Food prices are climbing fast. Ground beef just hit a record $6.90 per pound, wheat is up 28% since January, and tomato prices keep ticking higher. It looks like my next summer cookout might be BYO-burger.

But here’s the thing: the forces pushing food prices higher are just getting started.

Over the next 12 to 18 months, American consumers will face a food price crisis as the ongoing energy shock ripples through the food supply chain. Farmers will cut back on plantings due to higher fertilizer costs. Logistics firms will charge more as diesel prices rise. Grocers will pass food inflation onto customers. In fact, the crisis is so worrying that the White House has already rolled back tariffs on hundreds of imported food items, including coffee, bananas and cocoa. It is now considering doing the same for beef.

These efforts aren’t enough. The British Energy and Climate Intelligence Unit (ECIU) estimates that U.K. food prices will rise at four times the historic rate from high energy prices and weather disruptions. American consumers are staring down the same pressures. High energy prices and poor harvests mean high food prices, and there’s no magical cure on the horizon.

So, everyone knows food prices are about to surge. It’s just a question of when the market will care.

I believe one stock is positioned to benefit enormously when it does.

GO Stock: The Company the Market Forgot

Grocery Outlet Holding Corp. (GO) is not your typical grocer.

While companies like Albertsons Companies Inc. (ACI) and Kroger Co. (KR) rely on contracted suppliers and carry predictable inventory, Grocery Outlet operates on an entirely different model.

Its centralized buying team scours the market for closeout deals, overstock, label redesigns, short-dated inventory, and seasonal surplus from major national brands. When a brand overproduces, changes its label, or needs to clear warehouse space, Grocery Outlet swoops in and buys that inventory, typically at 40% to 70% below retail prices.

Then it passes those savings to customers through its roughly 570 stores across 16 states, with the bulk of its locations on the West Coast.

Think of it less like a traditional grocer and more like a TJX Co. (TJX) for food. It’s the same treasure-hunt, never-the-same-inventory-twice model that has made T.J. Maxx one of the most resilient retailers in America. Except instead of discounted designer handbags, you’re getting name-brand cereal, olive oil, and frozen burgers at a steep discount.

This distinction matters most when food prices are rising.

GO Stock Thrives When Food Prices Rise. We’ve Seen This Movie Before

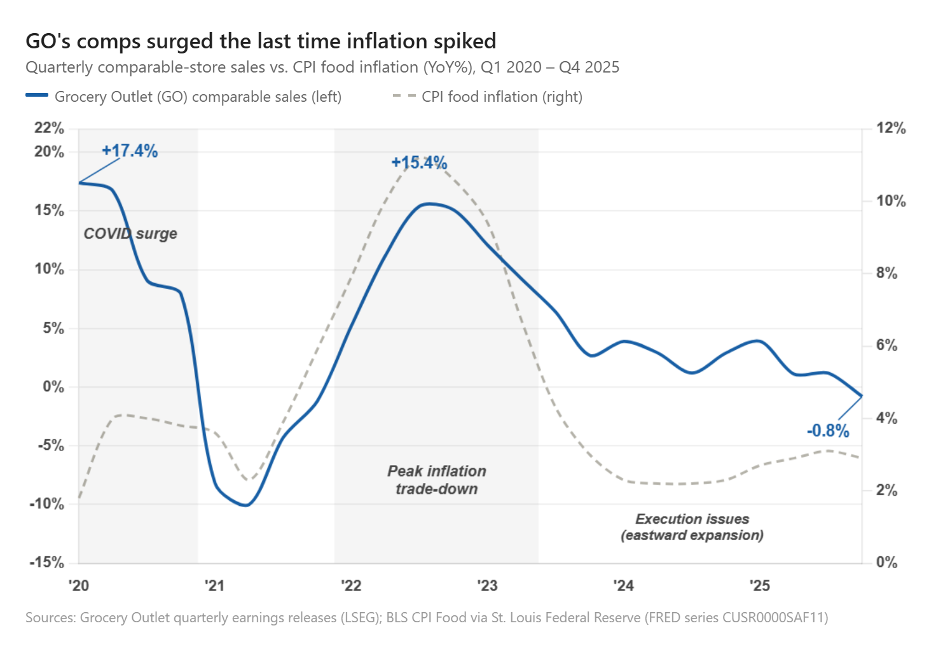

In 2022, rising food prices sent Grocery Outlet’s comparable store sales surging.

Comparable sales jumped 15.4% in the third quarter of that year, and 15.1% in the next. Customers who had never set foot in a Grocery Outlet were suddenly walking through the doors because their usual grocery bills had become unbearable.

“As consumers are dealing with record inflation, they are turning to us for access to affordable quality food and our industry-leading savings,” said the company’s CEO at the time, RJ Sheedy. “Our compelling WOW! shopping experience is attracting new customers and existing customers are spending more of their dollars with us.”

