Image Credit Associated Press

You don’t see many opportunities that could potentially offer 100X returns in a few years.

Even rarer is to find a 100X opportunity spelled out in a government application with the Federal Communications Commission (“FCC”). But that’s exactly what Elon Musk’s SpaceX did, earlier this year, for something called the “SpaceX Orbital Data Center System.”

The numbers buried in its FCC filing are startling…

SpaceX asked the government for permission to launch a constellation of up to 1 million satellites. Each one would carry specialized artificial intelligence (“AI”) chips, act as a mini data center, and link to its neighbors with lasers to form a single, planet-circling computing network.

For perspective, SpaceX had around 9,400 Starlink satellites in orbit at the time of its application. One million satellites represent a 106-fold jump in fleet size.

Renowned tech investor Jeff Brown, founder of Brownstone Research, has spent much of 2026 writing about this filing.

He calls the idea ‘Orbital AI.’ And he believes it explains a corporate maneuver just days after the FCC filing that puzzled most of Wall Street: the $1.25 trillion merger between SpaceX and Elon Musk’s AI company, xAI.

Jeff couldn’t understand why the story – the largest mergers-and-acquisitions transaction in history – wasn’t getting more attention.

As he wrote the day after the merger was announced:

Not only is it the largest deal, but it is the combination of two of the most transformational companies in history. One would think it would be on the front page of every news outlet.

And yet, the story only made the sidebar of the print edition of the Wall Street Journal… And it didn’t even make the front page of the Wall Street Journal website. Or even the front page of the “tech” section of the WSJ.

How’s that for media bias?

What comes next could be the biggest wealth-building opportunity since the release of generative AI. And to help you make sense of it, Jeff personally explains his 106X Orbital AI prediction in an exclusive video, which you can watch for free by clicking right here.

Or continue reading this guide as it walks through what ‘Orbital AI’ actually means:

- We’ll explain why data centers on Earth are hitting three major problems that space can help solve.

- We’ll lay out why Jeff thinks the SpaceX/xAI tie-up is really about the vertical integration required to move what most folks think of “the cloud” into orbit.

- And finally, we’ll show why the next generation of Musk’s Starship rocket is so important to making this opportunity happen – and at such an incredible scale that almost no one is grasping today.

Wall Street analysts estimate this new technology could be responsible for a wealth explosion of up to $12.8 trillion. And right now is your chance to learn more before the rest of the market catches up.

Table of Contents

The 3 Big Ideas Behind Jeff Brown’s 106X Orbital AI Prediction

Before we go deeper into each of these ideas, we want to summarize why three pieces of Jeff Brown’s 106X ‘Orbital AI’ thesis matter most.

First, AI is currently in the process of breaking Earth’s power grid…

Data centers already draw more electricity per year than some entire countries, and they need millions of gallons of water per day to keep chips from melting.

Local communities are pushing back. New sites sit in permitting limbo for years. Consulting firm McKinsey & Company projects demand for data-center capacity will almost triple by 2030… and the physical world simply can’t keep up.

Second, Musk’s acquisition of xAI was not, as the press claimed, a rescue.

Jeff Brown’s reading of the SpaceX FCC filing and the leaked internal reasoning is that SpaceX bought xAI to feed its orbital data-center system. Musk is putting rockets, satellites, computing power, and AI models all under one roof.

The goal is a 1-million satellite constellation in sun-synchronous orbit. It will be powered by the sun, cooled by the vacuum of space, and communicate with lasers.

Third, none of this works without cheap launches, which only SpaceX can provide at this time.

For decades, sending a kilogram to low Earth orbit has cost tens of thousands of dollars. SpaceX’s Falcon 9 already dragged that figure down to about $2,500. Starship Version 3, which began commercial operations this year, aims to push the cost below $200 per kilogram by 2027 and below $100 by 2028.

That’s the price point at which it becomes cheaper to put a server farm in orbit than to build one in Northern Virginia.

Stacked together, these three shifts are what Jeff calls a $12.8 trillion opportunity.

Earth’s Data Centers Are Hitting 3 Major Bottlenecks

Most folks never think about what happens behind the scenes when you ask an AI chatbot like ChatGPT or Claude a question…

With every single query, a data center somewhere fires up a rack of chips to generate your answer. That takes power – a lot of power. AI is one of the most resource-intensive industries ever built.

As Jeff’s senior analyst wrote in March:

Since the release of ChatGPT in late 2022, NVIDIA estimates that token generation demand per AI task has increased 10,000x. At the same time, overall model usage has surged 100x. Together, that implies a 1,000,000x increase in compute demand in just a couple of years.

A millionfold increase in demand… in just three years.

All that computing power must live somewhere – and get power from somewhere.

