Image Credit: Associated Press

Listen to the audio version of this article (generated by AI).

Key Points

- Amazon plans to raise $25 billion through a bond sale to help fund nearly $200 billion in AI-related capital spending, including AWS expansion, custom AI chips, and new data centers.

- Amazon Web Services continues to support the investment case with 28% year-over-year revenue growth, a record $364 billion backlog, and consistently strong operating margins.

- Despite taking on more debt, Amazon maintains a strong balance sheet and AA credit rating, positioning the bond offering as a strategic investment in long-term AI growth.

Amazon (AMZN) expects to spend $200 billion in capital expenditures (“capex”) this year, with much of it going toward artificial intelligence (“AI”) and Amazon Web Services (“AWS”), Amazon’s massive cloud-computing platform.

For a company that boasts a market capitalization north of $2.6 trillion, it would be easy to assume that $200 billion is a drop in the bucket for Amazon. That clearly isn’t the case, because Amazon is looking to raise at least $25 billion through a bond sale to fund more spending on its AI infrastructure, as reported by Bloomberg on July 7.

If roughly $200 billion sounds like a lot of money to invest in AI, well, it is.

And it’s more than any other company is projected to spend in 2026. More than Alphabet (GOOGL) and Microsoft (MSFT), both of which expect to invest around $185 billion to $190 billion this year. It’s also significantly more than Meta Platforms (META), which may spend up to $145 billion.

This raises a few questions.

- Why does a company as wealthy as Amazon need to raise money through bonds to fund its AI-infrastructure spending?

- What specifically is the $200 billion in capex (as well as the $25 billion in bond sales) funding?

- How does raising funds through capital markets impact Amazon’s cash flow and bottom line down the road?

- What should investors take away from this most recent debt raise?

Why Amazon Is Turning to Bond Issuance to Fund AI Spending

The simple answer: AI infrastructure is astronomically expensive to build out. And it’s becoming increasingly necessary to keep spending to stay ahead of the competition.

Amazon CEO Andy Jassy said as much in his April shareholder letter, in which he stated:

We’re not investing approximately $200 billion in capex in 2026 on a hunch… We’re not going to be conservative in how we play this [AI build-out] – we’re investing to be the meaningful leader, and our future business, operating income, and [free cash flow] will be much larger because of it.

Even the world’s richest companies – like Amazon, Nvidia (NVDA), Alphabet, and Meta – have spending limits. And all those mega-cap businesses have leveraged debt at some point to finance their AI build-outs. In less than a year, for example, Meta has raised roughly $55 billion from two bond sales.

It’s almost a must at this point.

Consider AI capex in 2025. Last year, the four major hyperscalers (Amazon, Microsoft, Meta, and Alphabet) spent a combined $410 billion on AI capex. This year, that number is expected to pass $725 billion – a roughly 77% increase.

By the end of next year, these four companies are likely to spend more than $1 trillion to expand their AI infrastructure.

Amazon spent roughly $105 billion on AI capex last year. This year’s expenses should nearly double that figure. Which makes sense, given the overall increase in AI capex.

It’s true that Amazon is flush with cash. Its trailing-12-month (“TTM”) revenue (ending March 31, 2026) was nearly $743 billion. But, during the same period, the company’s operating cash flow was roughly $148.5 billion, and its capex was $151 billion. That’s a free cash flow (“FCF”) of nearly negative $2.5 billion.

In other words, Amazon has been spending a ton. Thus, the decision to raise billions by selling bonds can help soften the spending blow.

It’s a strategy that has worked for Amazon before. The company raised around $54 billion in bonds in Europe and the U.S. earlier this year. Amazon also pulled in $14 billion in Canadian-dollar ($10 billion in U.S. dollars) bonds last month and another $15 billion from a U.S. bond sale last November.

So, while Amazon technically doesn’t need to raise debt to fund its AI expenditures, it certainly doesn’t hurt.

What Amazon’s $200 Billion in Capex Will Pay For

Amazon Web Services will receive the bulk of the money to build out the company’s physical and digital AI infrastructure as the demand for AWS continues to rise.

After the first quarter of 2026, AWS continued to lead all global cloud-infrastructure service providers in market share at 28%, followed by Microsoft Azure at 21%, and Google Cloud at 14%.

To maintain that edge, it’s imperative for Amazon to continue pouring resources into expanding AWS’s offerings and capabilities.

This includes spending on the construction and expansion of physical data centers – as well as the necessary networking equipment and hardware (such as Amazon’s multibillion-dollar deal with Corning) – to meet demand for AWS and cloud services.

