Image Credit: Associated Press

Key Points

- ASML delivered strong first-quarter 2026 earnings driven by surging AI chip demand, beating expectations and raising full-year guidance.

- Despite strong results, the stock has declined following earnings due to a cautious second-quarter outlook and weaker near-term performance, partly tied to reduced sales to China.

- Tightening export restrictions, including the proposed MATCH Act, threaten to impact revenue and could reduce both overall sales and ASML’s high-margin service business.

ASML (ASML), a leader in the lithography technology that enables mass production of semiconductor chips, announced strong first-quarter 2026 financial results on April 15.

That shouldn’t surprise anyone, given the relentless AI-driven demand for chips. But there’s one concern lingering over ASML like a storm cloud threatening to ruin a beautiful day… exports to China.

The U.S. and the Netherlands – where ASML is headquartered – are tightening export restrictions on China, which could adversely impact ASML in several ways. But will those trade hurdles be enough to slow ASML amid insatiable chip demand?

ASML’s Strong Quarter Fueled by Nonstop Demand for AI Chips

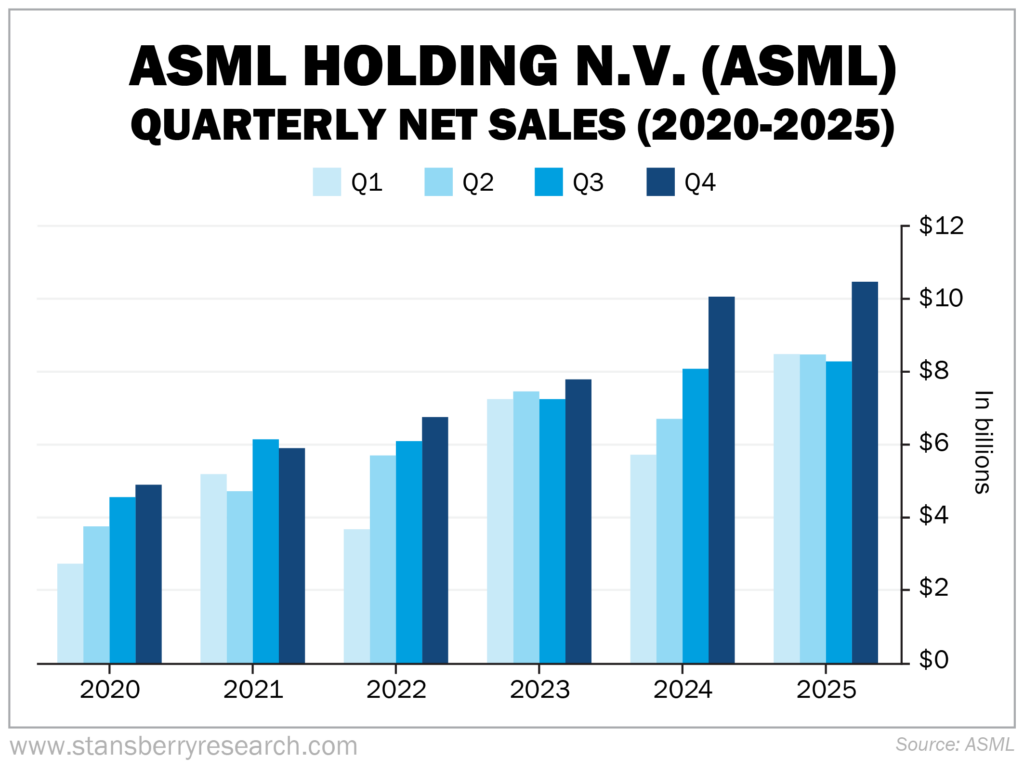

Overall, ASML’s results exceeded expectations, prompting the company to raise its full-year 2026 revenue guidance to a range of $42.2 billion to $46.9 billion.