A recent analysis by my colleague David Engle (citing Deloitte) estimated that AI data-center power demand in the United States alone could grow by nearly 3000% between 2024 and 2035, jumping from 4 gigawatts to 123 gigawatts. That’s roughly enough electricity to power every household on the East Coast.

And that’s solely AI’s share of electricity growth. Total data-center demand is set to climb even higher.

Jeff’s team has run similar numbers in his own writing. They walked readers through the math on a single next-generation Nvidia rollout:

Now consider the power draw. Each of these racks consumes approximately 200 kilowatts. Multiply that across the full deployment, and we’re already at 25 gigawatts of electricity demand just to run the compute hardware.

But that’s only part of the story. Modern AI data centers require advanced cooling systems, networking infrastructure, and redundancy layers. When we account for total facility overhead using a typical power usage effectiveness (PUE) factor of 1.3, total demand rises to roughly 32 to 33 gigawatts.

And that’s just one chipmaker’s gear. Layer in competing AI chips from Advanced Micro Devices (AMD) and the custom chips built by Alphabet (GOOGL), Amazon (AMZN), and Microsoft (MSFT) – and Jeff estimates the sector is heading toward 60 to 65 gigawatts of new demand.

The U.S. power grid simply wasn’t designed for that. It was designed for a world where electricity demand grew slowly and predictably. So, when a single new facility can consume the equivalent of a small city, grid operators cannot meet that need right now.

And of course, power is only half of the data center problem. The other half is heat.

Modern AI chips run hot, far hotter than your laptop.

As David wrote last year about data centers:

These facilities also generate extreme heat. Graphics processing unit (“GPU”) packages operating under heavy computational loads can reach temperatures of 105 degrees Celsius. That would be 221 degrees Fahrenheit, more than hot enough to fry an egg.

Left unchecked, the heat will destroy the chip. And the cooling solution for most data-center facilities has been water.

Jeff notes that a single large AI data center can consume 19 million gallons of water per day, roughly the amount a town of 50,000 people uses. Research from the University of California, Riverside has pegged the water cost of a 100-word AI-generated email at about one plastic bottle. As Jeff details in his video:

You don’t need to be some unhinged so-called “environmentalist” for that to concern you.

In fact, figures show that seven in 10 Americans are already affected by drought.

For everyday people, that looks like wildfires, water restrictions, and failed crops for our farmers.

And not surprisingly, all that power and water usage is sparking pushback from local communities.

Across the U.S., local residents are growing increasingly angry about data centers. Protests have shut down data-center proposals in Virginia, Pennsylvania, North Carolina, and other states.

In addition, all that community backlash has led to permitting delays becoming routine. Some projects now wait two or three years just to break ground. Construction backlogs stretch past eight months even when permits are in hand.

I covered the scope of the backlash in a recent piece on the AI data-center rebellion:

Over the past two years, residents have blocked or delayed a staggering $64 billion worth of data-center projects. And roughly 55% of the elected officials who have spoken out against data centers are Republicans, not Democrats.

The backlash here isn’t along the usual political fault lines.

It’s widespread… made up of regular folks worried about their water, their electric bills, their property values, and whether their elected officials are cutting deals behind closed doors.

And we predict the data-center backlash will grow much more significant, much more volatile, and far more violent.

But all these problems either shrink or disappear if you move the whole operation a few hundred kilometers straight up.

And according to Jeff’s analysis, solar panels in sun-synchronous orbit generate about five times more electricity in space than they do on the ground. Power costs for space-based systems trend toward free over the life of the panel.

As SpaceX described it in the context of its FCC filing:

By directly harnessing near-constant solar power with little operating or maintenance cost, these satellites will achieve transformative cost and energy efficiency while significantly reducing the environmental impact associated with terrestrial data centers.

Cooling works differently in orbit, too.

There’s no air, so there’s no need for water-based systems. Radiator panels dump heat into the near-absolute-zero vacuum, just as satellites have for decades.

And communities can’t easily protest satellites that fly 300 kilometers overhead. There are no zoning hearings in orbit. There’s no NIMBY lobby, short for “not in my backyard,” in the exosphere. Regulation still exists, but it runs through the FCC’s satellite licensing process, not a patchwork of local boards.

Jeff’s team summed up the advantages of data centers in space last month:

Once Starship drives launch costs down toward $100 per kilogram – which we believe is achievable by 2028 based on the current trajectory – the economics of compute begin to shift in a way most investors aren’t prepared for.

At that point, orbital AI data centers will be the most cost-efficient way to generate AI compute.

No land constraints. No grid bottlenecks. No cooling limitations. No permits to worry about.

And frankly, if SpaceX can make this happen, it could mark a whole new economic shift into space… and perhaps even a civilizational-level shift.