Part of this capex will go toward the $12 billion Amazon is spending to build new data centers in central Mississippi. And some of that capex will fund the development and production of Amazon’s proprietary Trainium, Inferentia, and Graviton chips to handle internal AI workloads and to sell to other companies.

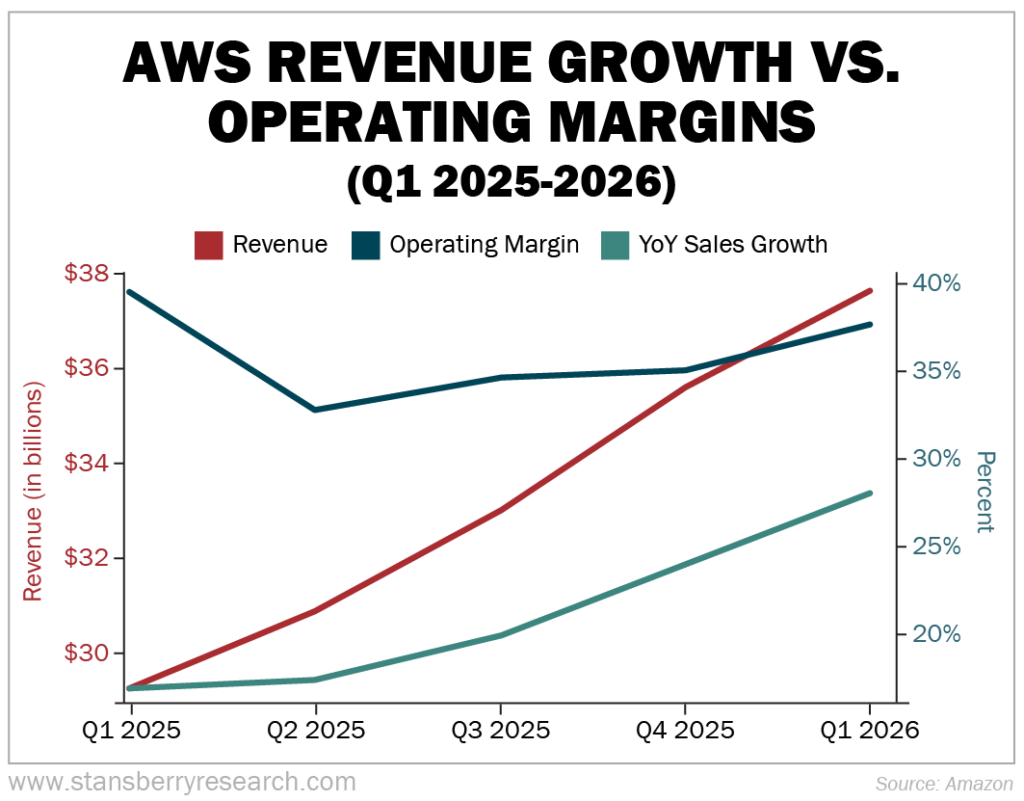

The significant investment in AWS is a no-brainer. Revenue has grown steadily since the first quarter of last year, from $29.3 billion to $37.6 billion in 2026’s first quarter.

Just as important, throughout this revenue growth, AWS has maintained steady operating margins of between roughly 33% and 40%, demonstrating that AWS is successfully managing AI demand without losing profitability.

So, it makes plenty of sense for Amazon to funnel most of its projected capex in 2026 toward AWS and AI infrastructure.

How Amazon’s Bond Sales Impact Earnings

At the end of the first quarter, Amazon’s total debt was roughly $119 billion, up 81% from the previous quarter.

The company’s recent bond sales add to that overall debt. But, because Amazon is borrowing money to help fund its massive capex, those bond sales also help the company’s bottom line by eliminating the need to spend huge amounts of cash up front. This helps preserve Amazon’s net income and FCF.

As I mentioned, bond sales have become an increasingly popular method of raising capital in the tech industry. In 2026 alone, worldwide AI-related bond sales have reached roughly $335 billion – more than double 2025’s sales. That figure is expected to reach $570 billion by the end of the year.

That could also explain why demand for Amazon’s latest bond sale wasn’t all that strong. This offering’s peak demand hit roughly $62 billion… around half of what it received during its bond sale in March.

Amazon has said internally (though not publicly) that its most recent $25 billion bond sale will be the company’s last debt issuance of the year, according to CNBC. Which looks like a wise decision.

There are clearly signs of investor fatigue, given the massive amounts of AI- and tech-related debt saturating the market today. Even so, and despite Amazon’s issuance of more than $100 billion in bonds over the past year, the company’s bottom line remains in excellent shape.

