Key Points

- A sharp tech sell-off following the June jobs report underscored the volatility that can accompany investments in AI and semiconductor stocks.

- Many AI and chip companies quickly recovered from the decline, reinforcing the view that long-term demand for AI infrastructure remains strong.

- Although concerns about an AI bubble persist, continued spending on data centers, chips, and related hardware suggests the AI boom may still have room to expand.

All it takes is one jobs report to turn the entire stock market on its head. On Friday, June 5, the Labor Department released its latest report, highlighted by the addition of 172,000 jobs in May. That more than doubled economists’ projections of 80,000.

Just like that, the tech-heavy Nasdaq composite tanked, closing the week ending June 5 at 4.7% lower – its worst week in more than a year – as AI and tech stocks experienced a significant sell-off.

Semiconductor stocks Nvidia (NVDA) and Broadcom (AVGO) dropped 6.2% and 7.9%, respectively, on speculation that demand for AI may be stalling and that higher interest rates – which would significantly increase AI-related spending – could lead to inflation. And they weren’t the only tech giants to take a hit on June 5 – it was absolute carnage.

Naturally, this leads investors and analysts back to the question that has been asked repeatedly over the past three years or so: Is the AI bubble finally set to burst?

AI and Chip Stocks Took a Big Hit Following a Strong Jobs Report

Why were investors spooked enough to sell off their AI and chip stocks following the jobs report?

There were a few reasons:

- Tech companies – especially related to chips and AI – continue to borrow and invest billions in AI and data center infrastructure. If interest rates rise due in part to a rosy employment picture, those tech companies would likely face a huge increase in interest expenses, which would immediately cut into their valuations.

- Many investors and analysts have long subscribed to the theory that the AI bubble will bust sooner rather than later. While those projections have yet to materialize, days like June 5 serve as ominous warning signs that maybe those investors and analysts were onto something. And those doubts hit tech stocks hard that day.

- The surprising job growth in May took some of the bite out of the “AI is coming for all our jobs” doomsday argument.

So, June 5 looked like it might be the day the AI boom started to unravel, and the bubble started to burst.

Tech Stocks Rebounded in a Big Way

It took one whole weekend for that dour sentiment to shift entirely.

On Monday, June 8, just as it looked like AI was on the precipice of a dot-com-like bubble burst, the following occurred:

- Alphabet’s (GOOGL) Google placed an order with Intel (INTC) for more than three million tensor processors in 2028. And Nvidia was exploring whether Intel could create a processor that holds four graphics chips. Intel stock spiked by roughly 11% on the news.

- Marvell Technology (MRVL) shares also increased more than 9% upon news that it was set to join the benchmark S&P 500 Index on June 22.

- Micron Technology (MU) gained nearly 10% as investors bought the Friday dip.

- Amazon (AMZN) signed a multibillion-dollar deal with Corning (GLW) to expand American fiber optic manufacturing for data centers. Corning signed a similar deal with Nvidia last month.

- Cerebras (CRBS) stock rose 3% as multiple Wall Street firms initiated coverage on the stock.

- The iShares Semiconductor Fund (SOXX) jumped nearly 6%.

Suddenly, the AI bubble that was about to burst began reinflating itself. Crisis averted, at least for now.

The Volatility of AI and Tech Stocks Can Be Intense

Was the tech stock mess from June 5 a precursor to the AI bubble finally bursting? Or was it just another day in the life of a tech stock?

History tells us it was much closer to the latter.

Compared with the broader stock market, tech stocks are traditionally more volatile.

The tech-weighted Nasdaq 100 Index has a 10-year annual volatility of roughly 23%. Historically, the S&P 500’s annualized volatility typically falls around 15% to 18%.

Investors ride the roller coaster of huge gains, significant losses, and then repeat the cycle. This pattern is even more pronounced for companies making semiconductors, memory, and AI-related technology.

That’s essentially what we saw on June 5. The jobs report caused the market to turn, resulting in a brutal day for tech stocks. Then, within one business day, most of those tech stocks had recovered much of their losses. It’s simply the boom-bust cycle doing its thing.