From SpaceX’s FCC filing:

Launching a constellation of a million satellites that operate as orbital data centers is a first step toward becoming a Kardashev Type II civilization – one that can harness the sun’s full power – while supporting AI-driven applications for billions of people today and ensuring humanity’s multiplanetary future among the stars.

Musk is pushing hard. And the timeline is aggressive, even for Musk.

I’ve written about the same divide in a slightly different way.

In a recent piece on the data-center backlash, I noted:

For some, the AI boom has the potential to be one of the biggest creators of wealth in their lifetime. For everyone else, it will likely be a nightmare. This is how Elon Musk can simultaneously build the most powerful AI supercomputer on Earth in a Memphis warehouse while preparing for the largest technology IPO in history with SpaceX (you can learn more about how to get pre-IPO access here).

Only Musk has the kind of resources to push this problem forward at scale. He has the rockets, the satellites, the chips, and the AI lab.

Of course, several other companies are also testing orbital data centers, as David Engle noted earlier this year.

- Starcloud, based in Washington state, launched a satellite carrying an Nvidia H100 GPU in November 2025. The chip ran AI queries in orbit.

- Google has announced its Project Suncatcher, with two prototype satellites scheduled for early 2027.

- Aetherflux is aiming at a commercial launch in the first quarter of 2027.

- And of course, Jeff Bezos, through Blue Origin, filed his own FCC application in March for a 51,600-satellite constellation called Project Sunrise. (But as I wrote recently, Blue Origin has its own problems with putting satellites in orbit.)

All these efforts, however, rely on one thing to make the numbers work at scale: launch costs that are cheap enough that the rockets stop being the limiting factor. And only one rocket company is nearing that price point…

The Biggest Pivot of Musk’s Career

When SpaceX announced in February that it was acquiring xAI in a merger worth $1.25 trillion, the largest ever, most financial reporters treated the deal as a rescue.

After all, xAI had burned through cash trying to catch up to OpenAI and Anthropic. Meanwhile, SpaceX was profitable and flush. The logic seemed obvious: SpaceX bailed out its sister company.

But Jeff’s reading was something totally different…

In his view, SpaceX didn’t buy xAI to save it. SpaceX bought xAI because that was the most obvious way for Musk to turn his orbital plans into reality.

As Jeff put it in his video describing the Orbital AI opportunity:

[xAI] was 21 times faster to market than OpenAI.

And the company’s valuation grew at the same breakneck speed.

That initial funding round valued the company at just $673 million…

But at the time of the merger with SpaceX, the company was valued at a huge $250 billion.

It’s not exactly what I’d call a bailout!

If you were an early investor in xAI, you would have already seen your initial investment grow some 37,000%, depending on dilution and later fundraising terms.

And what’s coming next with the combined SpaceX and xAI companies is incredible. The FCC application spells out what Musk wants to do.

As Jeff summarized at the time…

The scope of the application is breathtaking – so grand as to almost be unbelievable.

SpaceX is proposing to have an orbital data center constellation of up to 1 million satellites.

Each satellite will act like a mini-data center, full of GPUs for training and running AI applications.

They will all be interlinked via optical connections, creating a massive, distributed, interconnected data center in a sun-synchronous orbit around Earth.

The satellites will operate between altitudes of 500 to 2,000 kilometers in orbits that maximize exposure to the sun for constant power generation.

For context, the Starlink constellation at the time was roughly 9,400 satellites – and it has grown to a little more than 10,000 satellites in the months since.

The proposed Orbital AI constellation would be more than 100 times the scale of today’s Starlink fleet. And the AI satellites would also be individually larger than Starlink satellites, allowing them to carry more computing power.

As Musk noted in a statement announcing the xAI acquisition:

Current advances in AI are dependent on large terrestrial data centers, which require immense amounts of power and cooling. Global electricity demand for AI simply cannot be met with terrestrial solutions, even in the near term, without imposing hardship on communities and the environment.

In the long term, space-based AI is obviously the only way to scale.

Musk and Jeff are both looking at the merger not as a bailout, but as vertical integration. SpaceX supplies the rockets and the satellites. xAI provides the AI models, compute demand, and engineering talent that know how to squeeze performance from GPUs.

Combined, they have the potential to build an Orbital AI computing platform that is straight out of science fiction. And if it succeeds, then Musk would control the largest globe-spanning infrastructure project – a space-based Internet.

And it doesn’t seem likely that any other company will be able to replicate Musk’s plan, at least any time soon.

The closest deep-pocketed competitor is Jeff Bezos’ Blue Origin.

As I noted in March, Amazon filed a 17-page petition with the FCC urging them to block SpaceX’s Orbital AI application.

