Key Points

- Intel received a major boost after reports suggested Apple may use Intel’s advanced 18A chipmaking process in future devices, adding to momentum from recent AI and foundry partnerships.

- CEO Lip-Bu Tan’s turnaround strategy has been supported by rising foundry revenue, stronger AI data-center demand, government support, and improving relationships with major technology companies, helping drive the stock sharply higher over the past year.

- Despite Intel’s momentum and growing AI infrastructure role, investors remain concerned about the company’s valuation, ongoing operating losses, and whether the stock has risen too quickly relative to its long-term fundamentals.

Intel (INTC) CEO Lip-Bu Tan and Apple’s (AAPL) outgoing CEO Tim Cook agreed to a preliminary deal that would have Intel make chips for some Apple devices, according to a report from the Wall Street Journal on May 8.

Despite limited details, one thing is clear: Intel will be a massive winner if this deal materializes.

Intel is riding a wave of momentum that may be as high as the chipmaking titan has ever experienced in its nearly 60-year history. In roughly the past month alone, the American chipmaker forged a deal with Elon Musk and his joint SpaceX/xAI/Tesla (TSLA) Terafab project, reported its fourth straight quarter of increasing revenue, hit its all-time high stock price, and now this.

Getting the stamp of approval from two of the most impactful brands in the world has that effect. And Intel shareholders are reaping the benefits.

Intel stock was already blowing up at previously unseen levels. On May 1, I wrote a piece detailing Intel’s recent meteoric rise, noting that its stock had surged more than 360% over the past year.

Well, that has since grown to more than 500%. Yes, Intel’s stock has soared roughly 521% from the start of May 2025 to May 8, 2026, after the preliminary Apple deal was reported.

In fact, Intel shares skyrocketed 14% once news of the preliminary agreement broke.

Naturally, this begs these questions: Will Intel maintain this momentum (or gain even more), and is Intel a good investment at these sky-high prices?

Apple Deal Validates Intel as a Major Semiconductor Player

Despite Intel’s legacy as a tech giant, validation is essential given its recent history.

Here’s what I wrote on May 1 when examining Intel’s troubled past:

Intel’s issues stretch back to the late 1990s, when strategic misses began to derail the company.

- Intel missed the boat on developing graphics processing units (“GPUs”) in the 1990s. GPUs are now a critical component of AI accelerators – the technology that speeds up AI tasks and allows generative AI to run.

- In 2007, [Apple] approached Intel about supplying chips to power the first iPhone. Intel’s then-CEO, Paul Otellini, passed on the opportunity because he wasn’t sold on the iPhone. So, Apple turned to chips made by Arm Holdings (ARM). Today, Arm’s technology powers more than 99% of the world’s smartphones.

- Fast-forward another decade, when Intel failed to create good enough processors to compete with rivals such as [Advanced Micro Devices (AMD)], [Nvidia (NVDA)], Samsung Electronics, and [Taiwan Semiconductor Manufacturing (TSM)], ultimately pushing Intel into near irrelevance.

- In 2017, former CEO Bob Swan declined an offer to acquire a 15% stake in OpenAI for roughly $1 billion. This deal would’ve placed Intel at the center of the AI boom from day one. Besides costing Intel billions over the past decade, the decision blew Intel’s opportunity to become an AI pioneer while sabotaging any future business with OpenAI.

The aftermath of Intel’s miscalculations was ugly.

In July 2025, the company announced it was cutting its workforce by more than 25,000. This followed more than 15,000 layoffs in August 2024.

So, yes, this recent validation from Apple and Tesla is monumental for Intel. And it continues the amazing turnaround of its previously stagnant foundry business.