Here are some highlights from ASML’s first-quarter 2026 earnings call (all figures are converted to USD from euros):

- $10.3 billion net sales, up 13% year over year (“YOY”)

- $3.2 billion net income, a YOY increase of roughly 17%

- $5.4 billion gross profit, up more than 11% YOY

- 53% gross margin, decreased slightly YOY from 54%

- $8.38 earnings per share (“EPS”), a significant 19% YOY increase

But after a weeklong, pre-earnings rise of roughly 16.2% between April 7 and April 14, ASML’s stock dipped more than 7% in the days following the earnings call.

Why the steep drop in share price if the results were generally seen as strong?

That’s mainly because ASML opted for a cautious approach for the next quarter and offered a very conservative second-quarter 2026 outlook. Its midpoint revenue outlook of $10.2 billion for the second quarter fell below analysts’ $10.6 billion midpoint projection.

And its forecast 51% to 52% gross margin would represent a small decrease from its first-quarter figure.

Hence the drop in share price.

Also worth noting, nearly all the first-quarter numbers fell short of ASML’s fourth-quarter 2025 numbers. Net sales were down nearly 9.8%. Gross profit fell 8.3%. Net income dropped nearly 3%. And EPS dipped 2.7%.

Historical data suggests this may simply be seasonal. In five of the past six years, ASML has recorded its highest quarterly net sales in the fourth quarter (2021 being the sole outlier).

What are the reasons for high historical performance during the fourth quarter? Final acceptance of customer sales is one explanation. ASML pushing to clear its huge backlog (which was more than $45.7 billion at the end of 2025) by hitting year-end delivery goals is another reason.

It’s also worth noting that fourth-quarter 2025 was a record breaker in net sales for ASML, so a slight decline isn’t all that shocking.

However, there’s another worrying explanation for the quarter-over-quarter numbers decline, and it has everything to do with China.

China Export Restrictions Are Already Causing Problems for ASML

Some 36% of ASML’s net system sales in the fourth quarter of last year were to China. That number plunged to 19% during the first quarter of 2026.

This is a problem for ASML that may not be solved anytime soon. And it has the potential to make a significant dent in the company’s revenue moving forward.

Here’s why…

In early April, U.S. lawmakers proposed the Multilateral Alignment of Technology Controls on Hardware (“MATCH”) Act. The bill would stop shipments of the advanced machinery and equipment necessary to make chips to China. Chinese chipmakers Semiconductor Manufacturing International, ChangXin Memory Technologies, Yangtze Memory Technologies, Hua Hong, and Huawei were named specifically.

This ban would cover the same deep ultraviolet (“DUV”) lithography machinery that ASML manufactures and sells to chipmakers – including those in China. (Export of extreme ultraviolet (“EUV”) lithography equipment was already restricted.)

The MATCH Act goes even further, however. Not only are sales of new equipment to China prohibited, but previously sold machines that are already in Chinese facilities may not be serviced or maintained.

Taking a step back, you may wonder why an American law would impact a Dutch equipment maker like ASML?

Because the MATCH Act would enforce a 150-day deadline for U.S. allies (like the Netherlands) to conform their export controls to U.S. standards or else face repercussions in the form of sanctions, financial penalties, and even criminal charges.

It’s essentially forced compliance.

And that forced compliance could cost ASML roughly 17% in revenue, based on the above-mentioned quarterly drop in sales to China.

The company would also wave goodbye to a significant portion of its high-margin, $2.9 billion-plus in Installed Base Management sales (ASML’s upgrades, software, and maintenance of previously installed systems).

As the U.S. continues its battle with China for global AI dominance, the logic behind the MATCH Act makes sense. If China doesn’t have the technology it needs to make advanced nodes and wafers for its chips, this would set the country even further behind.

On the other hand, it might also force China to ramp up its own chipmaking technology, creating unforeseen competition for businesses and companies like ASML.