Amazon’s argument went something like this: Deploying a million satellites would take more than 220 years at the current pace of global launches. Amazon also warned that approving SpaceX’s application would give the company near-total control over insertion orbits, forcing every other operator to plan around a constellation that might never exist.

It’s unlikely Amazon’s attempt to slow down SpaceX will work. And Blue Origin has its own problems. After all, Elon Musk has claimed that SpaceX will launch more than 95% of all mass that goes to orbit this year.

If Amazon wants an Orbital AI constellation of its own, it will need to lean heavily on Musk’s rockets. While Blue Origin has an operational New Glenn rocket larger than SpaceX’s Falcon 9, it flies much less frequently.

I wrote about this dynamic myself after Blue Origin’s failed April launch in a piece on the space race:

While Blue Origin teams are picking through telemetry to find out what went wrong, SpaceX is going to keep launching rockets – one after another, and at a level of reliability and scale that no one else on Earth can touch.

As of Blue Origin’s launch this past weekend, SpaceX had completed 47 Falcon family launches in 2026 alone. That’s more missions in less than four months than every other American rocket company combined will manage all year.

Musk is playing for all the marbles – and for SpaceX and xAI to beat everyone else in AI.

To understand the scale of what SpaceX is actually attempting, consider the numbers Musk laid out at a recent TeraFab announcement.

Jeff summarized them in an April 2026 Bleeding Edge issue:

SpaceX will scale to launch 10 million tons of mass per year into Earth’s orbit.

This will be required to get to 1 terawatt a year of orbital power generation to enable SpaceX’s orbital web services (OWS) plans, with its 1 million orbital AI data center satellites.

A terawatt is a staggering amount of power. It’s 1,000 gigawatts, far more than what AI data centers are projected to consume on Earth by 2035. SpaceX aims to put it all into orbit.

But none of it happens without rockets cheap enough to get the satellites up there.

Why Starship Is the Cornerstone of Orbital AI

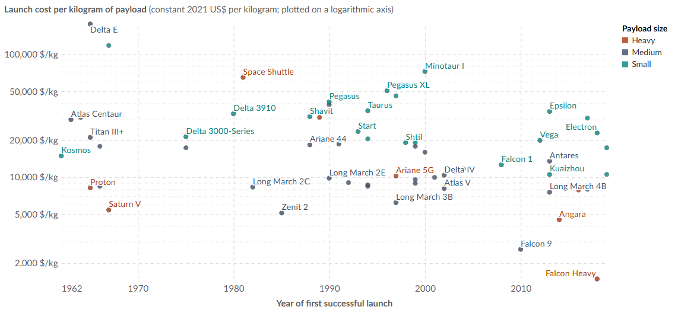

Orbital AI lives or dies on one number: cost per kilogram to orbit.

For most of the space age, that number was brutally high.

Our World in Data has a great chart that maps out the approximate launch cost per kilogram since the 1960s:

Until the early 2000s, costs remained high, as shown above, especially for higher payload sizes. As a result, satellites were primarily launched by governments. Private companies had a tough time affording the rides.

Then SpaceX showed up.

The Falcon 9 was introduced in 2010 and made routinely reusable by 2017. It dragged the cost down to as low as $2,500 per kilogram for paying customers. And keep in mind, that’s what SpaceX charges. The actual internal cost is considerably lower.

The Falcon Heavy, essentially three Falcon 9s strapped together, brought down the price for some payloads even further.

But $2,500 per kilogram still isn’t cheap enough for orbital data centers at scale. A single AI satellite with solar panels and radiators might weigh 1,000 kilograms or more. When multiplied by 1 million satellites, even Falcon 9 pricing would cost trillions.

That’s where Elon Musk’s new Starship rocket comes in.

As Jeff framed it after watching a Starship test flight:

SpaceX is designing for simplicity and performance. The team isn’t just trying to put a Starship in orbit, which is easy for them to do today.

SpaceX is optimizing its technology and its heat shield to do the impossible. Rapid reusability, safe enough for passengers, and sub $100 per kilogram launch costs, which will ignite a booming space economy.

The phrase “ignite a booming space economy” is key here. If Starship can succeed, then Orbital AI is inevitable. And more…

Starship is a fully reusable super-heavy-lift launch vehicle. The booster lands itself. The upper stage returns intact. And then both can fly again with less refurbishment than the Falcon class.

Version 2, which flew throughout 2025, carries up to 150 metric tons to low Earth orbit. Version 3 is even bigger.

As Jeff described it last fall:

Starship V3 will add another 15 or so meters in height and several additional Raptor engines to the Starship itself.

The payload will increase to 200 tonnes to low Earth orbit (LEO), compared to a maximum of 150 tonnes for V2.

