Image Credit: Associated Press

Key Points

- Intel stock has surged more than 360% over the past year, driven by CEO Lip-Bu Tan’s turnaround strategy, improved execution, and renewed investor confidence.

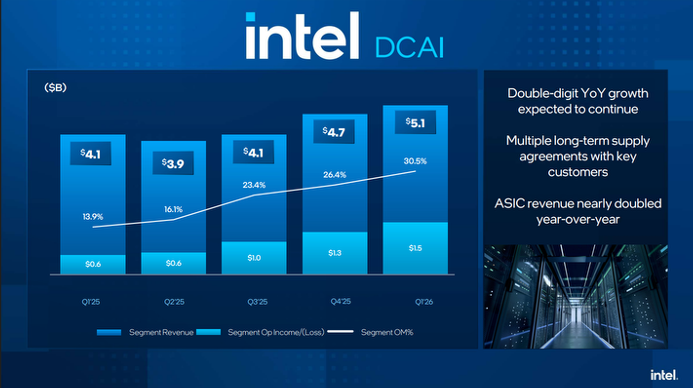

- The company is gaining traction in AI and data centers, with first-quarter 2026 revenue in that segment rising 22% year over year to $5.1 billion.

- Despite the rebound, Intel still faces key risks, including operating losses, strong competition, and a valuation that may already reflect near-perfect execution.

Intel (INTC) looked dead in the water just a year ago. The once-formidable semiconductor manufacturer’s stock hit an intraday trading low of $17.67 on April 8, 2025, Intel’s lowest price since July 2009.

And that freefall was warranted. Between massive employee layoffs and huge losses in its foundry business, Intel was floundering. Its competitors, like Nvidia (NVDA), Taiwan Semiconductor Manufacturing (TSM), and Advanced Micro Devices (AMD), were so far ahead that they weren’t even on the company’s radar anymore.

But new CEO Lip-Bu Tan, who was appointed in March 2025, wasn’t going to let Intel go down without a fight. At this time last year, Intel closed at $19.98. On April 30, Intel’s stock closed at $94.48, up around 373% from the previous year.

What exactly spurred Intel’s turnaround, and what is the company’s outlook moving forward? Let’s break it down.

Intel’s Long and Rough Road

To truly appreciate the strides Intel has made in the past year, it’s important to understand the depths it has reached.

Intel’s issues stretch back to the late 1990s, when strategic misses began to derail the company.

Here’s a look at some of the company’s major missteps:

- Intel missed the boat on developing graphics processing units (“GPUs”) in the 1990s. GPUs are now a critical component of AI accelerators – the technology that speeds up AI tasks and allows generative AI to run.

- In 2007, Apple (AAPL) approached Intel about supplying chips to power the first iPhone. Intel’s then-CEO, Paul Otellini, passed on the opportunity because he wasn’t sold on the iPhone. So, Apple turned to chips made by Arm Holdings (ARM). Today, Arm’s technology powers more than 99% of the world’s smartphones.

- Fast-forward another decade, when Intel failed to create good enough processors to compete with rivals such as Advanced Micro Devices, Nvidia, Samsung Electronics, and Taiwan Semiconductor, ultimately pushing Intel into near irrelevance.

- In 2017, former CEO Bob Swan declined an offer to acquire a 15% stake in OpenAI for roughly $1 billion. This deal would’ve placed Intel at the center of the AI boom from day one. Besides costing Intel billions over the past decade, the decision blew Intel’s opportunity to become an AI pioneer while sabotaging any future business with OpenAI.

The aftermath of Intel’s miscalculations was ugly.

In July 2025, the company announced it was cutting its workforce by more than 25,000. This followed more than 15,000 layoffs in August 2024.

Intel also canceled plans to build factories in Poland and Germany last July. And the company again delayed construction on its two Ohio fabs, with expected completion dates now pushed to between 2030 and 2032.

Then, later in 2025 and into 2026, everything suddenly began to change for Intel.

MORE: Can Micron Reach $1,000? AI Memory Chip Demand Has Analysts Bullish

Intel’s Stunning Turnaround Story Under Tan’s Leadership

It’s difficult to pinpoint any single event or decision that prompted Intel’s reversal of fortune. But it’s safe to say that better overall strategy and decision-making, led by Tan, has played a pivotal role.