More from my May 1 analysis of Intel Foundry:

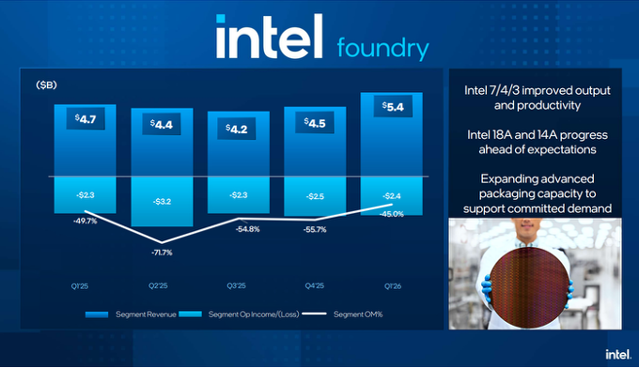

In 2022 and 2023, Intel Foundry Services (“IFS”) earned external foundry revenue of $895 million and $952 million, respectively.

IFS revenue then exploded to $17.5 billion in 2024 and increased to $17.8 billion last year. The pattern continued into 2026’s first quarter, with Intel’s foundry business earning $5.4 billion, a nearly $1 billion jump from the previous quarter.

This proposed deal has Apple using Intel and its 18A process node to build Apple’s chips, a confirmation that Apple – a notoriously demanding customer – approves of Intel’s technology.

As for Musk and his Terafab deal with Intel? He noted during Tesla’s first-quarter 2026 earnings call that:

We plan to use Intel’s 14A process, which is state of the art and in fact not yet totally complete. By the time Terafab scales up, 14A will be probably fairly mature or ready for primetime.

14A seems like the right move, and we have a great relationship with Intel, a lot of respect for the CEO, the [chief technology officer], and the new team there.

This was music to Intel’s ears – and President Donald Trump’s.

Government’s Stake in Intel Also Makes This Deal Highly Political

Back in August 2025, the United States government became an Intel shareholder when the company ceded roughly 10% of its non-voting shares (an $8.9 billion investment by the government) in a deal widely seen as a lifeline for the then-floundering company.

I examined the Intel-White House deal back in September, writing:

Favoring Intel is President Trump’s personal involvement with the agreement… It’s difficult to envision him or his administration allowing Intel to fail.

The White House has all the motivation in the world for Intel to succeed. And Intel gained new capital as a result of the deal. All things being equal, that’s never bad…

If there’s one thing Donald Trump hates, it’s being wrong… So expect the White House to do everything in its power to make Intel successful again.

Fast-forward to the present.

Trump (and Commerce Secretary Howard Lutnick) reportedly played a major role in the Apple-Intel deal, personally lobbying Tim Cook to have Intel produce chips for some Apple devices. This deal would benefit the government in a few ways.

First, Apple will reduce its reliance on chips from Taiwan Semiconductor and accelerate domestic semiconductor manufacturing. Intel operates advanced fabs in Arizona, New Mexico, and Oregon, with a massive new facility under construction in Ohio. This decisively strengthens the U.S. semiconductor supply chain – a clear strategic victory for Intel and the Trump administration.

Of course, the federal government also stands to make a lot of money from this deal. After Intel’s stock soared once the Intel-Apple agreement was made public, the government’s initial $8.9 billion investment was suddenly worth $56.5 billion. That means the U.S. Treasury holds roughly $47.6 billion in unrealized gains from this deal.

While that amount of money is certain to raise some eyebrows, there’s no denying that this arrangement benefits all three parties involved – the government, Intel, and Apple, as the latter buys itself some leeway with Trump by moving more of its manufacturing to America.

Is It a Good Time to Buy Intel Stock Near Its All-Time High?

Intel has performed a complete reversal over the past year, turning its business and reputation around under the guidance of Lip-Bu Tan.

As I wrote on May 1:

It’s difficult to pinpoint any single event or decision that prompted Intel’s reversal of fortune. But it’s safe to say that better overall strategy and decision-making, led by Tan, has played a pivotal role.

Since Tan came aboard in March 2025, he has been laser-focused on improving margins (which was, in part, accomplished by the massive 2025 layoffs), becoming a key player in the AI data-center realm, maximizing yields for its advanced 18A and 14A process nodes, and resurrecting Intel’s foundry business.

All of this has heavily contributed to Intel’s incredible stock gains since last May, when Intel could be had for roughly $20 a share. Today, Intel is trading around $120 per share.