It will be capable of missions to both the Moon and Mars, as well as launching version 3 of Starlink satellites at 350 kilometers of altitude, which is a lower altitude than the current Starlink satellites, enabling sub-20 millisecond latency. That level of performance will be indiscernible to almost all from land-based fiber optic broadband internet solutions… and it’s delivered from space.

More capacity per launch means lower cost per kilogram. And Jeff has been closely tracking Starship’s commercial debut.

He predicts that initial launch costs per kilogram to low Earth orbit will be less than $1,000 this year… below $200 in 2027… and down to $100 by 2028.

[Full story: Watch Jeff’s prediction here.]

That $200 number is the threshold at which Jeff believes putting servers in orbit becomes cheaper than building equivalent capacity on Earth, factoring in land, power, water, permitting, and construction costs. Former NASA physicists and researchers at Google have reached similar conclusions.

And while skeptical readers might wonder whether this is wishful thinking, there’s a concrete data point available.

Voyager Technologies (VOYG) disclosed in March that it contracted a 2029 Starship launch for its Starlab commercial space station for $90 million.

That’s wildly inexpensive, considering that the Artemis II mission around the moon earlier this year cost NASA more than $4 billion.

Jeff’s back-of-envelope math puts Starlab at roughly 147,000 kilograms, which works out to about $612 per kilogram. That’s about a 75% discount to Falcon 9. And SpaceX is already building a facility called Gigabay that will manufacture up to 1,000 Starships per year.

That’s not to say that anything about this timeline is guaranteed. Nothing is.

Rockets explode, timelines slip, and Musk has a long history of blowing past his own deadlines.

But if you’re an investor and you’re not wildly optimistic about the potential of space, then I believe you’ll regret it in the coming years.

Each successful launch makes the next one cheaper, and every booster that lands intact further trims the fixed-cost base.

And when the cost per kilogram breaks below $200, as Jeff and Musk both predict for 2027, the calculus flips. Orbital AI starts becoming the most efficient way to build AI infrastructure, anywhere.

As Jeff noted in his video, which you can watch for free here:

With ‘Orbital AI,’ I believe we’re about to witness another paradigm shift.

One that could change the entire future of humanity…

And provide a once-in-a-lifetime wealth-building opportunity if you’re positioned correctly.

That time is now, if you’re interested in learning more… And if you’ve already read enough and are ready to check out Jeff’s work, click here to go directly to the order form for his Near Future Report. (This link does not go to a long video.)

What Is Brownstone Research?

Brownstone Research is an independent investment research firm that publishes deep-dive reports on technology investing. The company has been tracking Musk’s space plans long before the SpaceX/xAI merger.

The firm’s mission is to help subscribers “thrive amid this era of profound, exponential change driven by today’s tech breakthroughs.” In practice, that means covering AI, quantum computing, autonomous robotics, biotech, and the fast-expanding space economy with a mix of engineering analysis and investment recommendations.

And that tech focus lets the Brownstone team go deeper on esoteric topics like radiation-hardened chip design or the details of Starship’s engines.

A few of Brownstone’s calls over the years are worth noting because they illustrate the firm’s approach to new technologies.

For example, founder Jeff Brown recommended bitcoin to readers in 2015, when it was trading around $240. He called Nvidia an AI play in early 2016, before most financial journalists had connected the dots between GPUs and machine learning. He made a contrarian Tesla recommendation in late 2018, at a moment when most of Wall Street was bearish, and some analysts were predicting bankruptcy within months.

All three of those calls turned out to be spectacular:

- Anyone who held bitcoin from 2015 to its peak saw gains well into the thousands of percent.

- NVIDIA has delivered roughly a 28,000% total return from Jeff’s 2016 recommendation through its peak, according to Brownstone’s tracking.

- And Tesla has delivered more than 2,400% since the 2018 buy call.

Jeff’s way of thinking is important to note, too.

For example, most folks might want a company they own to raise the launch cost as high as possible, to make as much money as possible.

But here’s Jeff breaking down the unit economics of SpaceX’s pricing strategy:

The most ironic part is that SpaceX could charge significantly more for its services and still be the cheapest, safest, most efficient launch provider in the world. What most don’t understand is that SpaceX’s guiding mission is to make the human race a multiplanetary species, and to do so, it needs to achieve incredible scale…

Musk’s target is to manufacture more than 1,000 Starships a year, a mindboggling number, and also practical if the goal is to build a self-sustaining civilization on Mars.

With great scale comes dramatically lower costs per launch. That’s why SpaceX isn’t charging higher prices. Lower prices drive higher utilization, which allows SpaceX to scale more quickly.