Since Tan came aboard in March 2025, he has been laser-focused on improving margins (which was, in part, accomplished by the massive 2025 layoffs), becoming a key player in the AI data-center realm, maximizing yields for its advanced 18A and 14A process nodes, and resurrecting Intel’s foundry business.

Perhaps one of the earliest signs of an Intel turnaround came in August 2025, when the company ceded 10% of its non-voting shares (valued at more than $11 billion) to the United States government in an effort to prop up the American chipmaker.

I wrote about the potential benefits of the Intel-U.S. government agreement on September 10:

Favoring Intel is President [Donald] Trump’s personal involvement with the agreement… It’s difficult to envision him or his administration allowing Intel to fail.

The White House has all the motivation in the world for Intel to succeed. And Intel gained new capital as a result of the deal. All things being equal, that’s never bad.

With the government seemingly all-in on Intel, there is certainly some reason for optimism. If there’s one thing Donald Trump hates, it’s being wrong… So, expect the White House to do everything in its power to make Intel successful again.

But, under Tan’s guidance, Intel has achieved even more since this government deal was made.

AI Data-Center Business

Tan has stated that Intel is locked into “multiple long-term supply agreements with key customers” for the data-center business. Among them is Google, which Tan believes is a key to success for Intel regarding AI infrastructure.

In the first quarter of 2026, Intel saw its Data Center and AI (“DCAI”) revenue increase 22% year over year to reach $5.1 billion. This was driven by increased demand for the company’s Xeon server central processing units, which are frequently used in AI data centers for both agentic and inference workloads.

While not directly related to data centers, Intel’s Client Computing Group revenue reported $7.7 billion in first-quarter 2026 revenue, a modest 1% year-over-year increase. The primary driver was demand for Intel’s AI PC chips. In fact, Intel labeled the launch of its Core Ultra Series 3 processors the best in five years for the company.

MORE: Best AI ETFs: 7 Top Funds for Artificial Intelligence

18A and 14A Process-Node Production

Intel began high-volume manufacturing of its 18A process nodes late last year. By January, the company had released its Core Ultra Series 3 processors (Panther Lake), the first commercial products built on 18A.

And its Xeon 6+ processors on 18A should launch within the next couple of months.

But perhaps the most exciting node-related development for Intel is this: Its 14A process will likely be the first ever to use ASML’s next-level high NA EUV (high numerical aperture extreme ultraviolet) lithography machines to create sub-2-nm (nanometer) AI chips, high-end processors, and GPUs sometime in 2027 or 2028.

This is massive news for Intel, as it positions the company to gain a competitive edge in chip production.

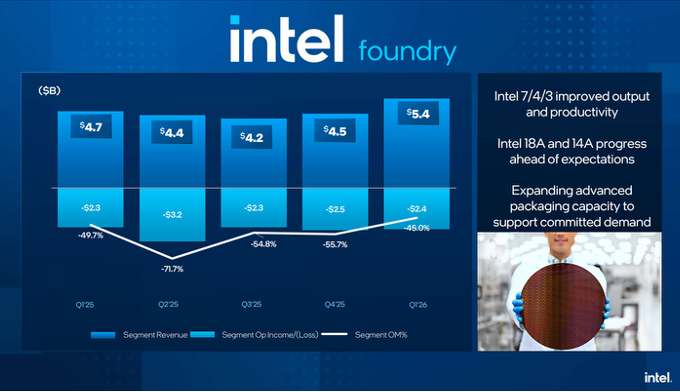

Intel’s Foundry Revival

In 2022 and 2023, Intel Foundry Services (“IFS”) earned external foundry revenue of $895 million and $952 million, respectively.

IFS revenue then exploded to $17.5 billion in 2024 and increased to $17.8 billion last year. The pattern continued into 2026’s first quarter, with Intel’s foundry business earning $5.4 billion, a nearly $1 billion jump from the previous quarter.

What sparked such a drastic revenue surge?

- Intel began manufacturing its own products, including the Core Ultra Series 3 and Xeon 6 processors, rather than having them manufactured by Taiwan Semiconductor.

- The AI data-center boom pushed demand for Intel’s Xeon processors to unprecedented levels.

- Intel’s application-specific integrated circuit (“ASIC”) custom chip business increased by more than 50% thanks to demand from cloud customers.

- EUV nodes accounted for more than 10% of IFS’ 2025 revenue, up from less than 1% just two years prior.

And what might be the best news Intel has received in some time – Elon Musk recently confirmed that his SpaceX/Tesla/xAI Terafab project will use Intel Foundry’s 14A fabrication technology.

