in 2025, the company reported a $1.64 billion loss caused by significant transitional expenses and impairment from the spinoff.

- Lastly, SanDisk pays no dividend right now (hence its “D” grade in Capital Efficiency). This takes some of the luster off SNDK stock, especially for income-focused investors.

All that said, SanDisk is expected to turn a profit in 2026, at which point its Stansberry Score should keep improving.

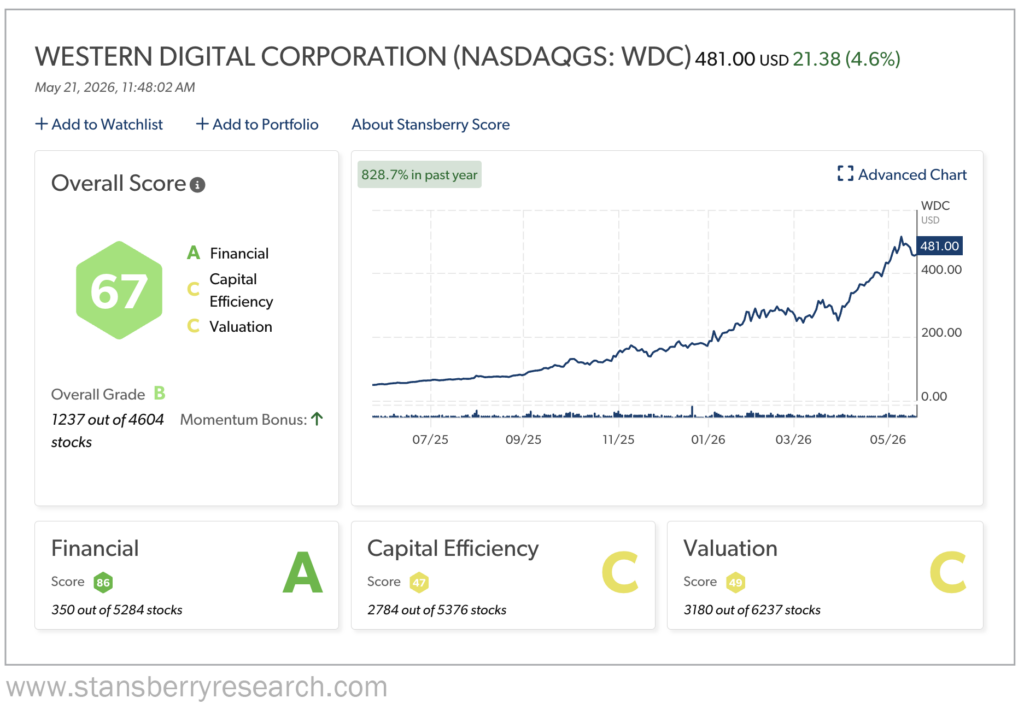

2. Western Digital (WDC): An AI Memory Stock Dominating HDD Storage

Yes, SanDisk’s previous owner is now one of its primary competitors. And though its trajectory hasn’t reached SanDisk-like heights, Western Digital – which focuses more on storage memory – is still demonstrating consistent growth as it serves as the dominant hard disk drive supplier and a major enterprise-grade SSD provider for AI data centers.

In fact, its HDD production capacity is already sold out for 2026. And the company is signing long-term purchase agreements through 2027 and 2028.

Over roughly the same period since SanDisk’s spinoff from its parent, Western Digital’s stock price soared from $49.07 on February 25, 2025 to roughly $475 on May 21, 2026 (with a few peaks and valleys along the way).

That’s an increase of 868%. It may not be SanDisk’s 2,800%, but it’s staggering, nonetheless.

Western Digital’s Q3 2026 revenue of $3.34 billion represents a 45% year-over-year increase. And its Q4 revenue is projected to be up between 36% and 44% year over year.

The company also reported $1.12 billion in operating cash flow (up from $745 million in Q2) and $978 million in free cash flow (up from $653 million in Q2).

WDC’s Stansberry Score is solid, with an overall “B” grade. That’s driven by its outstanding Financial score (“A”).

While the company does pay shareholders dividends, its current dividend yield of 0.15% is nothing to write home about. In fact, it went nearly five years without increasing its dividend payout before finally doing so in September 2025.

This helps explain its mediocre Capital Efficiency grade (“C”).

