Key Points

- Since hitting their peak in early June, solar stocks have slumped for a variety of reasons.

- Despite a recent slide in share price, First Solar continues to outperform fundamentally, posting strong revenue, earnings, and margins while maintaining a massive 47.9 GW contracted backlog.

- Analysts remain bullish on First Solar’s long-term outlook thanks to its U.S.-based manufacturing, lack of dependence on imported polysilicon, and growing demand for utility-scale solar to power AI infrastructure.

Solar energy stocks have pulled back sharply in recent weeks despite growing AI-driven electricity demand, as policy changes, expiring tax incentives, high interest rates, and global oversupply have weighed on the sector.

It wasn’t even three months ago that we were feeling pretty optimistic about solar stocks. In his May 6 Money & Megatrends newsletter, MarketWise’s Brian Hunt had this to say about solar:

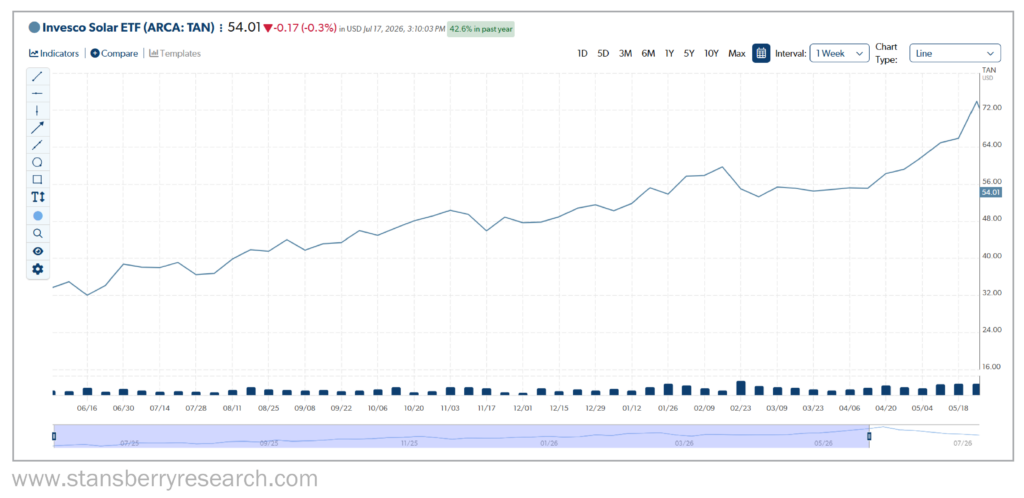

Over the past 10 trading sessions, the Invesco Solar ETF (TAN) has surged 11% and reached new all-time highs.

This upswing makes solar energy one of the world’s top-performing themes right now…

It’s a bull market in virtually every form of electric power production… including the one that gets free fuel from the sun.

Brian was absolutely right. The Invesco Solar ETF soared 124% between June 2, 2025 and June 2 of this year, and set multiple record highs in the process.

By July 13 of this year, the Invesco Solar ETF had plunged 27% in the span of roughly 45 days.

Industry leader First Solar (FSLR) certainly hasn’t been immune to the headwinds the entire solar sector is facing. First Solar’s stock is down nearly 20% since the start of the year. But the stock hasn’t fallen out of favor because of declining sales.

First Solar Is in Excellent Financial Shape… Even If Its Stock Isn’t

First Solar enjoyed an outstanding first quarter of 2026, with record net sales of just over $1 billion – jumping by 24% year over year. The company’s net income increased an impressive 65% year over year to $347 million, and its diluted earnings per share beat estimates at $3.22. Gross margin also grew by 6 percentage points to 47% compared with a year ago.

Just as importantly, First Solar maintained a contract backlog of 47.9 gigawatts (“GW”), ensuring substantial revenue through the end of the decade.

Interestingly enough, First Solar seemingly beat its own expectations in the first quarter of 2026. Its initial full-year guidance hinted at the possibility of no sales growth and even revenue decline.

First Solar’s second-quarter earnings will be announced on July 30, so we’ll see how the company performed against its impressive first quarter.

Despite the company’s financial success, however, First Solar stock continues to fall from its early-June all-time high. Its stock price has plunged by just over 30% since June 3. But it’s far from the only solar stock to take a significant hit during that time.

SolarEdge Technologies (SEDG) fell by 33%, while Enphase Energy (ENPH) dropped 38%, and Sunrun (RUN) dipped 16% since June 3.

Which prompts a couple of questions. Why did solar stocks surge to multiyear highs in early June? And why such a precipitous drop since then?

The Late-Spring/Early-Summer Rise and Fall of Solar Stocks

Of course, as the increasingly brutal summer heat and humidity set in, energy demand rises as Americans fire up their air conditioners.

