Image Credit: Associated Press

Key Points

- Micron’s stock has surged by more than 500% in the past year, driven by unprecedented demand for AI-related memory chips.

- High-bandwidth memory (“HBM”) shortages and rising prices are fueling record revenue, margins, and cash flow growth.

- Meanwhile, supply constraints, helium shortages, and the risk of future oversupply present potential challenges ahead.

- While bullish projections point to a $1,000-plus valuation, more conservative estimates align closer to current trading levels.

Micron Technology (MU) stock closed at $69.33 a year ago. Fast-forward to 2026, and the memory chipmaker finished trading at $465.66 on April 14.

That’s a gain of roughly 572% in just one year.

In other words, Micron is white hot… and it likely hasn’t reached its peak.

Arete Research raised its price target on Micron to $852 on April 13 Other analysts are going even higher with targets of $1,000 and even $1,200!

Now, these are clearly at the high end of analyst targets. For context, the average price target for Micron on April 15 is $553.10, according to MarketWatch.

That target certainly seems more realistic. But the $1,200 target? It no longer feels entirely impossible for a few reasons.

- Micron, as we just noted, soared more than 500% in one year.

- The demand for high-bandwidth memory (“HBM”), especially AI memory chips, is sky-high. And that demand is not likely to fade anytime soon.

- That constant demand means consistently increasing revenue for Micron.

What’s Driving Analysts to Price Micron So Aggressively?

Let’s look at these factors more closely.

AI’s Unwavering Demand for Memory

Back in November, I wrote about AI data centers’ need for high-bandwidth memory:

HBM chips are so in demand that Micron, SK Hynix, and Samsung’s HBM capacity sold out through the rest of 2025 and into 2026. That sort of demand means one thing – pricing power. Those simple supply-and-demand economics make HBM manufacturers a very intriguing play for investors.

In short, the world needs more memory. The companies that sell it are in a powerful position. That means we should continue to see higher memory prices.

And that’s proven to be true. According to Counterpoint Research, memory prices across dynamic random-access memory (“DRAM”), NAND, and HBM have skyrocketed 80% to 90% from the fourth quarter of 2025 to the first quarter of 2026.

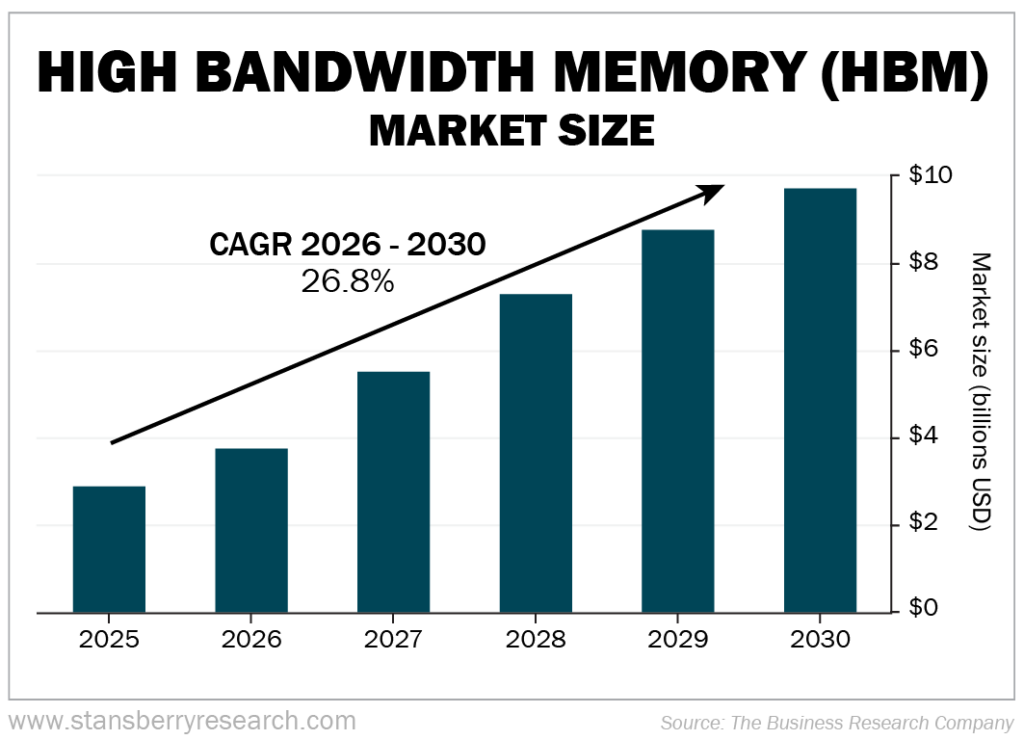

Naturally, that’s pushed the HBM market to never-before-seen heights. And it will continue to follow that trajectory throughout the rest of the decade. According to the Business Research Company, the HBM market will reach $9.84 billion in 2030 at a compound annual growth rate (“CAGR”) of 26.8%.