Why are tech stocks so volatile? Because they’re often considered “growth stocks.” Investors buy these stocks not for immediate cash dividends but for the future earnings they believe the stocks will generate.

Unfortunately, there’s no way to predict the future, so these stocks are especially sensitive to the country’s rapidly changing economics – inflation, interest rates, corporate earnings, wartime conflicts, and consumer trends. That’s why we see constant fluctuation in tech stocks.

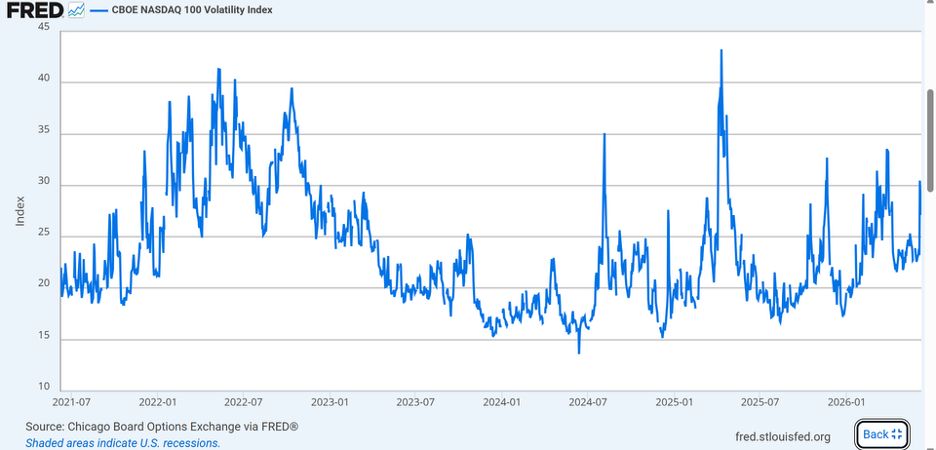

The CBOE Nasdaq-100 Volatility Index (VXN) – known as the tech industry’s “fear gauge” – is a real-time market index that measures the market’s expectation of 30-day volatility for the Nasdaq 100. It doesn’t take an economics expert to see just how volatile tech stocks have been over the past five years, as shown by the VXN.

It’s even more pronounced in the chip, memory, hardware, and AI industries because these categories are extremely cyclical. The market has experienced an AI boom over the past few years – particularly in the aforementioned categories, driven by insanely high demand for AI and data centers.

But as soon as that demand softens – even briefly – we see days like June 5, where those stocks plummet, and companies instantly lose millions, if not billions, in market value.

Broadcom, in particular, had a miserable day. My esteemed colleague James Royal examined its stock decline on June 5, noting:

The reasons behind Broadcom’s sharp decline had less to do with the company’s latest report and more to do with estimates for the current quarter, in which management’s projections for artificial-intelligence (“AI”) chip revenue fell short of expectations.

So, in a quarter where Broadcom generated record revenue, record operating profit, and record free cash flow, the stock lost nearly $300 billion in value. That occurred even as AI-chip revenue surged 143% year over year to $10.8 billion, exceeding the company’s forecast.

But that’s the story in AI now: When you set high expectations, the market comes to expect even more. Excellent results are no longer excellent enough. Instead, they must now be outstanding.

And that’s the rub with AI. Despite record-setting earnings, Broadcom still lost nearly $300 billion in value because of a combination of missed (and perhaps unrealistic) expectations and overreactions.

The massive sell-off on June 5 sure appears to be a result of overreactions. Yes, the jobs report was positive. And, theoretically, that could mean that maybe AI isn’t accelerating at a pace where the global workforce has to be worried yet about losing their jobs to automation.

However, that probably isn’t the case.

But the AI Boom Hasn’t Gone Bust Yet

AI is still in massive demand, despite the jobs report. The June 8 bounce-back strengthened the AI bull argument, and there are very few signs that the AI push will slow down anytime soon, or that we’ve entered the bubble.

“I think if we’re in a bubble, we’re still early stages,” Warren Pies, co-founder of 3Fourteen Research, said to CNBC on June 5. “I think there’s way too much pessimism and worry at this point in time. And the metrics don’t back it up.”

