Key Points

- Neocloud providers CoreWeave and Nebius Group, along with AI infrastructure specialist Astera Labs, were added to the Nasdaq 100 Index, highlighting the growing influence of AI and data-center businesses in the technology sector.

- CoreWeave and Nebius are rapidly expanding cloud infrastructure providers with massive revenue backlogs but ongoing losses, while Astera Labs is already profitable and benefiting from strong demand for AI connectivity hardware.

- Nasdaq 100 inclusion could attract billions in new investment. Because major ETFs and index funds track the Nasdaq 100, the addition of these stocks may drive increased institutional ownership, liquidity, and visibility among investors.

Neocloud providers CoreWeave (CRWV) and Nebius (NBIS), as well as AI-infrastructure company Astera Labs (ALAB), officially joined the Nasdaq 100 Index on Monday – along with aerospace company Rocket Lab (RKLB) and advanced robotics manufacturer Teradyne (TER) – signifying a reshaping of the tech index as it leans more into businesses innovating in artificial intelligence (“AI”) and data centers.

Let’s take a closer look at CoreWeave, Nebius, and Astera Labs to analyze their businesses and Stansberry Score metrics now that each has been added to the Nasdaq 100.

CoreWeave: The AI Cloud Leader

Neoclouds, incredibly powerful computer networks designed specifically to run the most demanding AI programs on the best chips, have become an increasingly important part of the AI industry.

By providing dedicated, highly optimized graphics processing unit (“GPU”) power, neoclouds are built to improve efficiency and reduce bottlenecks when running complex AI models.

CoreWeave has set the standard for neoclouds, having inked a long list of megadeals since the start of 2025 that guarantee the company billions in revenue for the foreseeable future:

- Meta Platforms (META):This deal includes a $21 billion commitment with Meta to provide Mark Zuckerberg’s hyperscaler with dedicated AI cloud capacity through 2032.

- Anthropic: CoreWeave agreed to a multiyear deal with the AI giant to provide the compute capacity needed to run massive workloads for Anthropic’s Claude AI models.

- Nvidia (NVDA): The bellwether chipmaker invested $2 billion in CoreWeave’s Class A common stock to push the AI factory build-out.

- Jane Street: Quantitative trading firm Jane Street went all-in on CoreWeave, committing $6 billion to the company’s AI cloud platform and another $1 billion in equity.

- OpenAI: The Sam Altman-led AI giant invested another $6.5 billion (for a total commitment of roughly $22.4 billion) in its cloud infrastructure partnership with CoreWeave.

CoreWeave is banking on these contracts, part of a nearly $100 billion revenue backlog through the first quarter of 2026, to push the company out of the red and into the black.

While CoreWeave blew away last year’s first-quarter revenue of $982 million with $2.08 billion in the first quarter of 2026, the company still reported a $740 million net loss for the quarter. That loss more than doubled year over year.

There’s an obvious reason for the massive loss increase, however. CoreWeave is clearly in the “you have to spend money to make money” phase of its business, with up to $35 billion in capital expenditures (“capex”) projected throughout 2026 as it expands its data-center and GPU infrastructure.

