Image Credit: Associated Press

Key Points

- Micron Technology reached a $1 trillion market capitalization on Tuesday after its stock nearly doubled over six weeks, driven by surging AI memory demand and bullish analyst upgrades.

- UBS tripled its Micron price target to $1,625 per share, while long-term customer agreements and sold-out production capacity through much of 2027 continue to strengthen the company’s revenue outlook.

- Despite Micron’s massive rally, many analysts remain bullish because of booming AI memory-chip demand, rapid revenue and cash-flow growth, and the company’s key role in AI infrastructure.

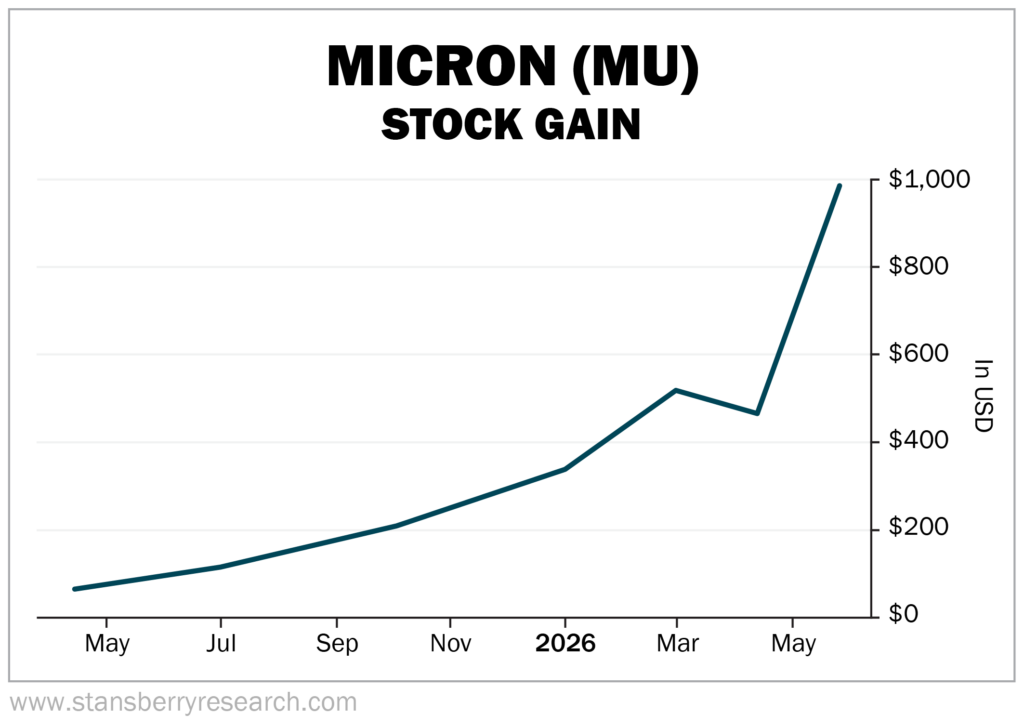

Micron Technology (MU) shares skyrocketed the day after Memorial Day as the company reached the $1 trillion market value milestone for the first time. The stock closed at $895.88 and then peaked at nearly $985, roughly an hour before the market opened on May 27.

Over the past six weeks, the stock has gone bonkers, nearly doubling in price by market open on May 27.

On April 21, I wrote the following about Micron Technology’s (MU) stock soaring thanks to AI-driven memory demand:

Micron Technology stock closed at $69.33 a year ago. Fast-forward to 2026, and the memory chipmaker finished trading at $465.66 on April 14.

That’s a gain of roughly 572% in just one year.

In other words, Micron is white hot… and it likely hasn’t reached its peak.

If we stick to that $69.33 closing price from April 16, 2025 and redo the math based on this massive spike, Micron has generated a roughly 1,321% return in a little more than a year.

And the thing is, I believe $985 could just be the beginning. There’s a bull case for Micron going well over $2,000 per share in the not-too-distant future.

Micron Stock Soars on Massive Boost to Analyst’s Price Target

The primary driver of Micron’s extraordinary gains on May 26 was Swiss investment firm UBS. It didn’t just raise its price target for Micron, but tripled it.

After citing the strength of Micron’s long-term agreements and partially fixed pricing (which promise ample revenue in the coming years), UBS increased its target from $535 to $1,625 per share.

That was enough to push Micron’s stock into the stratosphere and lift its valuation past the trillion-dollar mark. Only a few weeks ago, Micron passed $700 billion in market value.

To quote Anchorman‘s Ron Burgundy… “Boy, that escalated quickly.”

But it isn’t really a surprise.

Here’s more from the piece I wrote on April 21 discussing the recent swing (much) higher in analyst price targets:

Arete Research raised its price target on Micron to $852 on April 13. Other analysts are going even higher with targets of $1,000 and even $1,200!

Now, these are clearly at the high end of analyst targets. For context, the average price target for Micron on April 15 is $553.10, according to MarketWatch.

That target certainly seems more realistic. But the $1,200 target? It no longer feels entirely impossible for a few reasons.

- Micron, as we just noted, soared more than 500% in one year.

- The demand for high-bandwidth memory (“HBM”), especially AI memory chips, is sky-high. And that demand is not likely to fade anytime soon.

- That constant demand means consistently increasing revenue for Micron.

The average price target for Micron is $696.51 as of May 27. Still well below its market price, but also nearly $150 above MarketWatch’s average target just six weeks ago.