But the main catalyst behind the surge in energy demand and the subsequent stock price increase, which shouldn’t come as much of a surprise, is artificial intelligence (“AI”). Power grids remain strained by AI data centers, meaning operators and hyperscalers must secure reliable energy sources.

Solar has stepped up to fill that void, with tech giants such as Alphabet (GOOGL) and Meta Platforms (META) locking into long-term Power Purchase Agreements (“PPAs”) with solar companies. These contracts – and AI’s insatiable thirst for energy – prompted analysts to upgrade their price targets and make bullish cases for solar stocks.

First Solar benefited not only from data centers’ constant need for energy, but also because of the U.S. Department of Commerce’s Section 232 investigation into imported polysilicon and the possibility of per-watt tariffs being imposed on the material.

That’s because First Solar does not use any polysilicon in its products. This fully shields the company from any material trade war while keeping its prices in check relative to competitors that import silicon for their products.

This explains why analysts have been so bullish on First Solar. The stock’s price target received at least five upgrades in 2026:

- GLJ Research: Upgraded from hold to buy, increased price target from $207.82 to $315 in late May.

- UBS: Raised its price target from $290 to $330 on June 11.

- Deutsche Bank: Upgraded from neutral to buy, increased price target from $245 to $272 on July 6.

- Wells Fargo: Increased its price target from $255 to $320 on July 6.

- Barclays: Raised its price target from $213 to $279 on July 13.

Here’s where the picture becomes a bit blurry, however. Although First Solar has gotten several price target bumps from reputable analysts, its stock price has been falling for weeks. Since its high of just over $320 on June 4, First Solar’s stock has lost just under $100 per share.

So, why are analysts so bullish on First Solar (and other solar companies) when their stocks continue to tumble?

Four Reasons Why Solar Stocks Are Falling

It’s important to understand the key reasons solar stocks have been falling to make sense of why analysts remain optimistic about the solar sector.

1. Trump’s Tax Bill Removes Crucial Renewable-Energy Incentives

In mid-June 2025, the Senate passed a version of President Donald Trump’s One Big Beautiful Bill, which included provisions to completely eliminate renewable-energy tax incentives by 2028. The bill puts solar and wind power tax incentives squarely in its crosshairs… obviously devastating news for the renewable-energy sector.

What makes this policy shift even harder for the sector to swallow is that the bill gives its full support to other energy sources – hydropower, geothermal, and nuclear.

Compound that with significant U.S. tariffs on solar panels and components imported from Southeast Asia (a combined 35% to 55%), and it’s easy to understand why the solar industry has suffered.

The Trump administration seems to be doing whatever it takes to cut back on renewable energy in America. And that’s already made a significant negative impact on solar and renewable energy stocks.

2. Expiration of Residential Solar Tax Credits

When Trump signed the tax bill into law last July, the Residential Clean Energy Credit (Section 25D) began its countdown toward extinction. This credit, which offered a 30% tax break on home solar installations, was a massive incentive for homeowners to invest in renewable energy.

The expiration of that credit at the end of 2025 has softened demand in residential solar installations. Market research firm Ohm Analytics expected second-quarter solar interconnections to decline by more than 25% year over year, with a full-year installation decrease of 22%.

Companies specializing in residential solar installations are feeling the pressure.

Enphase announced earlier this year that it would slash 6% of its workforce. Freedom Forever, the second-largest residential installer in the U.S., stopped doing business in one-third of its state markets and laid off roughly 20% of its employees in the process. Then it filed for bankruptcy in May. Several small solar installers followed suit.

3. High Interest Rates

Most homeowners and businesses can’t simply shell out the tens of thousands of dollars it takes to install a solar energy system. It’s an investment that typically requires financing. Today’s high interest rates are a major detriment to those types of investments.

Between the elevated rates and the tax credit expiration, residential installation companies are in dire straits. Sunrun, the leading solar installer in the country, experienced steep losses in the first quarter of 2026. Year over year, new subscriber count was down 25% year over year, added energy-storage capacity fell by 15%, and added solar capacity dropped 19%.

4. Massive Solar Panel Oversupply

China currently manufactures more than 80% of the world’s solar panels. And, because of the factors we’ve covered here as well as intense manufacturer competition within the country, they’re stuck with a huge oversupply. The glut is so significant that China is actively working to cut back on production and ease the solar-panel oversupply problem.

This obviously impacts the manufacturing side of the solar industry. With solar panel prices so low because of the oversupply, manufacturers must lower their own prices, which squeezes margins and impacts their stock prices.