Should investors consider buying at these elevated levels?

Intel’s performance will hinge on how decisively it capitalizes on its momentum and secures additional deals. Let’s look at the bull and bear cases for Intel.

Bull Case for Intel

Intel is clearly heading in the right direction.

- Revenue is on the rise, with Intel reporting first-quarter 2026 earnings of $13.6 billion, up 7% year over year. This marked the sixth straight quarter that Intel beat expectations.

- Intel has reportedly sold out most of its server central processing unit (“CPU”) inventory for 2026.

- The company’s foundry business has a $15 billion-plus backlog.

- Intel’s Data Center and AI (“DCAI”) first-quarter 2026 revenue increased 22% year over year to reach $5.1 billion.

- The company has long-term agreements with three of the world’s top cloud providers (Microsoft Azure, Google Cloud, and Amazon Web Services) to use Intel’s processors to enhance their AI infrastructure.

- The Apple and Terafab deals on the horizon are high-profile wins for Intel.

That has all contributed to the stock price more than doubling since the start of 2026. If Intel maintains this momentum and builds upon it, today’s roughly $120 share price could look like a bargain in a few months, especially when you consider the relentless demand for GPUs and CPUs and Intel’s relative pricing control over those components.

But Intel’s steep upward trajectory could lead to a pullback at some point. While it’s certainly possible Intel will sustain this level of outperformance, remember that it’s part of a very volatile industry and the market tends to correct itself over time.

Bear Case for Intel

We know that AI demand is massive right now, and Intel has been white-hot. But we don’t have to go far back in Intel’s history to understand why it was in a position that necessitated a turnaround in the first place.

The company still has some issues, which I outlined on May 1.

Intel still incurs significant operating losses despite receiving government subsidies. For example, even with the recent gains in its foundry business in 2025, Intel reported operating losses of $2.2 billion last year. That contributed to Intel’s more than $1.6 billion in negative free cash flow, as did roughly $11.2 billion in capital expenditures to build new fabs and equipment (a justifiable investment). In the first quarter of 2026, Intel’s foundry business reported another $2.4 billion in operating losses.

As of April 30, Intel’s forward price-to-earnings (P/E) ratio was 93.76 times, which is extremely high. Considering Intel stock was trading at roughly $93 on April 30, its valuation is also quite high… suggesting that Intel is considerably overvalued right now. That means Intel will have to perform at a near-perfect level in the coming months to sustain its current trajectory.

That still holds true a couple of weeks later, only its forward P/E ratio is even worse – on May 12, it was 115.47 times, and its closing price was $120.61. Intel looks overvalued using that metric.

And one more thought to consider: Is Intel simply the beneficiary of good timing, given the relentless demand for its CPUs, GPUs, and other products? Or is the company delivering the innovation that data centers and electronics manufacturers want?

Probably a little bit of both.

There’s no disputing the fact that Intel has turned the ship around. The reported deal with Apple is simply further validation. Along with its Apple agreement, the company has several prominent deals in place and is growing fast in the AI and data-center space. After several years of questionable leadership decisions, it feels like Intel got it right with Tan as CEO.

But Intel still has a long road ahead if it expects to catch rivals Nvidia and Advanced Micro Devices, especially in the AI race. The company is finally gaining some ground, however.

So, is it a good time to buy Intel at roughly $120?

On May 12, Mizuho raised its price target for Intel from $100 to $124. Deutsche Bank did the same, increasing its target from $63 to $100. MarketWatch’s average price target for Intel on that same date was $92.60.

Simple math tells us that Intel is trading roughly $27 above its average price target. That math is hard to ignore.

There are clear reasons to be optimistic about Intel’s future. But at its current price? The stock looks expensive, making it harder to justify.

Regards,

David Engle

Editor’s Note: While everyone is focused on the SpaceX IPO, one America’s best stock pickers, Luke Lango says the real money is in something Elon has working on for decades. The world’s richest man is about to disrupt the $480 trillion global financial system in a way that few people see coming, and Luke is giving away his No. 1 way to play it, free, in this presentation.