In fact, it’s already starting to happen. Taiwan Semiconductor Manufacturing (TSM), a key buyer for EUV machines, stated that it will not be buying ASML’s latest generation high-NA (“numerical aperture”) EUV machines due to their high cost.

Stansberry Research Analyst Alan Gula isn’t concerned about this development, however. “I don’t see this as a big problem for ASML,” said Gula. “It just means that TSM will need more of the older EUV machines now. But, TSM will eventually need the more expensive EUV machines down the road.”

Gula noted that there are risks in the short term, as China accounted for roughly one-third of ASML’s sales in 2025 – much of which came from sales and servicing of ASML’s older DUV machines.

“Obviously, if export restrictions are tightened and ASML loses that China DUV revenue, it would hurt the company,” explained Gula. “It’s just a short-term risk that we have to live with amid a longer-term bullish backdrop.”

This is something worth monitoring in the coming months, as it could alter ASML’s trajectory for 2026 and beyond.

MORE: Best AI ETFs: 7 Top Funds for Artificial Intelligence

Will ASML Continue to Grow in 2026 Despite the Challenges?

Nothing is guaranteed. But ASML is considered a strong business, and AI’s seemingly never-ending demand for chips provides the company with a fairly wide moat.

In March, I wrote a piece on nanotechnology, the science behind chipmaking. In profiling ASML, I noted:

[EUV] machines are necessary to build advanced semiconductors below 7 [nanometers]. And if a tech company needs these advanced chips to build phones, computers, electric vehicles, or data centers, they’re coming to ASML.

Why? Because ASML is the world’s only provider of these EUV lithography systems. In fact, the company has a legal monopoly on EUV technology.

Yes, ASML is literally the world’s only supplier of the EUV machines needed to manufacture advanced chips. Also, EUV technology aside, ASML entered 2025 holding a 90% market share over the larger, global lithography-tool industry.

So, it’s built to withstand any revenue losses from China.

But it’s feasible that the lost sales from China could result in lower revenue forecasts in the coming quarters. It’ll be interesting to see how ASML’s second quarter plays out after factoring in another three months of decreasing sales to China.

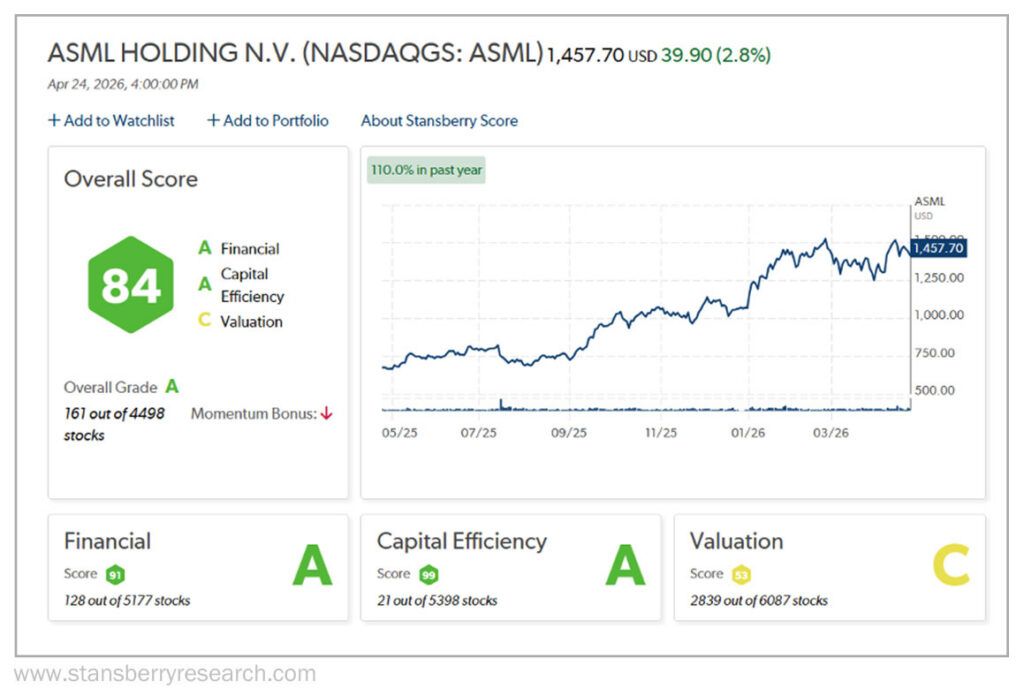

ASML’s Stock Rating

At nearly $1,500 a share, ASML’s stock is a pricey proposition.