Suppliers also tend to generate more surplus inventory during periods of inflation. Rising costs push brands to reformulate products, change packaging and reprice. Each of these moves creates the kind of surplus that Grocery Outlet’s buying team lives on. This effect showed up in 2020, when COVID disrupted food supply chains, and again in 2022 at the off-price retailer.

In other words, rising food prices doesn’t just push customers toward Grocery Outlet. It also improves the quality and quantity of deals available for GO to buy.

That’s a double tailwind most investors miss.

Of course, GO’s comps decelerated in 2023 and deteriorated badly by 2025 as inflation faded and the company made several execution missteps. That included a botched technology overhaul and an overambitious expansion eastward. CEO RJ Sheedy resigned and was replaced by former Fresh Market CEO Jason Potter in February 2025.

GO Stock Is Hated, but Not Broken

Things admittedly remain ugly.

The company closed 36 underperforming stores in 2025, or roughly 30% of its Eastern U.S. portfolio. Management wrote off $308 million the same year in goodwill and restructuring charges, generating the company’s first net loss in history. Guidance calls for comparable-store sales between -2% and flat for fiscal 2026, and GO stock now trades roughly 80% below its all-time highs set in 2022.

But ugly and broken are different things.

Many of Grocery Outlet’s “issues” are sandbagging. Large write-offs and low guidance are a classic way of throwing old management under the bus to start with a clean slate. And the core business model remains intact: larger rivals have shown little interest in competing in the off-price grocery space.

In fact, we’ve seen some green shoots emerge in recent months. In March 2026, the CEO guided to gross margins of 29.7% to 30%. This is back in line with historical levels. The company is planning to open 30 to 33 new stores in 2026, refocusing on the West Coast.

Most importantly, insiders have been buying shares. Over the past several months, we’ve seen:

- CEO Jason Potter — 398,000 shares (~$2.4 million)

- 5 Directors — 920,000 shares (~$5.4 million)

Cluster buying — when multiple insiders purchase shares simultaneously — is one of my favorite “Buy” signals. It says insiders believe in the business. And even though three other insiders made smaller sales of 4,000 shares each, the sheer size of these purchases more than offsets the small sells.

Meanwhile, the negative headlines have pushed Grocery Outlet to its most attractive valuation in its operating history. GO stock trades at roughly 16x forward earnings and 0.2x sales, making it the second cheapest stock in its grocery peer group on a price-to-sales basis. The only grocer trading cheaper is Albertsons, which carries significantly more debt and runs a conventional model that tends to suffer during recessions.

Risks to the GO Stock and Food Prices Thesis

This isn’t a risk-free call, and I want to be transparent about where the problems may lie.

The biggest risk is execution. If Grocery Outlet’s comparable-store sales don’t rebound by Q3 2026, that would tell me the operational problems run deeper than a few bad store locations. It would mean the turnaround isn’t working, and no amount of food price inflation will fix a fundamentally challenged retailer.

Food inflation could also prove milder than expected if tariffs are rolled back or supply chains adapt faster than anticipated. That would remove the primary catalyst.

The third challenge comes from the company’s Independent Business Owner model, where store-level gross profits are split 50/50 between Grocery Outlet and the operator. While this structure allows the company to expand quickly it also creates operational inconsistency. Not every operator follows corporate standards to the letter, and some locations have been known to charge higher prices than others – a direct threat to the brand’s core value proposition.

I should also acknowledge that while GO looks like an off-price retailer, it’s still a grocer at its core. If consumers become so squeezed that they cut back on food spending altogether – not just trading down, but buying less – even the deepest discounter feels that.

The Bottom Line on GO Stock

Nevertheless, Grocery Outlet is a genuinely differentiated business hiding in one of the most beaten-down stocks in retail. Its model has proven itself in past food price surges. The turnaround is early but directionally right. And the valuation, at 16x forward earnings, gives a reasonable margin of safety if the recovery takes longer than expected.

I’m looking for 80% or more upside in GO stock over the next 12 to 18 months as food inflation accelerates. I’m adding Grocery Outlet to my “Top Picks” list for 2026. (You can see my other picks here and here, which have risen 17.4% on average since recommendation first recommended them).

In a market obsessed with AI and semiconductors, sometimes the best opportunities are hiding in the grocery aisle.

Regards,

Thomas Yeung, CFA

Market Analyst, InvestorPlace

Editor’s Note: While the financial media tells you what to buy, legendary Wall Street analyst Louis Navellier has spent 46 years tracking where billionaires and institutions actually position their money. His proprietary stock grading system — the same one wealthy firms paid $24,000 per year for me to evaluate stocks with — measures the three factors that predict institutional buying before it happens. Right now, his system is detecting something he’s only seen twice before in his career: massive money flows that signal the largest wealth transfer in American history. And most investors are positioned on the wrong side. See what Navellier’s system is revealing — including the specific sectors where institutional money is flooding in while retail investors look elsewhere — in his urgent presentation here.