During Tesla’s (TSLA) first-quarter 2026 earnings call, Musk said, “We plan to use Intel’s 14A process, which is state of the art and in fact not yet totally complete. By the time Terafab scales up, 14A will be probably fairly mature or ready for prime time.”

Musk added that “14A seems like the right move and we have a great relationship with Intel, a lot of respect for the CEO, the CTO, and the new team there.”

I wrote about Intel’s partnership with Musk on April 13 and noted the immediate impact the announcement had on Intel’s stock:

On April 6, Intel closed at $50.78. The next day, when the Terafab announcement was made, Intel closed at $52.91, a jump of more than 4%. The following day, April 8, Intel shares closed at $58.95, an increase of more than 11% from the day before and roughly 16% higher than April 6…

Assuming the Terafab project moves along as planned, Intel should benefit from what could be a massive production output and long-term revenue gain over the next several years…

Musk’s stamp of approval could go a long way toward revitalizing Intel’s struggling foundry business. After all, if Elon Musk wants your product, it stands to reason that other companies will follow suit.

There’s little doubt that the Terafab deal will have a long-term positive impact on Intel’s foundry business.

A Closer Look at Intel’s Stock

The first quarter of 2026 marked Intel’s fourth straight quarter of increasing revenue (and sixth consecutive quarter of revenue exceeding expectations) and earnings.

Intel’s total first-quarter highlights included:

- Revenue of $13.6 billion, up 7% year over year

- Non-GAAP (generally accepted accounting principles) gross margin increased 1.8 percentage points to 41%

- Non-GAAP earnings per share (“EPS”) of $0.29, up $0.16 year over year and $0.29 over January’s outlook

- Double-digit AI business growth year over year

Looking ahead to the second quarter, Intel is projecting a revenue midpoint of $14.3 billion (a $1.4 billion year-over-year increase), 39% non-GAAP gross margin (up 9.3 percentage points year over year), and $0.20 EPS (up $0.30 over last year).

The string of quarterly successes has obviously translated to Intel’s stock performance in a big way.

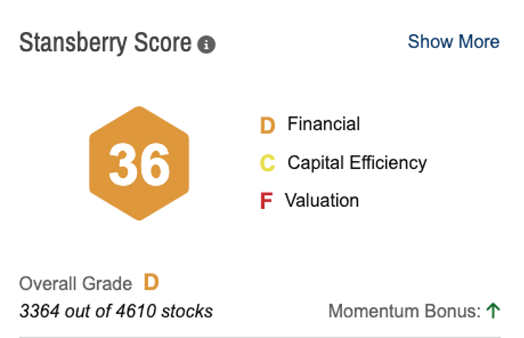

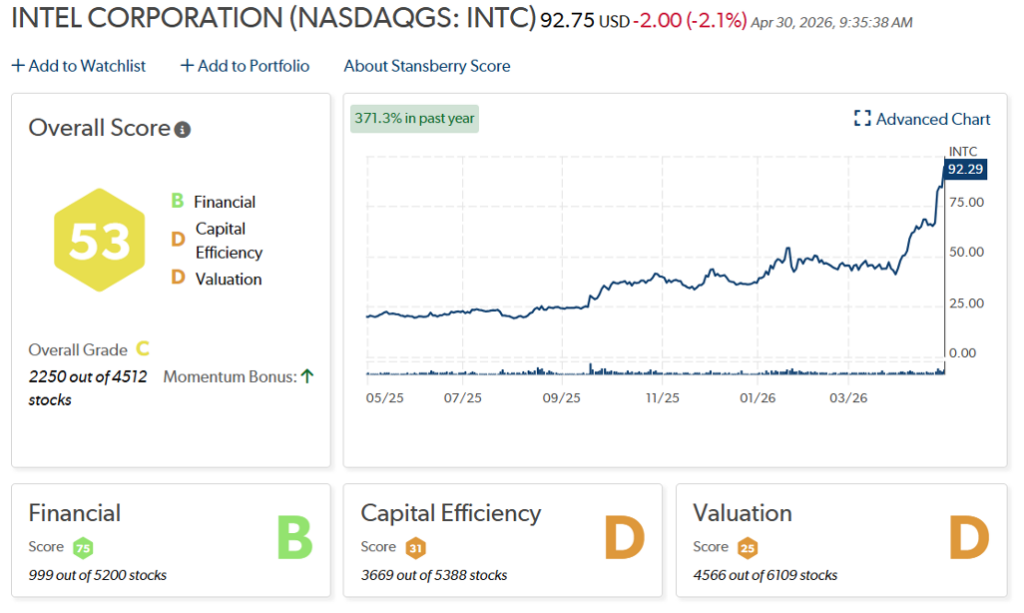

Using Stansberry Research’s Stansberry Score, a tool that helps determine the quality and long-term value of thousands of stocks, we can see Intel’s recent upward trajectory in a couple of key categories – Financials and Valuation.