Throughout 2025, Micron and Samsung jockeyed for second place in HBM market share. Micron held steady in the 20% to 22% range for most of the year. Meanwhile, South Korean-based SK Hynix was the runaway market share leader in the 60% to 62% range.

Still, a 20% to 22% share of $3 billion (in 2025) is significant. And that was primarily driven by AI’s demand for memory in data centers.

As I wrote back in November:

The AI boom is not slowing anytime soon. Projections show that more than 8,300 AI data centers will be up and running globally by 2030… up from around 6,100 today.

As more AI data centers pop up around the world, and as new AI innovations roll out, HBM will remain in high demand. And not just because of HBM’s ability to ease the AI memory bottleneck. They also reduce energy consumption.

This is critically important because AI data centers generate massive amounts of power. A typical hyperscaler center requires around 100 megawatts of power. That figure is expected to soar to around 1 gigawatt (“GW”) or more. And 1 GW of power is enough to satisfy the peak power demand of a city the size of San Francisco…

HBM chips can reduce energy consumption by up to 70% for certain AI workloads, compared to standard memory systems. That’s the type of efficiency AI data centers need as they search for energy savings. And it’s one reason why HBM chips are such high-demand components.

Between saving energy and providing the memory that companies like Advanced Micro Devices (AMD) and Nvidia (NVDA) need to build their AI chips, HBM manufacturers like Micron are irreplaceable within today’s AI infrastructure.

And that’s exactly why Micron has completely sold out its inventory for 2026 and is signing customers to long-term supply agreements (up to five years) into 2027 and beyond.

That Demand Equals Steadily Increasing Revenue for Micron

Economics 101 tells us it’s not the least bit surprising that Micron’s revenue has exploded alongside the rising demand for its products.

And, it has certainly exploded.