Why Analysts Remain Bullish on Solar Despite Sagging Stock Performance

Despite the Trump administration’s push for more fossil-fuel energy, many analysts still believe that cheaper and cleaner solar power will remain in high demand as AI data centers continue to strain power grids across the country.

Besides the advantages of cheaper, cleaner power, solar plants typically require far less construction time (around 18 months) than, say, a natural gas plant (three to five years). This is crucial considering the current grid strain. Traditional power plants simply can’t be built quickly enough to handle today’s energy demand.

And though the Trump administration has handcuffed solar businesses with cost-prohibitive tariffs on imported solar components and sweeping incentive rollbacks, those actions are starting to increase domestic solar production, which is certainly an intended consequence.

Plus, despite the many renewable energy cuts in Trump’s One Big Beautiful Bill, the legislation did keep the Inflation Reduction Act’s full Section 45X solar manufacturing credits through 2032, as well as incentives for battery storage, designed to spur American solar production.

As for interest rates, the Federal Reserve recently held its benchmark range steady and said it doesn’t anticipate any cuts until sometime in 2027 at the earliest. That means solar customers are still facing elevated interest rates when financing any solar installation.

But, as I noted with First Solar’s price target increases, analysts are still expecting big things not only from First Solar, but also from other solar businesses as well, in the coming months.

The Solar Stock Outlook for Investors

The solar industry is notoriously volatile, adding an underlying element of risk to any solar stock. The industry’s beta – which measures a stock’s volatility – is significantly higher than the broader market.

For example, the Invesco Solar ETF beta, which held positions in 31 stocks as of March 31, has a five-year monthly beta of 1.85. That means its stocks are roughly 85% more volatile than the total stock market.

As of July 15, First Solar’s five-year monthly beta is 1.73, Sunrun’s is a staggering 2.32, SolarEdge’s is 1.45, and Enphase’s is 1.62. So, if you’re considering investing in solar, buckle your seatbelt… It’s going to be a bumpy ride.

At face value, there’s no logical reason to invest in solar stocks in the current climate. They simply haven’t performed well in weeks. A clean-energy analyst at Guggenheim Securities went so far as to call the solar industry a “zero-growth sector” as recently as May.

But beneath the surface, there’s a strong case to buy the dip, if you will. One reason is that some solar companies have pivoted to counter the headwinds they’ve experienced due to policy changes, oversupply concerns, and high interest rates.

SolarEdge, for example, is looking toward Europe to boost its revenue, as the war in Iran has significantly increased European energy prices due to reliance on oil that flows through the Strait of Hormuz.

And battery storage is a path that solar companies have emphasized, since those tax credits remain available for the next six years. Sunrun, which boasts a massive national home battery network, could be a major beneficiary of this type of strategy shift.

But the fates of most solar companies in the U.S. rest on Trump’s decision regarding the Department of Commerce’s Section 232 investigation into imported polysilicon. If Trump decides to impose tariffs or quotas on foreign polysilicon, the solar supply chain will be in trouble. And so are some American solar installers who rely on imported solar panels, as well as American solar consumers. Solar installations will simply become too expensive.

For companies like First Solar, however, imported polysilicon tariffs would represent a colossal win. Like I mentioned, First Solar – unlike many domestic solar manufacturers – does not use polysilicon in its products. That ensures costs will remain stable while other manufacturers may face skyrocketing supply costs.

Keep an eye on an upcoming Section 232 decision on imported polysilicon from the president in early August, as it will likely shake up the solar market either way.

If you’ve made it this far, you can clearly see how volatile and highly dependent on policy and global trade the solar industry is. But even as stock prices fall, analysts remain generally optimistic about the solar sector’s long-term outlook, especially First Solar’s.

Despite disappointing 2026 sales guidance that fell below expectations, First Solar still beat first-quarter revenue and earnings-per-share estimates while maintaining (not decreasing) its full-year sales guidance.

Plus, it has that huge 47.9 GW contracted backlog to fall back on for the foreseeable future. And, perhaps most importantly, it is not dependent on the Chinese supply chain, which could face enormous problems in just a couple of weeks. These factors all make First Solar stock one of the safer bets in a highly fickle industry.

Regards,

Editor’s Note: A new “dark energy” is being rolled out as we speak… It completely bypasses our need for foreign oil. And it’s not nuclear or solar or wind or anything you would expect.

This new potential $10 trillion technology is already seeing investment by early backers of Microsoft, Google, Amazon, and more… Most important, these dozens of billionaires can’t make this tech themselves. They have to go through obscure “supplier” companies.

And in the coming months, this new “dark energy” could send three little-known stocks soaring… while wiping out 10 of the most popular stocks on the market. Learn more about this dark energy opportunity by clicking right here.