For context, during the peak of the dot-com bubble, 22 stocks grew by more than 400% over the course of a year. Only six stocks in the Nasdaq 100 have experienced similar growth this time around.

But there will always be naysayers. Perhaps chief among them is Julien Garran, a researcher and partner at MacroStrategy Partnership, a U.K.-based firm. Last fall, Garran published a report stating that we are in “the biggest and most dangerous bubble the world has ever seen.”

He went on to say that there is a “misallocation of capital in the U.S.” that makes today’s AI boom 17 times bigger than the dot-com bubble and 4 times bigger than the disastrous 2008 real estate bubble.

His argument isn’t without some merit. According to a July 2025 study by MIT, roughly 95% of businesses invested in AI have not made a profit. So, companies putting money into AI aren’t seeing returns on their investments – which raises the question of whether it’s worthwhile to spend on AI if it’s not going to result in profit.

Paul Kedrosky, a research fellow at MIT’s Institute for the Digital Economy and a venture capitalist, told ABC News that “It’s not particularly unusual for a market at this early stage to not be making much profit. Of course, the difference is most markets at this stage aren’t also spending a trillion dollars.”

Native AI companies like OpenAI, Anthropic, and Cerebras are not yet profitable (though it’s widely anticipated that Anthropic will post its first profitable quarter in Q2 2026). They’re building the models, and they are generating revenue… but they’ve also suffered massive losses that put them firmly in the red.

So, yes, there are logical bear cases to be made regarding AI.

But the tech companies making the hardware and building the infrastructure are turning major profits.

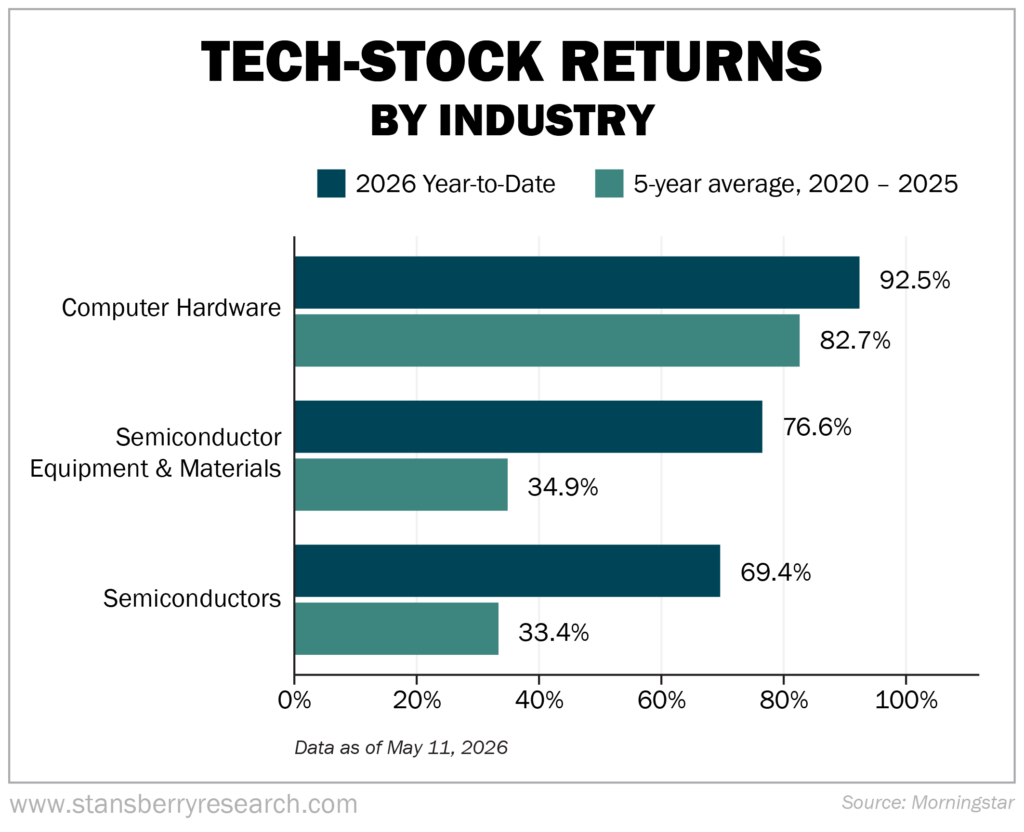

The above categories are clearly on the rise in 2026, which pokes a few holes in the bear argument.