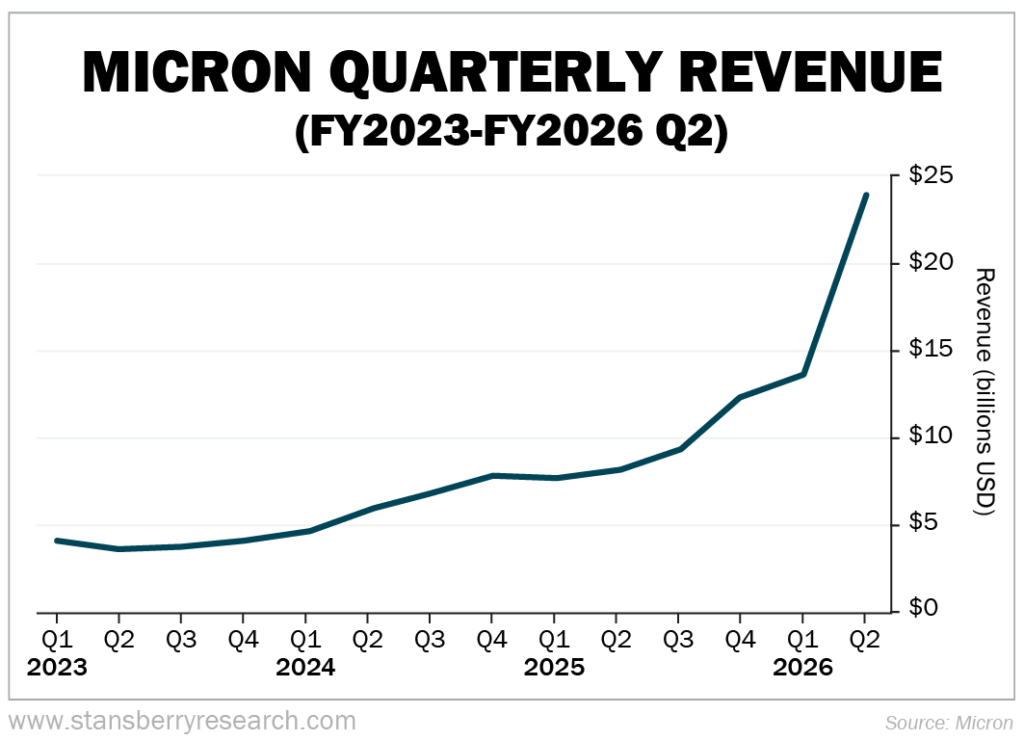

The first quarter of fiscal 2026 was a record-breaker for Micron as it earned roughly $13.6 billion in revenue – up 57% year over year (“YOY”). Micron also generated roughly $8.4 billion in operating cash flow and $3.9 billion in free cash flow, with a non-GAAP (generally accepted accounting principles) gross margin of 56.8%.

Micron’s second quarter? Even better… and not particularly close.

In fiscal second quarter 2026, Micron:

- Pulled in nearly $23.9 billion in revenue – a nearly 75% quarter-over-quarter increase and roughly 196% YOY.

- Generated $11.9 billion in operating cash flow – up nearly 42% over the first quarter and roughly 202% YOY.

- Achieved a non-GAAP gross margin of 74.9% – a quarter-over-quarter increase of nearly 32%, and YOY growth of nearly 98%.

- Reported $6.9 billion in adjusted free cash flow – up roughly 77% from the first quarter and a staggering 705% YOY.

Micron’s growth, revenue-wise, over the past three-plus years is nothing short of astounding.

Obviously, that giant spike beginning halfway through fiscal 2025 was driven (and continues to be) by the AI data-center boom.

What Challenges Does Micron Face Moving Forward?

Will Micron stay on a steep upward trajectory? The demand is certainly there. But there are a couple of hurdles Micron must clear first.

Inability to Meet Customer Demand

Memory chip demand is certainly not one of those challenges. But the capacity to satisfy that demand will be.

Micron CEO Sanjay Mehrotra confirmed as much during the company’s fiscal first-quarter earnings conference call on December 17. Among Mehrotra’s revealing statements were:

Over the last few months, our customers’ AI data center build-out plans have driven a sharp increase in demand forecasts for memory and storage. We believe that the aggregate industry supply will remain substantially short of the demand for the foreseeable future.

The dramatic increase in HBM demand is further challenging the supply environment due to the 3-to-1 trade ratio with DDR5 [memory], and this trade ratio only increases with future generations of HBM… Together, these demand and supply factors are driving tight industry conditions across DRAM and NAND, and we expect tightness to persist through and beyond calendar 2026.

Perhaps most revealing…

Micron is working hard to support our customers’ demand during this time, and we expect to grow our DRAM and NAND bit shipments approximately 20% in calendar [year] 2026. Despite significant efforts, we are disappointed to be unable to meet demand from our customers, across all market segments.

Mehrotra took it a step further in a CNBC interview on March 19, after Micron’s fiscal Q2 earnings were released:

We are only able to supply, for our key customers in the midterm, about 50% to two-thirds of their requirements.

HBM supply simply can’t keep up with demand.

It’s not for lack of trying on Micron’s part, however. The company announced on March 16 that it had completed a $1.8 billion acquisition of a chipmaking plant in Taiwan from Powerchip Semiconductor Manufacturing. The problem here is that wafer output likely won’t occur until the second half of 2027.

Micron is building two DRAM memory chip fabs in Idaho, which will certainly help. But production from the first fab won’t begin until 2027, with the second facility to follow later.

Similarly, Micron broke ground on an advanced wafer fab in Singapore in late January, one that will provide Micron with 700,000 square feet of cleanroom space. The company is putting $24 billion into the project over 10 years. But wafer output won’t begin until the second half of 2028.

Long term, Micron is investing up to $100 billion to create up to four memory fabs in New York state over the next 20-plus years. And the company plans to spend more than $2 billion to expand and update its fab site in Manassas, Virginia.

This is all fantastic news for Micron and the AI industry moving forward. These new facilities will scale Micron’s output exponentially.

But it doesn’t help today.

Right now, Micron can’t fulfill a significant portion of its existing orders. But that’s not necessarily Micron’s fault. Nor can anyone blame its competitors, who are facing the same challenges. There just isn’t enough supply to meet the nonstop demand.