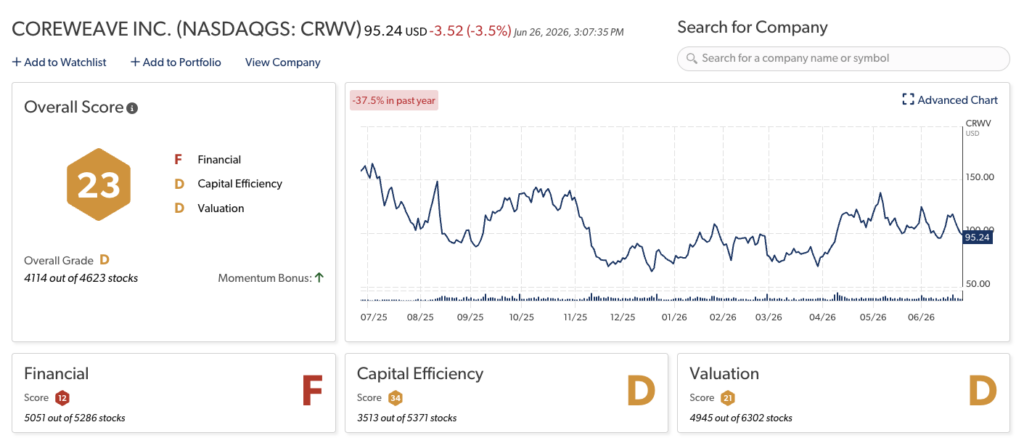

A quick glance at CoreWeave’s Stansberry Score, a tool that helps determine the quality and long-term value of thousands of stocks, illustrates the clear impact of the company’s massive debt.

CoreWeave’s overall “D” score is dragged down by both its capital efficiency and valuation – but it’s primarily a reflection of the company simply not being profitable right now.

Is CoreWeave stock worth the investment? There are legitimate bull and bear arguments to be made. The bullish case points to the company’s growing revenue and, primarily, its significant backlog, which promises steady income from industry titans like Meta, Nvidia, and OpenAI.

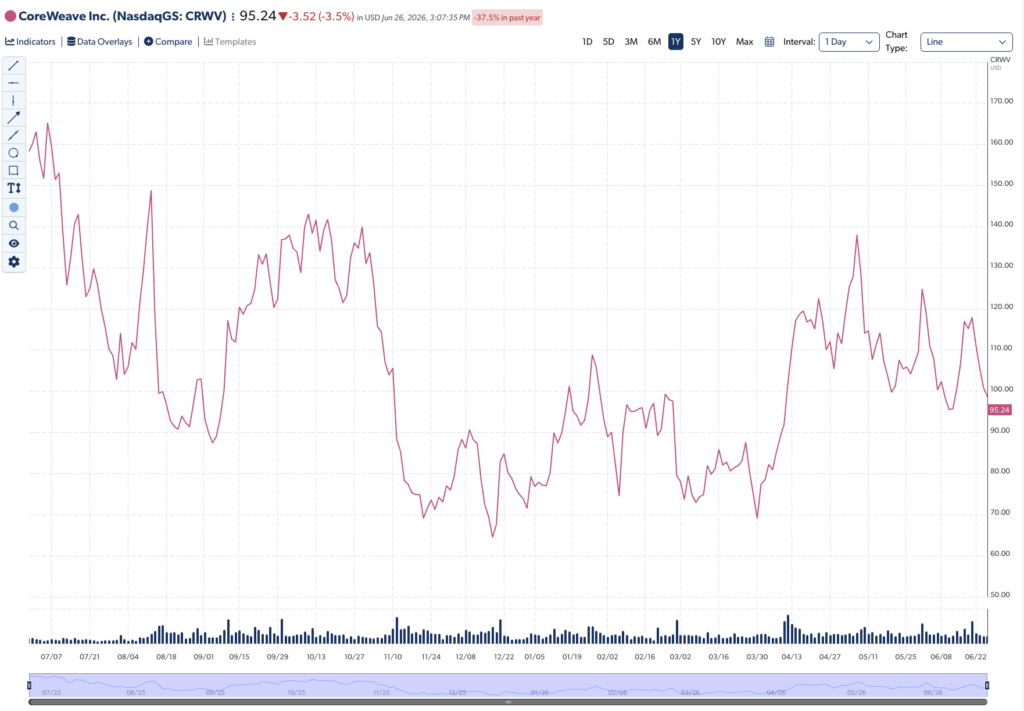

The bearish argument demonstrably points a finger at CoreWeave’s very red balance sheet and the fact that the company’s stock has actually declined by 38% over the past year.

A silver lining? Since hitting its 2026 low point of $69.15 on March 30, the stock is up more than 40%.

