Image Credit: Associated Press

Key Points

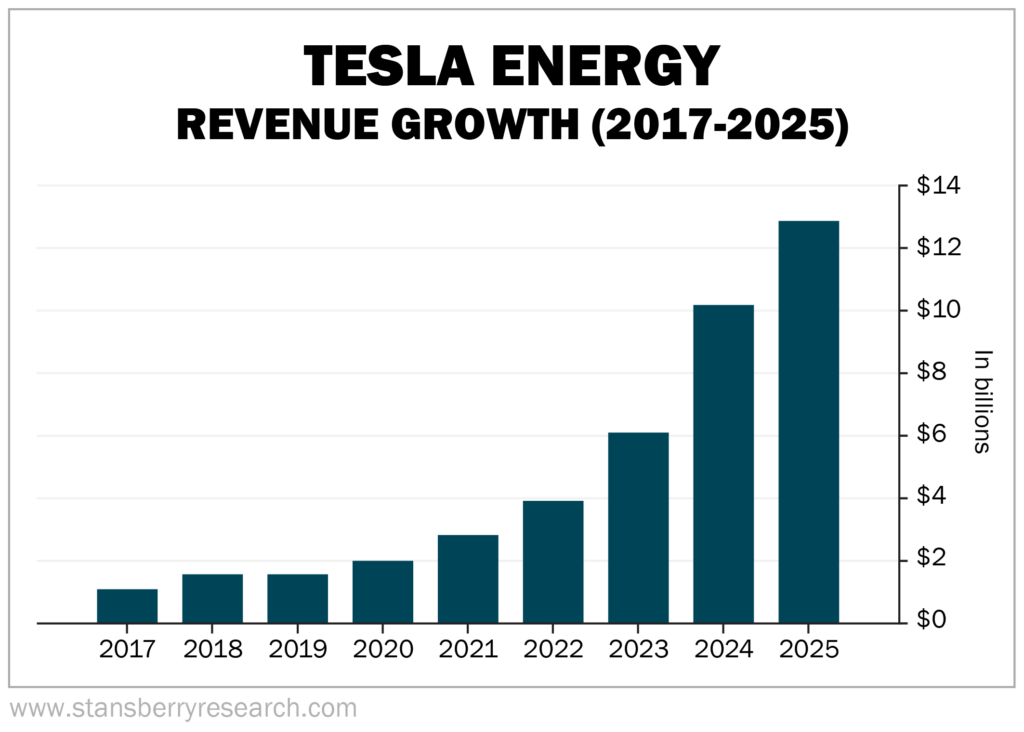

- Tesla is rapidly expanding its solar business, with Tesla Energy revenue climbing to nearly $12.8 billion in 2025 as AI-driven electricity demand accelerates.

- The company plans to build 100 gigawatts of annual solar capacity by 2028 through a massive new Texas facility, an extremely ambitious target relative to the current size of the industry.

- If Tesla successfully scales its integrated solar ecosystem of panels, Powerwall batteries, and Megapack storage systems, it could secure major advantages in pricing, supply chains, and market share.

Tesla is back in on solar in a big way, and artificial intelligence (“AI”) is the main driver.

Ten years ago, Tesla (TSLA) acquired SolarCity, a residential solar energy company, for approximately $2.6 billion. SolarCity’s operations were folded into Tesla Energy, the branch of Elon Musk’s empire that offers solar panels, solar roofs, Powerwall batteries, and Megapack large-scale energy storage.

Tesla Energy’s business stayed relatively dormant for about seven years after the acquisition.

In 2017, the year after the deal, it generated roughly $1.1 billion. From there, revenue increased only incrementally for several years.

But during 2024, Tesla Energy revenue jumped from just over $6 billion to nearly $10.1 billion, primarily driven by the nonstop energy needs of AI data centers. In 2025, it earned $12.8 billion.

Now that Tesla Energy is a solid earner for the company, Tesla is reportedly building a massive new solar panel manufacturing factory in Brookshire, Texas, near Houston, to be co-located with its Megapack Megafactory. That facility is expected to open later this year.

Even as the solar plant is still under construction and undergoing modifications, Musk has publicly stated that Tesla aims to vastly expand its solar manufacturing capacity by the end of 2028.

What does this new solar facility mean for Tesla and investors? Let’s dive in.

