Key Points

- AMD reported blockbuster first-quarter earnings, sending the stock up roughly 21% in less than 24 hours as revenue, profit, and free cash flow posted strong double-digit growth.

- Surging demand for AI infrastructure fueled major growth in AMD’s data-center segment, driven by its Instinct GPUs, EPYC CPUs, and partnerships with companies including OpenAI and Meta Platforms.

- Although AMD still trails Nvidia in GPU market share, its lower-cost, open-source strategy and improving performance are helping it gain ground as customers look for alternatives to Nvidia’s ecosystem.

It’s safe to say that the market reacted favorably to Advanced Micro Devices’ (AMD) earnings call on Tuesday.

Shares climbed roughly 7% in after-hours trading that evening. And by 9:45 a.m. on Wednesday, AMD stock absolutely popped, hitting $430.15 after closing at $355.26 the day before.

That’s a 21% gain in less than 24 hours and demonstrates just how impressive AMD’s first-quarter 2026 performance was.

As expected, there was plenty for investors to love about AMD’s results. Let’s look at the year-over-year highlights on a non-GAAP basis (and there are plenty):

- $10.25 billion revenue, up 38%

- $5.69 billion gross profit, up 42%

- $2.54 billion operating income, up 43%

- $2.27 billion net income, up 45%

- $1.37 diluted earnings per share (“EPS”), up 43%

- 55% gross margin, up one percentage point

- A record $2.6 billion free cash flow, up more than 3 times the previous year

AMD also projected its second-quarter revenue to reach $11.2 billion, which would be a 46% year-over-year increase. Needless to say, the market reacted quite favorably to that projection.

Let’s look at what fueled AMD’s stellar first quarter, where things stand competitively against rival Nvidia (NVDA), and the latest outlook for AMD’s stock.

Data Centers, AI, and PCs Drove Revenue Gains

AMD’s CEO, Dr. Lisa Su, summed up the company’s first three months, stating during the earnings call that AMD’s success was “driven by accelerating demand for AI infrastructure, with Data Center now the primary driver of our revenue and earnings growth. We are seeing strong momentum as inferencing and agentic AI drive increasing demand for high-performance CPUs and accelerators.”

Riding that relentless demand for AI infrastructure, AMD’s Instinct AI graphics processing units (“GPUs”) and EPYC AI central processing units (“CPUs”) drove AMD’s Data Center segment revenue to $5.8 billion, a massive 57% year-over-year gain, and a continuation of its upward trajectory.

The demand for AI infrastructure, especially for inference and agentic AI, shows no signs of slowing down anytime soon. That’s why data centers can’t get enough of AMD’s Instinct MI GPUs and EPYC server CPUs.

That insatiable demand compelled AMD to join other investors in providing $100 million in seed money to RadixArk, a new AI-infrastructure company. This is a clear sign to investors that AMD isn’t settling on chipmaking – it’s looking to become a key player in the expansion of AI infrastructure and large-language-model (“LLM”) deployment.

AMD’s Client (PC) and Gaming segments also experienced significant year-over-year first-quarter gains, up 26% and 11% to $2.9 billion and $720 million, respectively. These gains were primarily driven by AMD’s focus on AI PCs equipped with its Ryzen AI PRO 400 Series processors and AI-powered apps designed to improve efficiency.

AMD’s AI-Focused Partnerships Pay Off in Strong First Quarter

AMD’s outstanding first quarter is a direct result of the company’s forward-thinking AI strategies and partnerships that put it at the center of the AI revolution.

Back in October, AMD and OpenAI announced a 6-gigawatt (“GW”) agreement to power OpenAI’s AI infrastructure. The deal will drive large-scale deployments of AMD technology, “starting with the AMD Instinct MI450 series and rack-scale AI solutions and extending to future generations,” according to AMD. The first 1 GW deployment of AMD Instinct MI450 GPUs is slated for the second half of 2026.

In January, Riot Platforms (RIOT) and AMD agreed to collaborate on transitioning Riot from a bitcoin miner into an AI data-center operator. The 10-year partnership initially called for AMD to deliver 25 megawatts (“MW”) of capacity to Riot’s data center in Rockdale, Texas by May. But earlier this month, the companies agreed to double that capacity to 50 MW, with expansion options for up to 200 MW.

Then, in late February, AMD and Meta Platforms (META) expanded their existing partnership to focus on quickly scaling AI infrastructure and expediting the development and deployment of innovative AI models using up to 6 GW of AMD’s Instinct GPUs.