Whether you want to invest in CoreWeave depends on your risk appetite. There’s certainly tons of upside, but that should be tempered by strong caution given not only the company’s losses but also the volatility of its industry.

The average beta – which measures the volatility of a stock relative to the overall market – for the three stocks we’re analyzing here is 2.66, meaning these neocloud stocks are roughly 2.7 times as volatile as the market.

Nebius Group

There’s a lot of momentum behind Nebius right now as it enters the Nasdaq 100. The neocloud company provides the full-stack infrastructure needed to test, train, and deploy AI at scale.

And it manages large GPU clusters across North America, Europe, and the Middle East via the Nebius AI Cloud platform, enabling enterprises to instantly run server-free AI workloads.

Like CoreWeave, Nebius has inked its share of major deals over the past year and a half.

- Meta: Nebius agreed on a $3 billion deal in November 2025 to provide Meta with AI infrastructure over a five-year span. Meta doubled down on its investment in Nebius in March when it expanded the agreement to include $12 billion of dedicated compute based on a large-scale deployment of the Nvidia Vera Rubin platform. Nebius will begin delivering this capacity in early 2027.

- On top of all that, Meta agreed to purchase more available compute capacity for a total of up to $15 billion over five years. That brings this contract’s value up to potentially $27 billion.

- Microsoft (MSFT): Nebius and Microsoft agreed to a five-year contract worth up to $19.4 billion last September. Nebius will provide Microsoft with GPU capacity from its new data centers – primarily the 300-megawatt (“MW”) facility in Southern New Jersey.

- Nvidia: The chip giant invested $2 billion in Nebius in March, building on the company’s continuous deployment of Nvidia hardware across the Nebius platform. This will help Nebius’s quest to deploy more than 5 gigawatts (“GW”) of compute capacity by the end of 2030, using the latest generation of Nvidia’s architecture.

- Bloom Energy (BE): Nebius and Bloom Energy signed a 10-year agreement in May worth up to $2.6 billion in service fees to deploy fuel cells across Nebius’s U.S. data centers. This ensures 250 MW of power capacity by the end of the year.

Again, similar to CoreWeave, these contracts are critical as they guarantee Nebius steady revenue moving forward. The company’s current backlog sits at roughly $46 billion, positioning it for at least a few years of success.

And Nebius will need that success in the coming years, because – once again, like CoreWeave (are you sensing a theme among neocloud companies?) – Nebius is not turning a profit yet.

But its $46 billion backlog is starting to convert into revenue. Its $399 million first-quarter revenue is evidence of that. And as Nebius continues to complete its contracts over the next few years, that revenue should continue to grow.

For comparison, CoreWeave is in the same boat, though with a backlog more than double that of Nebius. CoreWeave expects roughly 36% of its nearly $100 billion backlog to be recognized within the next two years and roughly 75% to convert into revenues over the next four years.

Nebius could certainly use that backlog revenue now. The company lost a little more than $100 million in the first quarter of 2026 as it continued making investments in expanding its infrastructure and developing its AI platform.

That was, however, the only piece of bad news for Nebius. The company otherwise enjoyed a tremendous first quarter, earning that $399 million in revenue – a staggering 684% year-over-year increase.

Nebius also reported positive EBITDA (earnings before interest, taxes, depreciation, and amortization) of $129.5 million. During last year’s first quarter, it suffered a $53.7 million EBITDA loss. That’s an impressive one-year turnaround.

The company also exited the first quarter of 2026 with $9.3 billion in cash and cash equivalents – a massive increase compared with last year’s $3.7 billion.

