Listen to the audio version of this article (generated by AI).

Key Points

Netflix (NFLX) shares sank to a fresh 52-week low after second-quarter revenue missed estimates and guided to a slower third quarter.

Nine days before Netflix’s earnings report, Marc Chaikin publicly argued that a roughly 40-times-earnings valuation leaves no room for slowing growth, flattening engagement, and AI-driven competition.

In Netflix’s place, Chaikin recommends his “100X Starburst” pick, a technology conglomerate he believes could split into multiple public companies while carrying built-in exposure to the SpaceX (SPCX) and Anthropic IPO wave.

Last night, the market started making his case for him.

Netflix reported second-quarter results after Thursday’s close, and shares fell as much as 12% in today’s trading, touching a new 52-week low. The stock has now been cut nearly in half from where it was a year ago.

Its quarter was relatively fine… Revenue was roughly in line with expectations at $12.6 billion, up 13% year on year and a quarterly record for the business. Earnings per share edged past the $0.79 Wall Street analyst consensus by a penny, and net income climbed by almost 9%.

So why the bloodbath?

Because Wall Street doesn’t pay nearly 40 times earnings for “relatively fine.” It wants to see real growth for that kind of valuation. As we put it last week:

At that price, you’re betting the company is growing fast for a long time, without getting disrupted. Yet Marc notes that new subscriber growth fell by nearly half in 2025, even as the company spends about $20 billion a year on high production-value content.

That works out to about 12% growth… a drop from the 13% growth this quarter and more than 16% in the first quarter. Growth is decelerating quarter after quarter.

There is definitely some kind of slowdown, and I’m not necessarily sure management has articulated what they can do to reinvigorate the business here… All around, there’s really nothing here to get excited about.

Third, Netflix also announced that it would only publish its viewership metrics annually, rather than biannually.

This one hasn’t gotten quite as much attention from Wall Street. But if one of a company’s most important metrics – how many folks are watching its shows – is going flat and management responds by reporting it less often… that’s a bad sign. As Business Insider put it:

The company is relatively candid about this in the investor letter it released Thursday afternoon: It wants Wall Street to stop focusing on the performance of its shows and movies.

“The goal of separating the publication of the report from our earnings results is to keep the focus on our primary financial metrics — revenue and operating profit,” the company said.

The flip side to that argument: If Netflix felt good about its engagement numbers, it would share them more often.

Now, Netflix did try to soften the blow by narrowing its full-year revenue forecast and holding its operating margin target steady. And it also said that recent price increases for U.S. subscribers – the second hike in a little more than a year – have performed in line with expectations.

But no surprise, this morning’s double-digit drop means that investors care a lot more about growth than they do about a company holding steady.

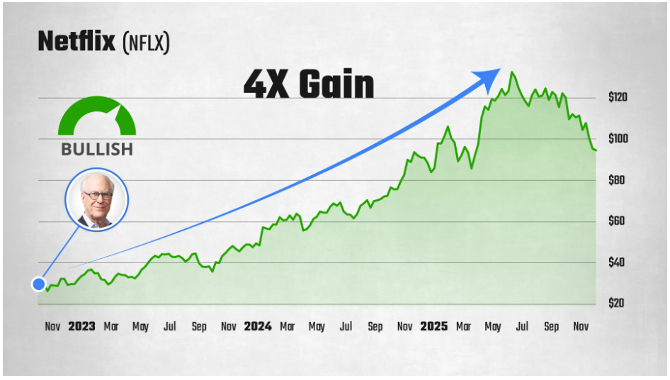

Marc is the 60-year Wall Street veteran whose Chaikin Money Flow indicator appears on Bloomberg terminals worldwide. And his final sell recommendation in his interview surprised me, because I’ve been a happy Netflix subscriber for years. As I noted about Marc’s research…

The Power Gauge liked Netflix for years. In his interview, Marc showed how investors who followed its past bullish and bearish signals could have quadrupled their money in the stock.

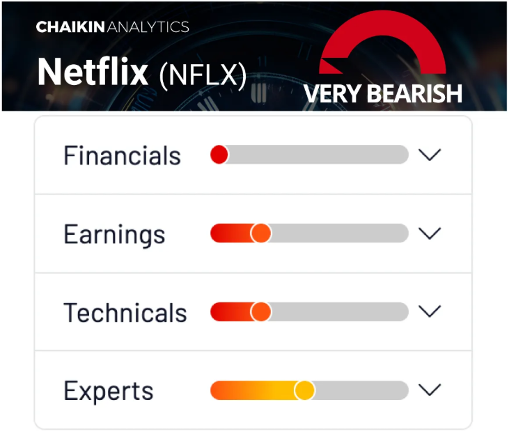

But the system now rates Netflix as Very Bearish, with poor marks across every category…

Marc says that disruption is coming to Netflix…

After all, Netflix’s moat has always been the enormous cost of producing high-quality film and television. A velvet rope kept everyone else out. Marc believes advancing artificial intelligence is about to cut that rope.