Tesla’s Solar Energy History

Before we get into the details, let’s remember that Elon Musk has a penchant for overpromising, or at least being overly aggressive in his planning. We’ll need to wait and see whether Tesla’s new solar manufacturing factory in Texas delivers Musk’s expected output (which we’ll get to in a moment) on his timeline.

Despite Musk’s ambitions, Tesla’s track record in the solar industry has been mixed.

When Tesla acquired SolarCity in 2016, the company brokered a deal with the State of New York in which the state built an expansive factory – Gigafactory New York – in Buffalo in exchange for the promise to create 1,500 jobs at the factory and to invest $5 billion in New York State over 10 years.

This solar manufacturing factory would be the largest of its kind in the Western Hemisphere.

But it didn’t happen. Tesla outsourced the production of its solar panels to Panasonic, which built them until 2020. After that, Gigafactory New York was primarily used to build Tesla’s Supercharger components.

For the next five years, Tesla shifted its attention away from solar power.

Then, in late 2025, as AI data centers began devouring any and all available power, Tesla started building its TSP-420 solar panels at Gigafactory New York. It began selling those solar panels commercially earlier this year. And it’s seemingly only getting started.

The capacity at Gigafactory New York is roughly 300 megawatts (“MW”) per year. Musk is thinking much, much bigger.

Tesla Aims for 100 GW of Solar Manufacturing Per Year

When Musk spoke at the World Economic Forum in Davos, Switzerland in January, he proclaimed that Tesla and SpaceX would each build 100 gigawatts (“GW”) of solar manufacturing capacity in America, from start to finish.

That’s 333 times more capacity than Gigafactory New York can provide. And it’s enough to power roughly 70 million average American households. Musk hopes to accomplish this growth in the span of a few years.

To illustrate how ambitious – or aggressive – this 100 GW goal is, let’s look at America’s largest solar manufacturer. First Solar (FSLR) projects to have a capacity of roughly 18 GW by 2027. Tesla is shooting for more than five times that number.

Meanwhile, the entire U.S. solar industry added 43.2 GW of capacity in 2025. Tesla wants to more than double that on its own.

This is where Musk’s ambitions sometimes get in the way of reality. But that won’t stop him from trying.

Tesla is already negotiating the purchase of nearly $3 billion of Chinese solar manufacturing equipment for the Texas facility.

And the type of equipment that Tesla will buy, according to Electrek, supports completely vertically integrated solar cell production.

That means Tesla’s entire solar manufacturing supply chain will be contained within its Megafactory campus outside of Houston, from processing raw materials through the assembly of finished panels.

In theory, this makes sense. Not only will the entire solar panel manufacturing process take place under one roof (or a couple of roofs in the same industrial complex), but these solar panels will go hand in hand with the other products Tesla is building at the Megapack Megafactory in Texas.

For example, Tesla offers its Megapacks with large-scale solar installations and its residential Powerwall batteries with rooftop solar panels. Co-locating Tesla’s solar manufacturing with its Megafactory simplifies both the supply chain and logistics.

If Musk’s grand solar plan comes to fruition, Tesla instantly becomes one of the world’s largest solar manufacturers and a major force to be reckoned with in the industry.

Is Tesla’s 100 GW Solar Goal Realistic for 2028?

Short answer: Probably not by 2028. Here’s why.

100 GW is an extremely aggressive goal, as I noted, especially when you consider both First Solar’s and the entire solar industry’s manufacturing capacities. If you’re looking to create five times more solar capacity than the current domestic leader, and more than double the solar capacity of the entire industry – in less than two years – you may be aiming too high.

And let’s be honest here, this wouldn’t be the first time Musk overpromised. Far from it.

A few examples:

- Tesla robotaxis and autonomous vehicles, which Musk claimed would be ready to drive cross-country, unmanned, by 2018. It’s 2026, and Tesla’s Full Self-Driving (“FSD”) vehicles still require human supervision.

- Boring Company’s network of underground tunnels that would autonomously shuttle passengers to their destinations at up to 150 miles per hour. Musk’s goal was to construct one mile of tunnel per week. Today, the only operational system is the Las Vegas Convention Center (“LVCC”) Loop, a 1.7-mile stretch that transports convention attendees across the LVCC campus… in human-driven Tesla cars, at speeds of up to 40 miles per hour.