According to AMD, the first deployment will use a custom AMD Instinct GPU to deliver platforms optimized for Meta’s AI workloads. Shipments supporting the first deployment are expected in the second half of 2026. And, of note, they will be built on the AMD Helios rack-scale architecture, which was developed by both AMD and Meta to “enable scalable, rack-level AI infrastructure.”

The Cost – and Benefit – of Not Being Nvidia

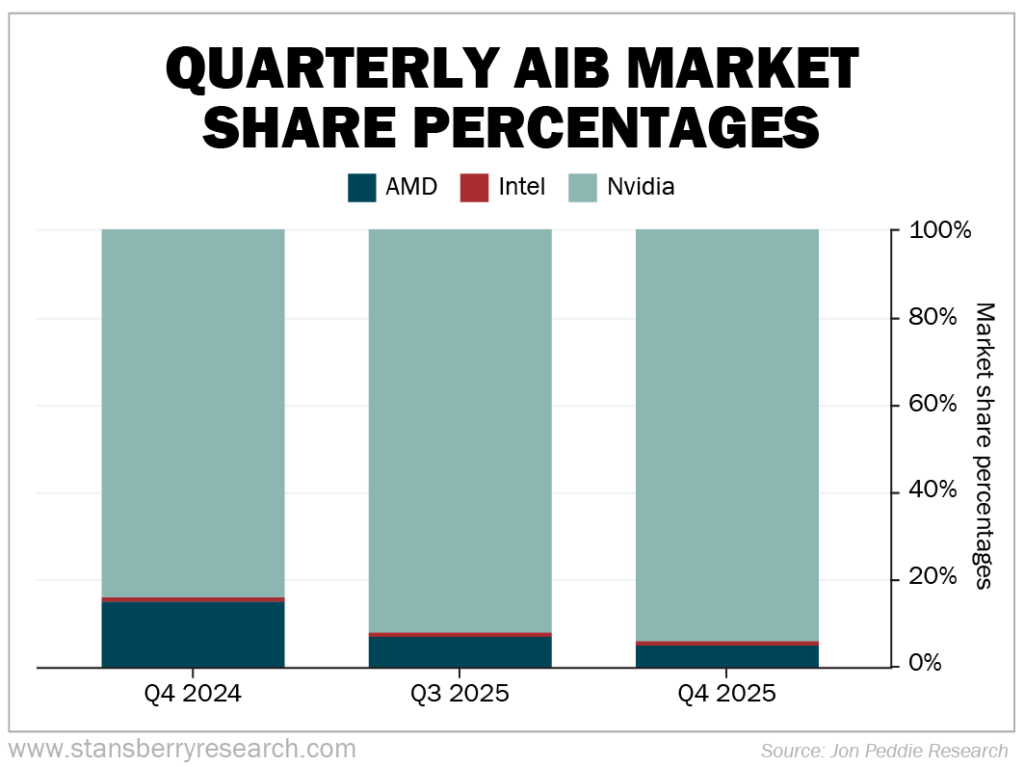

AMD is a significant player in the GPU and CPU world. But make no mistake: AMD is a very distant second to Nvidia in GPU market share.

By the end of the fourth quarter in 2025, Nvidia had claimed 94% of the add-in board (“AIB”) market share to AMD’s 5%. (An AIB is a circuit board added to a computer’s motherboard expansion slot to enhance graphics, memory, and other capabilities – like a GPU.)