That kind of explanation is far more valuable than throwing out stock tips or finding “high-risk, high-reward” small-cap companies. Jeff is explaining exactly why a company’s strategy makes sense… in this case, why Musk and SpaceX care more about scaling quickly to win the space race than they do about maximizing short-term profits. And so far, it’s working.

Brownstone’s business model matters, too.

The company is 100% funded by subscriptions. It’s not a brokerage or a money-management firm… and it certainly doesn’t accept payments from the companies it covers. Its revenue comes solely from readers like you, when you hear about an idea Brownstone covers and decide to subscribe to Brownstone’s research.

That structure aligns the firm’s incentives with its subscribers…

If the research or recommendations often turn out wrong, folks cancel. If they turn out right, time and time again, then subscribers stay… and even recommend Brownstone’s work to their friends.

Brownstone publishes three main products:

The Bleeding Edge is a free, daily e-letter.

It generally covers one tech story per day in enough depth to be useful, and it includes a reader Q&A every Friday. You can read The Bleeding Edge here for free… but it doesn’t include specific stock recommendations.

The Near Future Report is Brownstone’s flagship paid newsletter.

It focuses on larger-capitalization tech investments positioned for mass adoption, published monthly with typically at least one recommended stock opportunity for readers to buy with big potential upside. And it also includes updates and analysis across its model portfolio of prior recommendations.

This letter is also where Jeff hosts all of the special reports mentioned in his 106X Orbital AI prediction video, including…

- The Little-Known Chipmaker Enabling The 106X ‘Orbital AI’ Boom

- Elon’s 25,000% Secret Weapon: The One Stock That Makes Tesla’s Robotic Revolution Possible

- How To Profit From NVIDIA’s New Infrastructure Partner

The normal price for one year of access to The Near Future Report is typically $499. But Jeff does have a special offer available for first-time subscribers to give his work a try. You can click here to go directly to the order form to see that special price and judge Jeff’s work for yourself.

And finally, Exponential Tech Investor covers smaller, earlier-stage tech companies. An annual subscription to Exponential Tech Investor costs $5,000 and is primarily for readers with a higher risk tolerance.

Each of these three letters is personally anchored by Jeff.

His name goes on the recommendations, his analysis drives the content, and his reputation rises or falls with the calls.

Who Is Jeff Brown?

Jeff Brown is the founder and chief investment analyst at Brownstone Research. His background is unusual for someone in the financial publishing industry, and it shapes how he approaches his work.

Most investment analysts come from Wall Street, business school, or journalism. Jeff came from the technology industry itself.

He spent more than 25 years as a senior executive at major tech companies. That includes leadership roles at Qualcomm (QCOM), the wireless chipmaker that owns much of the intellectual property behind modern smartphones. He worked at NXP Semiconductors (NXPI), a major supplier of automotive and Internet-of-Things chips. He also held senior positions at Juniper Networks, the networking giant that was acquired by Hewlett Packard Enterprise (HPE) in the summer of 2025.

That variety of roles means Jeff was in the meetings where product road maps were approved and revenue targets got set. He watched new technologies graduate from whiteboards to commercial products. He saw firsthand which ideas had real engineering foundations and which were hype.

That background shows up when he analyzes a company like SpaceX.

He’s not guessing whether Starship’s engineering will work. He’s drawing on decades of experience watching hardware timelines and knowing what counts as a realistic delivery date versus an aspirational one.

Jeff is also a prolific angel investor. Over the years, he has backed hundreds of private tech companies. Some of those investments produced returns that sound unbelievable if you haven’t seen the documentation. He has publicly discussed gains of 5,000%, 7,300%, and 11,300% on select private deals.

Jeff’s educational background is a mix of engineering, business, and law…

- He studied aeronautical and astronautical engineering at Purdue University… which means he has a literal rocket-science degree.

- He earned a master’s in management from the London Business School.

- He also completed executive programs at the Yale School of Management, MIT, Stanford, and UC Berkeley’s School of Law.

That combination is rare. It means Jeff can read a technical FCC filing, assess the engineering feasibility, and simultaneously understand the corporate structure and regulatory hurdles involved.

Jeff has also lived abroad extensively, including a long stretch in Tokyo. He speaks at international conferences and has advised U.S. government agencies, including the Department of Commerce, the National Institute of Standards and Technology, and the Defense Intelligence Agency, on emerging technologies.

In 2015, he transitioned from tech executive to financial publisher. The motivation, by his account, was frustration that ordinary investors typically learn about transformative technologies only after the big gains have been captured by insiders.

His goal with Brownstone was to help change that by writing for a public audience about what was coming, and not what had already happened.

His calls on bitcoin, Nvidia, and Tesla are the most famous examples. But the broader project has always been the same… He finds a technology that’s poised for mass adoption, identifies the companies best positioned to benefit, and writes about them in enough detail that readers can make their own decisions.