- Tesla Cybertruck, the notorious stainless steel pickup truck that Musk promised would enter production in 2021 and retail for under $40,000 to start. Cybertruck production didn’t begin until late 2023, with an initial starting price of $61,000 for the base model. It has been a major commercial disappointment to date.

These are just a few prominent examples. There’s also the doomed Hyperloop, Tesla semitrucks, humans on Mars by 2025, and even his overinflated DOGE (Department of Government Efficiency) “waste, fraud, and abuse” target dollar amount.

Then there’s the literal timing. Keep in mind that, while facility modifications are underway, the solar facility at the Megafactory is not expected to open until later this year. And Tesla still needs to import the manufacturing equipment from China. Plus, the actual process of building 100 GW worth of solar panels takes time. Can it be done in less than two years? We’ll find out.

Love him or hate him, though, Elon Musk is a brilliant, relentless innovator who doesn’t give up on his visions quickly.

As far as solar goes, Musk and Tesla may not hit their 100 GW capacity goal by 2028. But I wouldn’t bet against the company reaching, say, one-third of that goal in two years. And that would still have a significant impact on the solar industry.

Tesla’s Solar Outlook

If Tesla achieves even half its stated goals, it could be a game changer for the entire solar industry.

So, let’s assume that Tesla does succeed. Its competitors should probably be a bit concerned for a few reasons.

Supply Chain Dominance

Since Tesla plans to manufacture its own solar panels from start to finish in one location, there’s no need to source materials. That eliminates any potential inventory issues, shipping delays, and other bottlenecks that its competitors face.

This puts a lot of pressure on other solar companies to make up lost ground, not only on the delivery and turnaround time Tesla will save because it controls its own supply chain, but also on the costs associated with the supply chain.

Pricing Advantage

Though it doesn’t control its entire solar supply chain just yet, Tesla Energy is still the only national solar company that provides and installs its own panels, inverters, and batteries.

That allows the company to offer low prices for its solar services. For example, Tesla’s solar panels cost, on average, $2.90 per watt. The national average, according to SolarReviews, is $3.03. When you’re talking about systems that range from 4.8 kilowatts (“kW”), or 4,800 watts, up to 19.2 kW, those few cents make a huge difference in price.

Integrated Solar Ecosystem

Since Tesla’s solar systems use their own solar panels, inverters, and Powerwall batteries, Tesla avoids paying solar rivals like SolarEdge Technologies (SEDG), Enphase Energy (ENPH), or Growatt for equipment used in Tesla installations.

Offering a full ecosystem of solar products that are designed to work together is also an appealing selling point for customers.

For investors, Tesla has been a popular, heavily traded stock for years. Whether you hold Tesla – and Elon Musk – in a positive or negative light, it can’t be disputed that this is a generational, iconic brand that consistently innovates, even if its ambitions sometimes defy reality. Musk is always looking to go bigger, better, faster, more efficient, and where no one has dared to go before.

If you’re looking to invest in Tesla, keep in mind that the company has never paid a cash dividend on its common stock. Rather, it reinvests its earnings to keep the company growing and innovating.

Tesla appeals to growth-oriented investors seeking long-term capital appreciation rather than immediate yield. Evaluate the stock with this strategy in mind.

Here’s a look at Tesla’s stock performance over the past five years. It has been a bumpy ride, but it has roughly doubled in that span.

Tesla Energy’s planned solar facility at the Megafactory campus in Texas makes it well-positioned not only to make major waves in the solar industry but possibly to take it over if Musk’s vision of 100 GW of production capacity by 2028 becomes reality.

Regards,

David Engle

Editor’s note: There’s one stock you should buy now above all others, according to Altimetry’s Rob Spivey. He shares the name of the company, its ticker, and the reason why it has the potential to at least double in the coming weeks and months – and it could do a lot more.

It’s all linked to fascinating research that his private institutional firm, Valens Research, has carried out on 3,000-plus stocks and more than 40,000 data points. These guys count the very biggest money managers in the world as clients – you should take a look at this stock pick today.

Recent Articles

How to Invest in Anthropic Stock Before Its IPO: 7 Ways to Buy Into the AI Company Behind Claude

Meta’s ‘Clean Energy’ Exit Signals These AI-Power Stocks Could Surge on Demand Boom