Considering Micron may very well finish May trading around $1,000 per share, that $1,200 price target is more feasible than ever, and it could hit that level in the coming months. Then again, in the short term, it could also retreat from its recent highs.

If you’ve already invested in Micron, you’re probably feeling pretty good right now. But does it make more sense to hold onto your shares or cash out while the company – and its stock – is riding higher than ever before?

The Bull Case for Projecting Micron to $2,500

The temptation to sell is understandable, especially if you were wise enough to get in on Micron before its massive spike in April. There are plenty of gains for you to realize if that’s when you bought.

But the bull case for holding onto your Micron shares is also rather convincing. Remember that, in just six weeks, Micron’s average price target increased by nearly $150. Yes, it’s still trading well above its price target, but that’s when you turn to Micron’s business and see that there are few – if any – signs of it slowing down anytime soon.

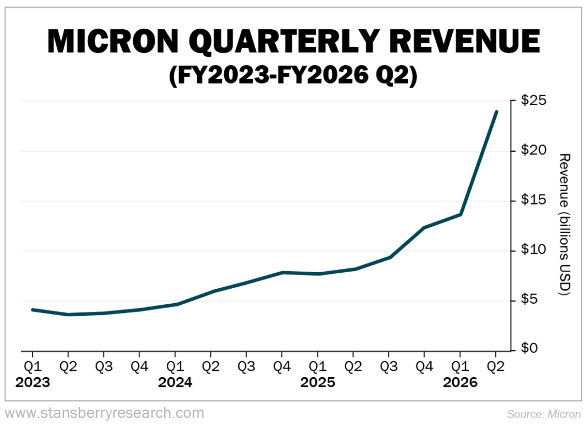

In its fiscal second quarter 2026, Micron:

- Earned nearly $23.9 billion in revenue – a roughly 75% quarter-over-quarter and roughly 196% year-over-year (“YOY”) increase.

- Generated $11.9 billion in operating cash flow – up nearly 42% over the first quarter and roughly 202% YOY.

- Achieved a non-GAAP (generally accepted accounting principles) gross margin of 74.9% – a quarter-over-quarter increase of nearly 32%, and YOY growth of nearly 98%.

- Reported $6.9 billion in adjusted free cash flow – up roughly 77% from the first quarter and a staggering 705% YOY.

And here’s a look at Micron’s quarterly revenue over the past few years:

Now, let’s look at earnings per share (“EPS”). In its fiscal second quarter 2026, Micron’s $12.20 EPS blew away analysts’ average estimates of $8.60.

Using Micron’s trailing 12 months (“TTM”) price-to-earnings (P/E) ratio of 43.76 on May 27 (more than double what it was in mid-April), and multiplying that by a projected EPS of $57.71, you get a price target of $2,525.

At first glance, that $2,525 price target feels more like a possible long-term projection, assuming Micron continues its torrid revenue growth over the next few years. But I don’t think it will take a few years to get there.

Remember what I wrote a little more than a month ago about a $1,212 price target being a bit of a pie-in-the-sky projection. Suddenly, that’s not pie-in-the-sky at all anymore. In fact, it seems like a short-term inevitability.

That’s why a $2,500-plus potential price target isn’t such a far-fetched scenario.

Micron’s entire 2026 inventory is sold out, as is much of its 2027 production. The company literally can’t make its products fast enough to satisfy the unrelenting memory demand driven by AI and data centers. That takes Micron’s customer agreements into 2028 and beyond, ensuring the company a hefty amount of guaranteed long-term income.

The bottom line is that Micron makes products that are and will remain in extraordinarily high demand for the foreseeable future. AI seemingly gains more momentum by the day, and Micron provides the memory that it needs to function.

Additionally, consider that Micron’s forward P/E ratio is roughly 9. It’s pretty mind-blowing to think that a stock that has grown by 13 times in a little more than a year could still be considered a bargain. But here we are.

When a company’s profits are growing at the same pace as its stock price, there’s a lot of value to be found in that stock – even if its price is rapidly approaching $1,000 per share.

That’s why so many analysts remain very bullish about Micron and believe it will outperform the market over the next year, if not longer. Analyst consensus is overwhelmingly “buy” or “strong buy” despite Micron’s all-time high share price.

And that makes Micron an especially intriguing investment.

Are there risks? Absolutely. Every investment comes with some element of risk. Look at, say, BlackBerry (BB), previously known as Research In Motion, which peaked at nearly $150 in June 2008 as the hot new tech item. Its market cap at that time was more than Amazon (AMZN), Nvidia (NVDA), Advanced Micro Devices (AMD), and Netflix (NFLX)… combined. By the end of 2008, BlackBerry was trading for roughly $40 per share. And it can be had today for around $8 per share.

But the bull market for Micron is incredibly strong right now – even stronger than it was for BlackBerry during its time as the world’s smartphone leader.

Between its new status as a trillion-dollar company, its essential role within the AI-driven memory supercycle, and its surging share price, Micron is still seen as a stock on the rise – even when trading at more than $900.

And it may just be a matter of time before Micron reaches $2,500.

Regards,

David Engle

Editor’s note: Forbes calls $1 billion fund manager Louis Navellier “the king of quants.” Today, he’s stepping forward to reveal why he’s investing $358 million of his own firm’s money in the next stage of AI… a technological sea-change that could erase millions of jobs, solve humanity’s biggest mysteries, and spark a wave of moneymaking opportunities — both in and outside the stock market. Click here for the details…