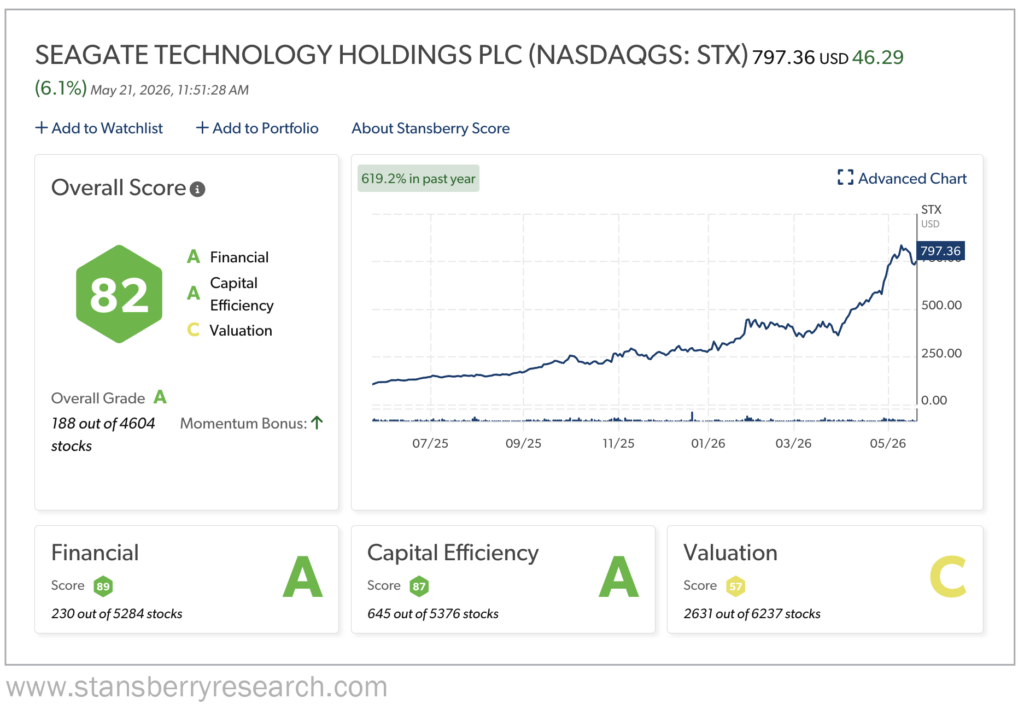

3. Seagate Technology (STX): An AI Memory Stock Built Around High-Capacity Storage

Like Western Digital, Seagate is benefiting from the need for storage memory in AI data centers. The company, which has been a leading hard drive manufacturer for years, even rebranded itself as a critical provider of AI infrastructure.

And it worked.

The key has been Seagate’s Mozaic platform and Heat-Assisted Magnetic Recording (“HAMR”) drives. This technology allows for vastly higher storage density than traditional drives. That density allows data centers to store more data without adding physical space. And that saves money.

Seagate CEO Dr. Dave Mosley’s vision of rebuilding the company around Mozaic and HAMR technology was risky. But it’s paying off in a big way.

As a highly effective solution for storing the massive amounts of data needed for AI training and inference, Seagate’s Mozaic HAMR drives have attracted the attention of hyperscale cloud providers as well as large-scale enterprises.

In fact, Seagate’s mass capacity/data center segment now accounts for 80% of its total revenue.

And that revenue continues to grow. Seagate reported $3.11 billion in revenue for fiscal Q3 2026, a nearly 10% increase from Q2 and a more than $950 million year-over-year jump.

That momentum is likely to continue following the recent news of Seagate’s Mozaic 4+ HAMR platform – which offers roughly 8 TB more storage capacity than its Mozaic 3+ platform – moving into mass production for hyperscale cloud providers.

In fact, Seagate’s 2026 hard drive capacity is completely sold out. And the company is already securing long-term order agreements into 2027.

Seagate’s stock performance – and its Stansberry Score – reflect the demand for its products.

Overall, Seagate gets an outstanding “A” grade, driven by excellent Financial and Capital Efficiency scores (“A”).

These marks are in line with fiscal third-quarter 2026 highlights that include:

- A record-breaking 47% non-GAAP (generally accepted accounting principles) gross margin, a 10.8% year-over-year increase over fiscal third-quarter 2025.

- $1.45 billion GAAP gross profit, up $687 million year over year.

- $748 million GAAP net income, up $408 million year over year.

- Operating cash flow of $1.1 billion and free cash flow of $953 million (up from $216 million year over year).

- Cash dividend of $0.74 per share.

STX has been on a roll for a year, with shares soaring nearly 630% from $108.86 to roughly $794.

And that’s no surprise, considering the demand for its storage drives from hyperscalers and large enterprises.

Memory Is a Strong AI Infrastructure “Pick and Shovel” Play

For investors looking to hitch a ride on the AI freight train, memory stocks are one of the many tickets that’ll get you on board.

Sure, the hyperscalers like Meta Platforms (META), Amazon (AMZN), and Microsoft (MSFT) grab the headlines. But it’s behind the scenes – or rather, within the data center walls – where money can be made.

It’s the companies generating the energy that literally power data centers… like NextEra Energy (NEE) and Vertiv (VRT).

And the data center real estate investment trusts (“REITs”) that own, develop, and manage the facilities that house AI infrastructure, like Digital Realty (DLR) and Equinix (EQIX).

It’s the semiconductor makers like Nvidia (NVDA)and Taiwan Semiconductor Manufacturing (TSM). And the nanotechnology used to make advanced chips.

Now, it’s also the memory that supplies AI models with the data they need to process information and make instant, intelligent, and autonomous decisions. As well as the storage that holds all that data.

Regards,

David Engle

Editor’s note: Forbes calls $1 billion fund manager Louis Navellier “the king of quants.” Today, he’s stepping forward to reveal why he’s investing $358 million of his own firm’s money in the next stage of Artificial Intelligence… a technological sea-change that could erase millions of jobs, solve humanity’s biggest mysteries, and spark a wave of moneymaking opportunities — both in and outside the stock market. Click here for the details…