When I wrote about Intel in September, Intel’s Stansberry Score was, well, abysmal.

At that time, Intel’s stock was graded a “D” – ranking 3,364th out of more than 4,600 overall stocks.

By the end of April, Intel improved its score to an overall “C” grade while moving up more than 1,100 spots to rank 2,250th out of 4,500-plus stocks.

Is this enough to consider Intel a great stock to own?

There are some areas of concern that investors should weigh carefully.

Intel continues to face key risks and challenges, even as it moves forward with its impressive turnaround.

- Intel still incurs significant operating losses despite receiving government subsidies. For example, even with the recent gains in its foundry business in 2025, Intel reported operating losses of $2.2 billion last year. That contributed to Intel’s more than $1.6 billion in negative free cash flow, as did roughly $11.2 billion in capital expenditures to build new fabs and equipment (a justifiable investment). In the first quarter of 2026, Intel’s foundry business reported another $2.4 billion in operating losses.

- As of April 30, Intel’s forward price-to-earnings (P/E) ratio was 93.76 times, which is extremely high. Considering Intel stock was trading at roughly $93 on April 30, its valuation is also quite high (hence the “D” for Valuation in its Stansberry Score), suggesting that Intel is considerably overvalued right now. That means Intel will have to perform at a near-perfect level in the coming months to sustain its current trajectory.

We can’t look at Intel in a vacuum. Has it improved upon its own performance? Yes. Is the stock performing well? Yes, it is. Has Intel’s performance really moved the needle among its competitors or been enough to warrant the hype? That’s a different story.

Sure, its first-quarter 7% year-over-year revenue increase and 41% non-GAAP gross margin are solid numbers. But Advanced Micro Devices projects 32% year-over-year revenue growth and a non-GAAP gross margin of 55% in the first quarter of 2026. Taiwan Semiconductor reported a 40.6% year-over-year revenue increase in the first quarter of 2026, along with a 66.2% gross margin. And Arm Holdings reported 26% year-over-year revenue growth and a 98% non-GAAP gross margin in its most recent quarterly earnings call.

When examining Intel through that lens, its performance doesn’t stand out quite as much. It was good, but not outstanding.

And is “good” something that typically propels a stock to rise more than 360% in a year? Or sustains that growth? History would tell us no.

MORE: How Investors Can Get Access to Elon Musk’s SpaceX IPO

Intel Is Making Progress, But Investors Should Remain Cautious

Here’s how I look at Intel in 2026. It’s made massive improvements and is setting itself up for more success in the AI world, especially with its deal with Elon Musk and the Terafab project. But Intel still lags behind its competitors – especially in AI.

Both these things can be true.

By all accounts, Lip-Bu Tan has done a stellar job as CEO over the past year (layoffs are incredibly difficult, but sometimes necessary). He changed the company’s culture and reestablished Intel as a major tech player after years of relative dormancy. He calls Intel a “fundamentally different company today” than in years past.

But he inherited a mess. And a mess of that magnitude can take years to fix. Tan certainly has Intel on its way. The evidence is in the company’s improving financials and skyrocketing stock price.

So, there are clear reasons to be optimistic about Intel, as long as they are coupled with a healthy dose of caution.

Regards,

David Engle

Editor’s note: Should investors prepare for an AI crash or buy the dips? Analyst and True Wealth editor Brett Eversole just posted a surprising answer. According to Brett’s research, there’s a pattern taking shape that could defy all the worst predictions about a bust. He’s calling it a “Melt Up Tsunami.” And he’s identified at least a half-dozen stocks that could benefit, including his No. 1 stock to own right now. He shares the ticker in this new presentation.

Recent Articles

KKR, Blackstone, and Brookfield Bet $16 Billion on Kuwait’s Oil Pipeline Deal

Bloom Energy’s Recent Mega Sell-Off Could Be a Buying Opportunity After a Blowout Earnings Report