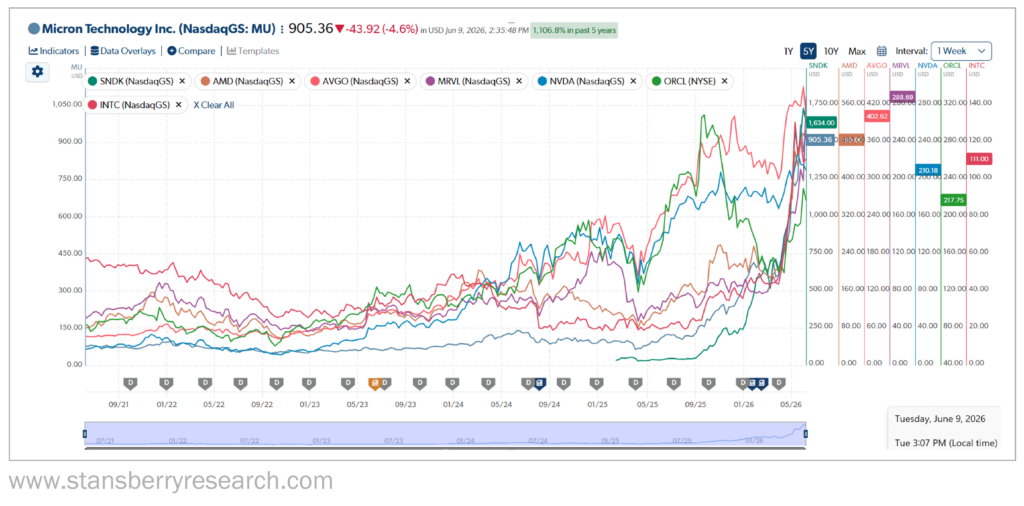

Looking at the five-year performance (less for Sandisk, which spun off in 2025) of the same hardware stocks we examined earlier – Broadcom, Sandisk (SNDK), Nvidia, Intel, Advanced Micro Devices (AMD), Marvell, Oracle (ORCL), and Micron – the growth is clear.

The approximate five-year growth numbers, as of June 8, 2026, are staggering:

- Sandisk: 4,338% (based on the February 13, 2025 relisting rather than five years)

- Nvidia: 1,090%

- Micron: 1,016%

- AMD: 499%

- Broadcom: 747%

- Marvell: 464%

- Oracle: 152%

- Intel: 92%

Despite some valleys, these stocks are trading at or near their all-time highs. Does that portend an AI bubble? Or is it simply evidence of a true boom with even more room to run?

It’s a topic of constant debate, but I point to the real, tangible demand that’s driving the AI bull market. It’s nonstop and seemingly insatiable. Data centers are popping up around the world at breakneck speed. And those data centers need the hardware and equipment these tech companies are manufacturing.

And there doesn’t appear to be a real end in sight. AI is the future until it’s not.

Of course, we don’t know how this will ultimately play out. Maybe AI fizzles out at some point. What we do know is that businesses are investing hundreds of billions of dollars a year in AI. And that means the tech companies providing the necessary components – and those investing in those companies – will continue to thrive.

But, as we saw in the span of just four days in June, you can expect some bumps and volatility along the way.

Regards,

David Engle

Editor’s note: Will AI crash the stock market? Every bubble in history eventually bursts, and Marketwise CEO Dr. David “Doc” Eifrig believes this AI bull market is no different.

But his team’s research suggests the more important question isn’t “if,” but “when” – and they’ve discovered the exact quantitative signal that has ended every bull market, including this one.

What makes this research particularly interesting: Doc and his team recommend you take three specific steps now that could make the next year the most profitable of your life – and show you when to get out. See his full presentation here.