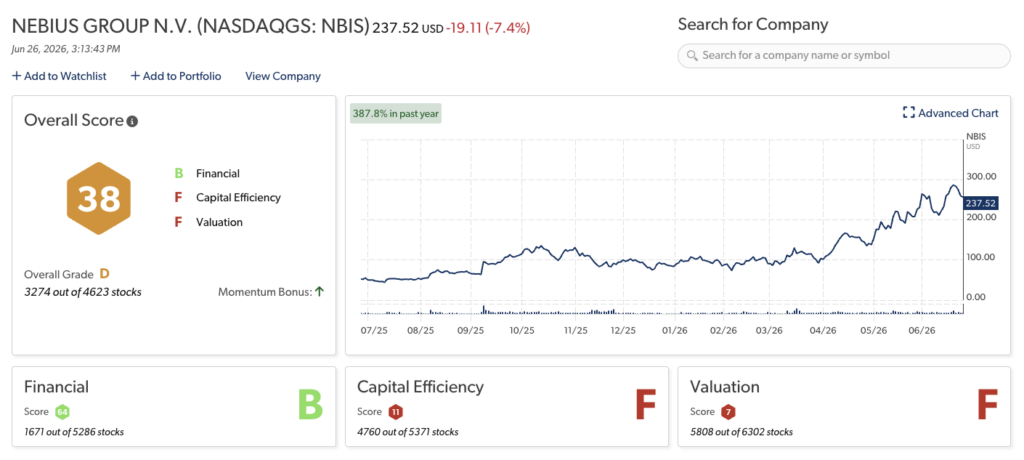

Looking at Nebius’ Stansberry Score might not offer much optimism, but there is some underlying momentum. The stock looks terrible on capital efficiency and valuation, as it’s generally viewed by analysts as overvalued. But its financials grade is at a strong “B,” riding the year-over-year revenue explosion from the first quarter.

Nebius stock has also been on a massive roll for a year, gaining more than 350% over that time.

But will it continue at that rate? Probably not. Nebius’s overvaluation largely stems from assumptions that the coming years will be executed precisely and that profit will begin to scale. The problem is that Nebius is simply not there yet.

Yes, Nebius’s contracts with hyperscalers Meta and Microsoft promise scalable revenue. And yes, Nebius is converting up to $9 billion of its backlog into actual revenue. But the company is still spending quite a bit – up to $25 billion – to achieve its goal of 1 GW of data center capacity by the end of this year. That includes massive AI factories in Pennsylvania and Missouri, as well as facilities in the United Kingdom.

So, Nebius is facing a lot more future capex, it’s not yet profitable, and it remains volatile. But the company’s eye-popping first-quarter revenue, $46 billion backlog, and addition to the Nasdaq 100 make it a stock to watch closely.

Astera Labs

Astera Labs builds what’s at the heart of today’s AI servers – the critical software and hardware that allows huge clusters of central processing units, GPUs, and memory to work in harmony within AI and cloud data centers.

While the company can’t boast a list of major partners as long as CoreWeave’s and Nebius’s, it does have one very important – and massive – client in its portfolio: Amazon (AMZN).

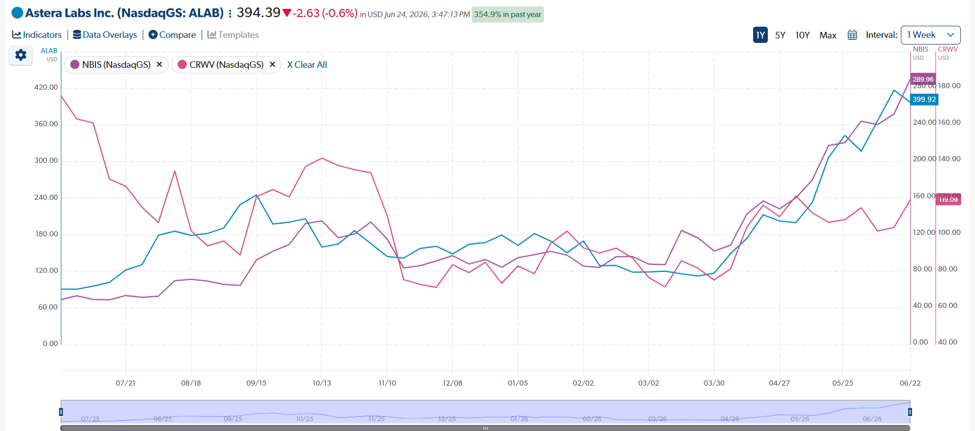

In February, Amazon and Astera agreed to a seven-year warrant deal that provides Amazon with the right to purchase up to $6.5 billion in future Astera products as well as warrants to buy more than 3.2 million common shares of Astera at its trading price of $142.82 each. (Astera stock since closed at $399.92 on June 24.)