Right now, that’s SpaceX – and specifically Orbital AI.

Jeff has been more enthusiastic about Orbital AI than almost any other recent thesis. And he’s telling his subscribers that the 106X build-out of Starlink is the biggest structural opportunity he has identified since his Nvidia call in 2016.

The Opportunity in ‘Selling Shovels’ During a Data-Center Boom

Before judging whether Jeff’s Orbital AI thesis is realistic, it’s worth looking at what happened with the last major data-center build-out on Earth.

From 2022 through early 2026, AI demand triggered one of the largest infrastructure expansions in modern history. Companies raced to build server farms, secure power contracts, and lock in cooling capacity. And typically, their stock prices surged.

For example…

Vertiv Holdings (VRT) supplies power management and cooling systems for data centers. It’s the type of company most retail investors had never heard of in 2022. The stock traded around $14 at the start of 2023.

By early 2026, Vertiv was trading near $255, a more than 1,700% increase. The business hadn’t changed fundamentally. The product catalog was similar. What changed was demand. Every new AI data center needed Vertiv’s cooling and power infrastructure, and the backlog piled up faster than the company could fulfill it.

Investors who caught Vertiv in 2022 or early 2023 participated in one of the cleanest infrastructure trades of the decade.

Powell Industries (POWL) makes heavy-duty electrical equipment for industrial customers, including data centers. It’s not a glamorous company. It’s a switchgear and substation builder.

Over the three-year data-center build-out, Powell’s stock climbed roughly 1,683%. Again, the business did what it had always done. The difference was volume. AI data centers bought so much switchgear that Powell couldn’t keep up with demand.

Celestica (CLS) is a Canadian contract manufacturer that builds server racks for data centers. The racks themselves don’t sound exciting. Each one, however, holds roughly $3 million worth of AI chips. Get the rack wrong, and the chips don’t work.

Celestica’s stock jumped more than 2,800% over the AI build-out.

But not every AI data-center supplier was necessarily a winner.

Super Micro Computer (SMCI) was Nvidia’s primary server-rack partner during the early stages of the AI boom. Its stock went parabolic, posting gains of more than 3,300% at its peak.

Then Super Micro ran into trouble. Accusations of accounting irregularities, alleged family self-dealing, and questions about sanctions compliance hit the company in 2024. Nvidia began redirecting shipments to other partners, and then the stock collapsed.

The Super Micro arc illustrates two things:

- First, the suppliers during a major tech build-out can deliver extraordinary returns.

- Second, picking the right company matters. Generic sector exposure is not the same as identifying the actual beneficiary of a partnership.

And the parallel to Jeff’s Orbital AI thesis should be obvious…

The 2022-2026 AI data-center boom was driven by a single technological breakthrough, AI, and a single bottleneck, compute capacity. Every company supplying that bottleneck saw a demand surge. The biggest winners were the picks-and-shovels businesses most investors had never heard of.

Jeff’s argument is that Orbital AI represents the next iteration of the same pattern. The technology is similar: rack up chips, power them, cool them, and network them together.

The difference is that the infrastructure is now in orbit rather than in Northern Virginia.

That means a new set of suppliers will matter:

- Solar panel manufacturers designed for space applications.

- Radiation-hardened chipmakers.

- Optical communications specialists who can build the laser interconnects.

- Launch service providers, though that category is effectively one company, SpaceX, for now.

The engineering challenge alone is enough to dramatically narrow the field.

As Brown explained when Nvidia announced its orbital-ready GPU module:

This system wasn’t designed for Earth. It was designed for orbital AI data centers.

Operating in space introduces a completely different set of challenges. Radiation constantly interferes with electronics, causing errors that can crash traditional systems.

Not all of these suppliers will succeed, of course. Some will fail to scale. Some will be undercut by SpaceX’s vertical integration. Still others will be acquired.

But if the build-out happens at anything like the scale Jeff expects, a handful of winners will emerge.

And that’s why Jeff’s team at Brownstone has been actively identifying those potential winners. In a special report that accompanies The Near Future Report, he focuses on what he calls Musk’s “hidden suppliers” – companies already shipping critical components to SpaceX that most investors don’t know about. You can get access to that report by clicking right here to go directly to The Near Future Report order page.

There are no guarantees in investing. But Jeff’s track record of big wins and transparent analysis makes it easy to think that he’ll find the next big winners as Orbital AI becomes a reality.

Frequently Asked Questions

What exactly is ‘Orbital AI‘?

Answer: ‘Orbital AI’ is the term Jeff Brown uses for AI data centers that operate in low Earth orbit, rather than on the ground.