S&P Global Ratings gives Amazon a strong AA credit rating thanks to its robust $90.8 billion TTM net income and its outstanding 0.43 times net-debt-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio.

Amazon firmly believes that taking on debt now to finance its AI and AWS build-out will pay off in a big way over the long term. In justifying the company’s exorbitant AI-related capex, CEO Jassy called AI a “once-in-a-lifetime opportunity” that will “yield strong returns on invested capital.”

Jassy also noted that Amazon already has customer commitments that will cover “a substantial portion” of its AI capex and that most of it will be monetized in 2027 and 2028.

How Amazon’s Most Recent Debt Raise Impacts Investors

The fact that Amazon is spending more on AI capex – and raising some of that capital through bond sales – is a positive sign, in my opinion. That’s because Amazon’s need for increased AI spending is strongly driven by the company’s huge $364 billion AWS-cloud-revenue backlog, including Amazon’s recent $100 billion deal with Anthropic.

As strong as Amazon’s AI business has been over the past few years, the value of the 2026 AWS backlog is a company record, and it guarantees nearly half a trillion dollars in future contract closings. That goes a long way toward offsetting – and then some – the growing capex.

In fact, AWS revenue increased 28% year over year during the first quarter of 2026, its fastest growth in nearly four years, hitting an annualized run rate of about $150 billion.

That rare combination of growth rate and sheer revenue volume is huge for Amazon, and it illustrates why AWS is the largest cloud-computing business in the world.

But AWS is far from the only revenue-generating machine for Amazon. Its custom chip business, which produces Trainium AI chips, Graviton processors, and Nitro architecture, boasts an annualized run rate of more than $20 billion. Jassy noted that this division is “growing triple-digit percentages” each year.

If you’re considering investing in Amazon, or already do, don’t let the capex or the bond sales scare you off. AWS is in high demand, and that won’t change for the foreseeable future. Amazon’s big spending on AI will only strengthen AWS’s offerings and expand its reach.

Yes, it’s true that Amazon stock has been a bit sluggish of late, down just over 10% (as of market close on July 9) from its 2026 closing high on May 6. But it’s also true that Amazon is 11% higher over the past year.

Let’s also keep in mind that, besides AWS’s outstanding performance, Amazon’s other business segments are performing incredibly well. The company’s list of 2026 first-quarter earnings highlights alone feels like a 10-minute read. Some of those include:

- New AWS agreements with dozens of businesses and organizations.

- The launch of Amazon Bio Discovery, an agentic-AI application designed to accelerate drug discovery.

- The launch of Health AI, a 24/7 AI-powered personal health agent on Amazon’s U.S. app.

- More than $600 million in global box office sales for Amazon MGM Studios’ Project Hail Mary film.

- The 10th launch of Amazon Leo satellites, bringing the total in orbit to more than 250.

- The news that Amazon Leo will power satellite services for Apple’s (AAPL) iPhone and Apple Watch, as well as provide Wi-Fi for hundreds of Delta Air Lines (DAL) aircraft starting in 2028.

In the first quarter of 2026, Amazon also grew its TTM advertising revenue to more than $70 billion. Amazon’s net sales totaled more than $181.5 billion, and its operating cash flow was up 30% year over year.

Plus, Amazon is projecting net sales to jump between 16% and 19% to a range of $194 billion to $199 billion in the second quarter.

Of course, there’s the matter of Amazon’s FCF, which plunged 95% year over year (but was still positive at $1.2 billion for the first quarter). But, again, that’s a direct result of the massive increase in AI spending.

At the end of the day, yes, there is a substantial amount of risk that comes with investing $200 billion in AI. But Amazon didn’t become one of the five most valuable companies in the world without taking some big swings.

Look no further than AWS and Amazon Prime. Both were considered risky ventures at the outset. Now they’re two of the biggest drivers of Amazon’s revenue.

Big spending can be an investment that pays off in the future to maximize an emerging opportunity.

When a “once-in-a-lifetime opportunity” (as Andy Jassy put it) presents itself, sometimes significant spending is the best investment. Especially if you firmly believe it will pay off in the future. Amazon is sticking to that philosophy, and there’s a better-than-good chance it will pay off for investors.

Regards,

David Engle

Editor’s Note: Whitney Tilson called the rise of Apple, Amazon, and Netflix… as well as the collapse of dozens of companies that went bankrupt. Now the former $200M hedge fund firm manager is stepping forward with what he calls the most important financial warning of his 30-year career. He’s sharing two free stock recommendations (one to buy, one to sell immediately) along with details of a new proprietary system fueling his predictions. See it all in his free presentation.