Essentially, this deal positions Astera as the main connectivity provider for Amazon’s custom Trainium and Inferentia AI chips – a huge score for the company.

The Amazon deal helped propel Astera to a fantastic first quarter of 2026. Astera earned a company-record $308.4 million in revenue for the quarter… a 93% year-over-year increase.

Among the other highlights were more than $235 million in gross profit and roughly $80.3 million in net income – both significant differentiators from CoreWeave and Nebius. Perhaps most impressive were its 76.3% gross margins.

And its second-quarter guidance projects plenty of confidence, with revenue between $355 million and $365 million.

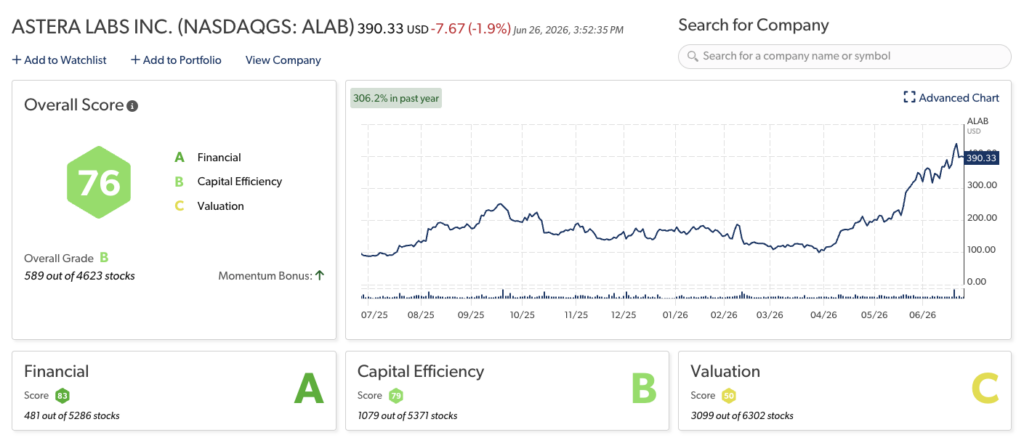

Astera’s stock, based on its rock-solid Stansberry Score (“B” overall), is a seemingly steadier bet than either CoreWeave or Nebius. Its financials (“A”) are outstanding (it is a profitable company, after all), and its capital efficiency is strong (“B”).