The War in Iran Is Hurting Helium Supply – and Chip Production

This may come as a surprise, but helium is crucial to chipmaking. Yes, the same gas that fills balloons is literally irreplaceable as far as its role in the manufacturing process. And the war in Iran is decimating the world’s helium supply.

I wrote about this topic on April 16:

Interesting fact: The semiconductor industry is the world’s largest consumer of helium. According to research firm IDTechEx, the semiconductor industry currently accounts for approximately 24% of total global helium consumption. The firm predicts that this amount will hit 30% by 2030.

While most people (correctly) associate silicon, copper, and other metals with semiconductor manufacturing, helium is just as essential a component. In fact, without helium, semiconductor fabrication would be impossible.

That’s because the gas possesses unique properties… that allow it to perform where no other materials can. Those properties make helium irreplaceable in the wafer cooling and photolithography steps of the semiconductor fabrication process, as well as advanced chip packaging and hard disk drive manufacturing.

Qatar, located along the Persian Gulf across from Iran, is responsible for roughly one-third (between 30% and 35%) of the world’s helium supply. Between the closure of the Strait of Hormuz and a March attack by Iran on Qatar’s largest liquefied natural gas facility – which damaged helium production lines – helium supply is quickly becoming a major problem.

And that only feeds into the backlog of AI memory chips and semiconductors. Long story short, the helium shortage is directly impacting Micron and its chipmaking peers.

Will Today’s Memory Chip Shortage Become Tomorrow’s Overproduction?

When companies face a shortage of product, what do they do? They invest tons of money in building factories and plants to produce more of that product to satisfy the demand. That’s exactly what’s happening with Micron, as we just outlined, as well as every other major player in the AI and chip industry.

So, what happens, say, a few years from now, when all these companies have funneled billions into these projects and are churning out more chips than ever before? Suddenly, there’s no memory shortage. But there could be a supply overflow.

What if the AI and memory markets soften? Now chipmakers are facing a market-wide oversupply, resulting in excess inventory of products that are rapidly being replaced by newer, faster iterations. And, with more chips on the market than supply demands, prices will tumble.

Of course, these are all hypotheticals. But they’re also scenarios that could easily unfold if market winds shift even in the slightest direction.

Will Micron Ever Hit Those High-End $1,200 Analyst Price Targets?

It’s a bold bet, but it’s theoretically feasible. The math tells us so.

Let’s look at Micron’s earnings per share (“EPS”). In fiscal second-quarter 2026, Micron’s $12.20 EPS absolutely torched analysts’ average estimates of $8.60.

Riding that momentum, Micron’s full-year projected EPS has risen to $57.76.

Now, using Micron’s current trailing-12-months, price-to-earnings ratio of roughly 20.98 and multiplying that by the projected EPS of $57.76, you get a price target of $1,212.

Wow.

But let’s back up for a moment. If we redo the math with Micron’s current forward P/E ratio of around 8, the numbers are much different. Now we’re looking at a price target of roughly $463, which is in line with Micron’s current trading price.

Big difference.

That’s not really a bear argument, either. That math simply suggests that the market doesn’t fully expect Micron to continue growing at the mind-blowing rate it has recently, at least not for the long term – especially for a company that operates in a historically volatile and cyclical sector.

But that doesn’t mean Micron won’t continue its growth. The demand for its products says it will. It just likely won’t continue at its current rate, especially over an extended period.

But that $553.10 average price target looks well within reach. And, given the sky-high demand for high-bandwidth memory, it’s likely just a matter of time before Micron gets there.

Regards,

David Engle

Editor’s note: Should investors prepare for an AI crash or buy the dips? Analyst and True Wealth editor Brett Eversole just posted a surprising answer. According to Brett’s research, there’s a pattern taking shape that could defy all the worst predictions about a bust. He’s calling it a Melt-Up Tsunami. And he’s identified at least a half-dozen stocks that could benefit, including his No. 1 stock to own right now. He shares the ticker in this new presentation.

Recent Articles

KKR, Blackstone, and Brookfield Bet $16 Billion on Kuwait’s Oil Pipeline Deal

Bloom Energy’s Recent Mega Sell-Off Could Be a Buying Opportunity After a Blowout Earnings Report