Yes, AI production tools will lower costs for Netflix… but they’ll lower them for Disney (DIS), Amazon (AMZN), Apple (AAPL), and every ambitious YouTube creator on the planet at the same time.

The Frontier AI Divide

Marc’s specific Netflix sell call sits inside a bigger stock-market thesis…

He believes that a new class of autonomous “frontier AI” will split the market into a small group of winners and a long list of losers.

For example, take Anthropic, the AI lab behind the Claude models.

The company built an AI model called Mythos that was so capable that it held it back from public release… first giving access to a short list of corporate and government partners under an initiative called Project Glasswing. My colleague David Engle detailed the story and the multiweek government requirement that Anthropic disable access to its newest models. As he wrote:

When Anthropic rolled out Claude Fable 5, its newest AI model, on June 9, the company touted that its capabilities “exceed those of any model we’ve ever made generally available.” Especially when it comes to identifying vulnerabilities in software.

However, AI experts had expressed concerns about the model being used in cyberattacks. Anthropic admitted as much, saying there are risks associated with releasing an AI model as advanced as Fable 5. But the company also unveiled safeguards designed to protect the model from being “misused to cause serious damage.”

That wasn’t enough reassurance for the government, which claimed that a “jailbreak” exists in the model that allows users to circumvent those safeguards.

Kimi K3 “performed competitively with Fable 5 (with fallback) and substantially outperformed Anthropic’s Opus 4.8, GPT 5.6 Sol, and GPT 5.5” in terms of GPU kernel optimisation, the company said. The term refers to techniques that maximise AI hardware utilisation and minimise latency.

That’s one side of the frontier AI divide Marc sees in our near future. As I wrote:

He believes that frontier AI is a technology that will not lift all boats… or at least all boats at the same time.

Instead, the companies who receive early, limited access to the most advanced models will ultimately profit. And the companies who miss out, or that sell software that is ultimately automated away by these more advanced AI agents, will lose.

The other side is even darker and much more personal.

Frontier AI vs. American Jobs

I’ve spent months documenting the risk that AI poses to American jobs…

As AI costs go up and AI gets smarter, human headcounts come down.

Microsoft CEO Satya Nadella himself has previously said that 2026 could be “messy” as the tech industry shifts from AI demos to actual AI integration. He has also called Microsoft’s size a “massive disadvantage” in the AI race.

Whether or not Microsoft announces another major round of cuts this year, the structural pressure isn’t going away. When your CEO describes your workforce as a competitive liability, the writing is on the wall.

If you’re one of the 2.5 million to 3 million folks employed by a Big Tech company… your job is absolutely at risk, whether or not the company denies it today.

That same force is now affecting entire companies…

And when the market is sorting itself this violently, as Marc argues, you don’t want to own a premium-priced content company, like Netflix, on the wrong side of the AI divide.

The short version… Marc has identified a technology conglomerate that he believes trades far below the combined value of its parts, thanks to the well-studied “conglomerate discount.” An ongoing government antitrust case could force the company to split into multiple public companies at once, an event Marc calls a starburst.

Now, out of respect for his paid subscribers, I can’t give that name away here.

But it’s a company that holds one of those Project Glasswing seats… And it carries built-in, pre-IPO stakes in as many as five potential blockbuster listings, including both Anthropic and SpaceX, which completed the largest public offering in history in June.

Discover Where to Put Your Money... And What to Avoid

The Chaikin Power Gauge system lets you pick up on Wall Street signals you can't see on a chart. Enter your email to sign up for our PowerFeed newsletter and gain insights from the system, free of charge.

By submitting your email address, you are agreeing to receive The Chaikin's Power Gauge free newsletter, as well as occasional marketing messages. You can unsubscribe from The Chaikin Power Gauge at any time. Privacy Policy.

Solar stocks have tumbled in 2026, but First Solar continues to deliver strong earnings, a record backlog, and long-term growth potential. Here's why analysts remain bullish.

Starbucks wants to use AI to develop its own inventory-tracking and maintenance system, and it could end up being a big problem for tech giants like Microsoft.