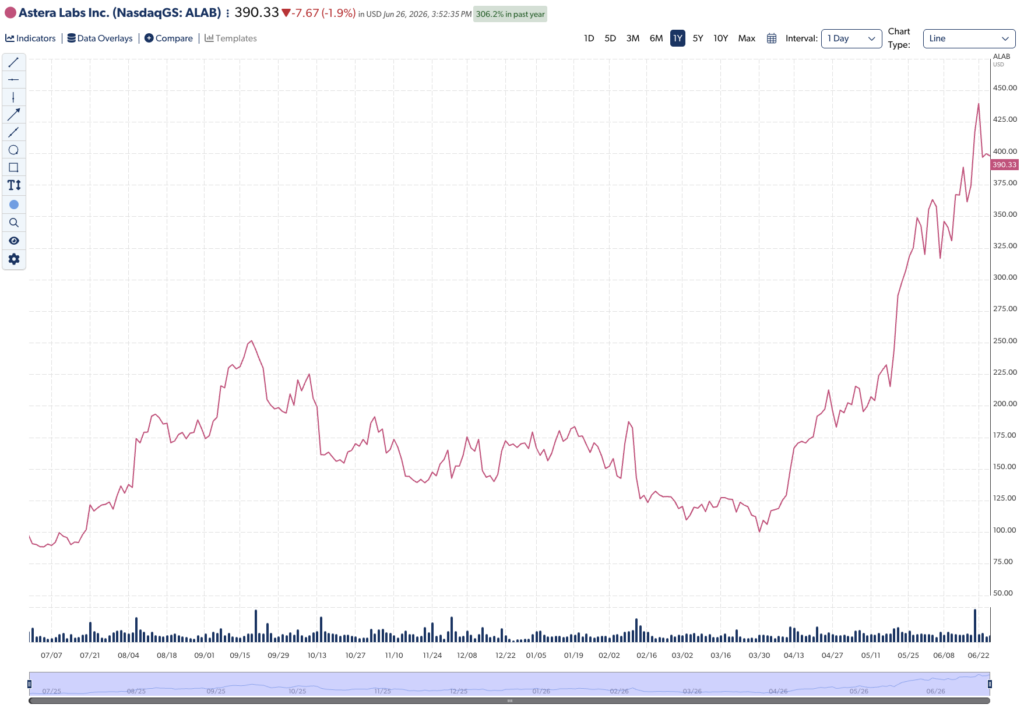

It’s also performed quite well over the past year, increasing its share price by more than 300%.

Again, volatility is always important to keep in mind. Despite its incredible run since last June, you can see the peaks and valleys in the chart above. If you’re willing to ride the waves, your patience may pay off in the long term.

Astera may not have a client roster as impressive as CoreWeave or Nebius, but the company is operating on steadier ground. Astera is making money, managing it well ($1.18 billion in cash and equivalents), and has a reliable source of revenue from Amazon.

Its stock is also trading at a premium right now – roughly $383 compared with an average 12-month price target of roughly $263. That’s enough to scare off some investors. It might be best to wait for a dip, although Astera offers plenty of upside.

Nasdaq 100 Benefits for CoreWeave, Nebius, and Astera Labs

These are not perfect stocks or perfect companies. Two of the three – CoreWeave and Nebius – aren’t making money (yet), and their stocks are considered overvalued and volatile.

But all three of these AI-infrastructure companies offer tons of potential and already have impressive market capitalizations. As of June 26, CoreWeave’s market cap was just above $52.2 billion, Nebius was at $61.6 billion, and Astera Labs was just above $66 billion. And two of the three stocks are significantly higher today than they were a year ago (CoreWeave being the exception).

But even more significant is their new listing in the Nasdaq 100, which comes with a level of prestige and respect reserved for the world’s leading tech innovators.

And it also means the potential for a substantial influx of capital. Because the Nasdaq 100 is an important benchmark used to track billions in capital, massive index-tracking ETFs and index funds are automatically triggered (and legally required) to purchase shares of the newly added stock.

Of course, with these benefits comes extra scrutiny by the media and analysts. (Kind of like this article.)

But that’s really a small price to pay to be considered elite enough for inclusion in the Nasdaq 100. Now let’s see how CoreWeave, Nebius, and Astera Labs perform in the brighter spotlight.

Regards,

David Engle

Editor’s Note: As America celebrates its 250th birthday, a Wall Street legend is sounding the alarm. Whitney Tilson (the hedge fund manager CNBC dubbed “The Prophet”) says the AI revolution is rewriting the rules of wealth faster than most people realize. Some investors are already seeing extraordinary gains. Others are being wiped out. Tilson says the next six months will determine which side you end up on — and he’s sharing exactly what to do about it in his free presentation here.

Recent Articles

Dell’s AI Factory Is Booming and the Stock Has Soared in 2026. Is It a Good Buy Right Now?

Why the PayPal Stripe Deal Is Proof That Elon Musk’s X Money Already Won