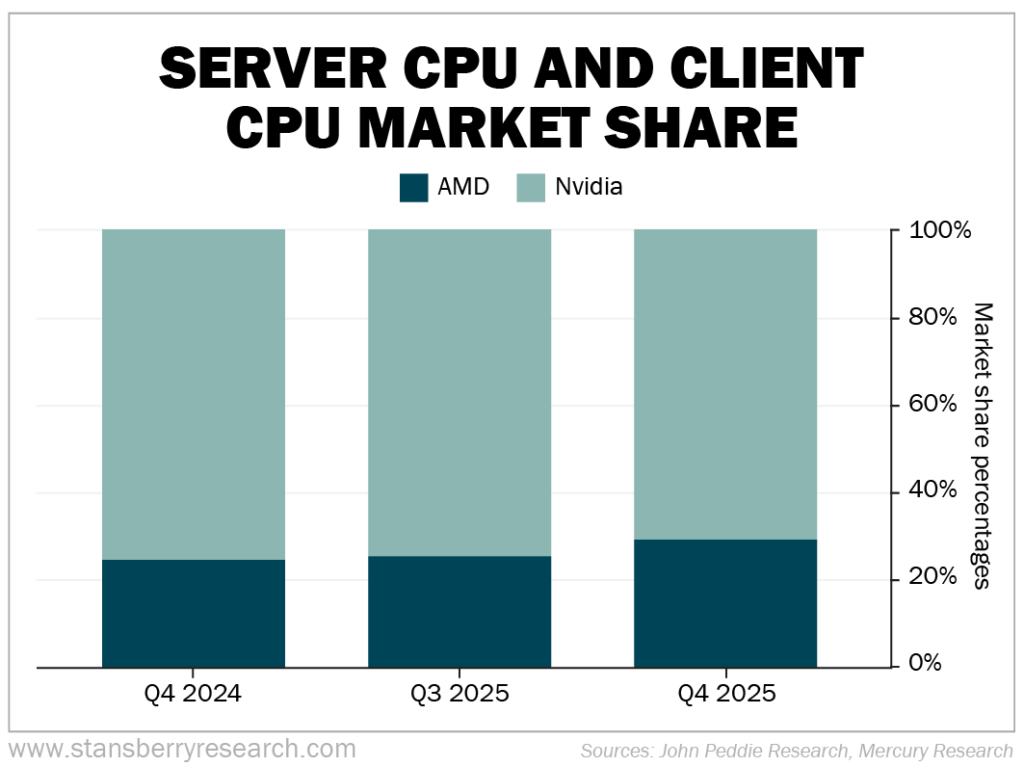

It’s also worth noting that AMD was second, by a large margin, to American chipmaker Intel (INTC) in server CPU and client CPU market share. In last year’s fourth quarter, AMD captured 28.8% of server CPU market share and 29.2% of client CPU market share compared to Intel’s 71% and 70.8%, respectively. But AMD has gradually eaten into Intel’s lead in each category over the past few quarters.

While Nvidia’s grip on GPUs appears insurmountable, AMD is making some inroads.

For more than a decade, the hyperscalers – Amazon (AMZN), Microsoft (MSFT), Meta, and Alphabet (GOOGL) – have allocated much of their spending to Nvidia GPUs, to the point where Nvidia became, in a sense, the default AI-computing provider.

Which seems reasonable. After all, Nvidia established itself as the gold standard of AI infrastructure long ago by delivering a full-stack ecosystem of hardware, CUDA software, and networking. And with that gold-standard label comes a measure of price control.

This is what’s commonly known in the tech industry as the “infrastructure tax,” a premium customers pay to secure the best available computing power. Even if it means sacrificing profit margins to cover Nvidia’s high price points.

At this point, there’s no reason to believe Nvidia won’t raise prices on its Blackwell and Rubin chips. Heavy demand for agentic and generative AI workloads warrants that rationale.

However, there has been a growing movement for companies to diversify their AI infrastructure and avoid vendor lock-in. Even if it means moving away from Nvidia.

This has led some hyperscalers to create AI accelerators tailored to their workloads. A few examples include Google’s TPU, Microsoft’s Maia, and Amazon’s Trainium.

But this movement has also resulted in increased adoption of AMD’s products – especially its GPUs. Companies are seeing a favorable price-to-performance ratio in AMD’s products, such as its Instinct MI300X and MI350 GPUs, which offer lower prices and greater AI-infrastructure flexibility, helping customers get the best value for their money.

For example, Nvidia’s Blackwell B200 chips cost between $35,000 and $40,000 per GPU. Meanwhile, AMD’s Instinct MI350 chip costs roughly $25,000 while offering competitive performance relative to Nvidia’s GPUs.

But AMD is also standing apart from Nvidia for its Linux performance and open-source ROCm platform (versus Nvidia’s closed CUDA platform) that helps developers mitigate lock-in to Nvidia’s CUDA software.

Nvidia still dominates the AI space, but AMD is certainly keeping CEO Jensen Huang and company on their toes as AI infrastructure accelerates.

AMD Stock Outlook

The stock has been on fire for months. After its massive post-earnings bump, AMD is up roughly 101% since the end of March.

Let’s go back even further. One year ago, on May 6, AMD closed at $98.62. On May 6 of this year, AMD closed at $421.39. That’s growth of more than 327%.

We went through the many reasons that AMD stock is flying high, much of it driven by the company’s strong first quarter.

But there are reasons to be excited by AMD moving forward as well. Along with its data-center successes, AMD is focused on growing its presence in the booming AI PC market.

According to Gartner research from August 2025, AI PCs were projected to account for 31% of the entire global PC market by the end of 2025. By the end of 2026, AI PCs may represent roughly 55% of all PCs. And by 2029, Gartner believes that AI PCs will “become the norm.”