But it’s a very strong stock.

The Stansberry Score, a tool that helps determine the quality and long-term value of thousands of stocks, grades ASML an “A” overall, ranked well within the top 200 stocks out of more than 4,400.

As we covered, the company’s Financials (“A”) are excellent. And its Capital Efficiency (“A”) is even better, ranking within that category’s top 25 out of nearly 5,400 stocks. ASML’s monopolistic hold over the lithography industry – specifically the EUV lithography market – gives the company an edge that can’t be overstated.

Because the products ASML builds are so complex and depend on years of research, entering the market as a new business is a risky path. That leaves ASML with very little – if any – competition.

And since ASML is the only company in the world making the EUV equipment that chip manufacturers need to build their products, it can basically name its price – where else are the chipmakers going to go?

Plus, roughly 28% of ASML’s sales come from the maintenance and service of its 5,000-plus installed machines. That’s high-margin revenue, which contributes substantially to ASML’s overall gross margins – hovering around 50%.

With those high margins comes a steady flow of free cash that pays dividends and funds share repurchases. ASML paid a dividend of $1.91 per share in February and will pay $3.18 per share (the second-highest quarterly dividend payment in company history) in early May.

In late January, ASML announced a roughly $14 billion share-purchase program that started after the announcement and concludes at the end of 2028.

That’s certainly welcome news for investors.

MORE: 11 Hot IPOs to Watch in 2026: SpaceX, Anthropic, and More

ASML Outlook

It’s safe to say that the AI-driven demand for chips won’t wane anytime soon. In fact, chips will only grow more complex with each new iteration. And that keeps ASML in a very enviable position.

ASML has semiconductor giants such as Samsung and Intel (INTC) locked into lucrative agreements over the coming years – not just for ASML’s current EUV lithography technology, but also early access to its high-NA EUV machinery.

Intel was the first company to receive a new ASML high-NA EUV scanner. And that should be put to good use, considering Intel’s recent deal with Elon Musk to join the SpaceX/Tesla/xAI Terafab project.

The geopolitical tensions with China are worth watching, as losing sales to China could dent ASML’s revenue stream.

But ASML is in such a strong defensive position that it may not even miss China’s revenue in the coming years.

If the company continues to research and develop the latest lithography tools that physics and nanotechnology have to offer, ASML will remain the foundation upon which the chip industry – and AI as a whole – is built.

Gula recognized ASML’s innovation and the effective monopoly it held on EUV machines back in 2022, when he and Stansberry first recommended ASML.

“That’s still the case,” said Gula. “And now ASML is a big beneficiary of the AI boom, which has even accelerated over the past few months. So, we continue to be bullish on ASML over the long term.”

Regards,

David Engle

Editor’s note: A former hedge-fund manager known for spotting early winners is sounding the alarm once again.

He called Netflix (NFLX) at $7.78 (up nearly 1,100% since), Apple (AAPL) at $0.35 (up more than 10,000%), and Amazon (AMZN) at a split-adjusted $2.41 (up 3,200%).

Now, this renowned investor released a newlist of his favorite AI stocks… and not a single Magnificent Seven name made the cut.

Instead, an AI stock you’ve likely never heard of just flagged as “near perfect” in his new investing scoring system.

Click here to watch his brand-new presentation, where he reveals the name, ticker symbol, and why this could be the smartest AI move of the year… especially if you’re over 50 years of age.