Grand View Research went a step further, estimating that the global AI PC market will reach nearly $282 billion by 2030, up from just over $51 billion in 2024. The market is also projected to grow at a compound annual growth rate (“CAGR”) of 34.4% through 2030.

That signals reliable future income for AMD, as it just launched the Ryzen 9 9950X3D2 Dual Edition processor, which AMD boasts is “the world’s first desktop processor with dual AMD 3D V-Cache technology.” In other words, it’s incredibly fast and powerful, which is perfect for high-level gamers, content creators, and developers.

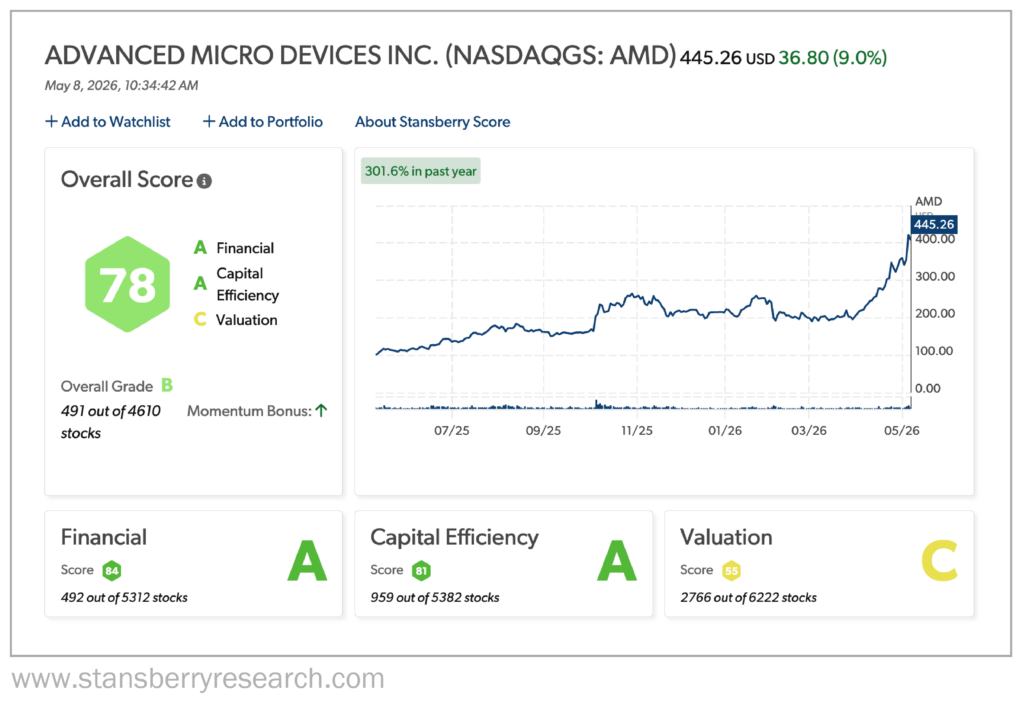

It has already been an exciting year for AMD, as evidenced by its stock’s performance thus far. Its Stansberry Score, a tool that helps determine the quality and long-term value of thousands of stocks, isn’t all that surprising.

AMD stock earns an overall “B” grade thanks to its outstanding Financials (“A”), which I covered earlier, and its Capital Efficiency (“A”), which is worth highlighting.

Unlike other chipmakers, AMD does not manufacture its own products. It outsources most of its production to Taiwan Semiconductor Manufacturing (TSM), saving AMD billions in capital expenditures (“capex”) by not having to build its own fabs, for example.

This ensures high margins on AMD’s products. Just look at the company’s 55.4% gross margin in the first quarter as an example.

And that leads to strong free cash flow, which allows AMD to reinvest in research and development without taking on high-interest loan debt.

Between its growing data-center revenue, expanding AI PC assortment, and many strategic partnerships, AMD has set itself up for success in 2026 and beyond.

Of course, there’s no guarantee AMD stock will continue its upward climb. In fact, given its mind-blowing growth over the past year, valuation concerns are likely to creep in eventually.

But as long as AI continues to grow at a staggering pace, there should be strong demand for AMD’s products and services. And cases don’t get much more bullish than that.

Regards,

David Engle

Editor’s note: As America celebrates its 250th birthday, a Wall Street legend is sounding the alarm. Whitney Tilson (the hedge-fund manager CNBC dubbed “The Prophet”) says the AI revolution is rewriting the rules of wealth faster than most people realize.

Some investors are already seeing extraordinary gains. Others are being wiped out. Tilson says the next six months will determine which side you end up on – and he’s sharing exactly what to do about it in his free presentation here.