Each orbital data center is a satellite packed with GPUs, powered by solar panels, cooled by radiating heat into the vacuum of space, and connected to other satellites via lasers.

Together, thousands or millions of these satellites form a single distributed computing network. SpaceX’s FCC filing for up to 1 million such satellites is the concrete proposal driving Jeff’s thesis.

Where does the “106X” number come from?

Answer: It’s the ratio between SpaceX’s Starlink constellation at the time of its FCC application and the proposed 1 million orbital data-center constellation.

One million divided by 9,400 is approximately 106. Jeff uses the number to communicate the sheer scale of what Musk is proposing relative to what SpaceX has already built.

Is the SpaceX/xAI merger really about Orbital AI, or is that just Jeff’s interpretation?

Answer: Musk himself has been explicit. In the statement announcing the acquisition, he described the combined company as “the most ambitious, vertically-integrated innovation engine on (and off) Earth, with AI, rockets, [and] space-based internet.”

Jeff didn’t invent the connection. He simply recognized it before most of the financial press.

When does this actually start happening?

Answer: The FCC filing was submitted in January 2026 and accepted for review. Starship Version 3 is expected to begin commercial operations later this year.

Jeff projects launch costs will drop below $200 per kilogram in 2027 and below $100 per kilogram by 2028. Musk’s own timeline suggests that most new data centers will be built in orbit within three years. Some smaller pilot projects, like Starcloud’s H100 satellite, are already operational.

Who is Musk’s “hidden supplier” that Jeff referenced in his video?

Answer: Jeff reserves the specific name for subscribers to The Near Future Report, so I can’t share it here.

But he has disclosed publicly that the company makes radiation-hardened chips and inter-satellite laser communications hardware. He has also said the company is roughly 148 times smaller than Nvidia and has already shipped 5 billion chips to SpaceX.

Jeff’s report, titled The Little-Known Chipmaker Enabling The 106X ‘Orbital AI’ Boom, contains the name, ticker symbol, and his reasoning. To get immediate access without watching a long video, click here to go directly to the subscription form.

What are the risks in the Orbital AI opportunity?

Answer: There are plenty of serious risks that an investor should keep in mind.

First, Starship could run into technical setbacks that push launch costs higher than projected and take longer than projected. The space industry is hard, and SpaceX’s timelines have slipped before.

Second, the regulatory environment could shift. Orbital debris concerns, filing disputes with competitors like Amazon, or international coordination issues could delay the deployment of 1 million satellites.

Third, the business model still needs to prove itself economically. For example, even if all the engineering works perfectly, if AI-demand growth slows or ground-based power grows cheaper, then the orbital advantage narrows.

Fourth, any specific supplier stock could underperform the sector. The historical parallel with Super Micro shows that picking the wrong suppliers is a real risk even when the overall trend plays out.

Jeff doesn’t pretend these risks don’t exist. His recommendation to size positions carefully and invest only money you can afford to lose always applies, especially here.

How do I actually invest in Orbital AI?

Answer: There are a few options depending on your risk tolerance.

For the overall thesis, you can gain exposure to SpaceX itself through publicly traded companies that hold SpaceX stakes, most notably EchoStar (SATS) and Alphabet (GOOGL). And Jeff has previously found a way for regular investors to claim an even more direct stake in SpaceX before it goes public via an investment vehicle that he’s personally vetted. We published a deep dive on how to get access to SpaceX shares here.

For the supplier thesis, Jeff’s Near Future Report names the specific radiation-hardened chip supplier he believes benefits the most. He also covers suppliers to Nvidia’s new server-rack partner and a handful of other niche players.

For a broader exposure to space as a theme, you could look at exchange-traded funds that hold space industry stocks, but make sure you know what you’re actually getting inside each fund’s portfolio.

What Investors Should Do Now

If Jeff Brown is right about even half of what he’s predicting, the Orbital AI data-center build-out will reshape the technology industry over the next decade.

As he puts it in his video, which you can watch for free by clicking right here…

Some of the world’s top hedge fund managers say this new industry represents a $12.8 trillion opportunity…

That’s more than the current value of PayPal, SpaceX, xAI, and Tesla… COMBINED.

Yet Musk’s “hidden supplier” in this ‘Orbital AI’ revolution is absolutely tiny.

A chipmaker almost nobody has heard of…

One that’s 148 times smaller than NVIDIA.

Yet it could soon become THE major chip-supplier for Musk’s 1 million-plus ‘Orbital AI’ satellites.

The biggest gains from any technology build-out usually go to investors who recognized the trend before it became obvious.

Orbital AI data centers are still, for most readers, a strange concept. That unfamiliarity is itself the opportunity. When every financial news channel is running banner headlines about space-based AI, the big, early returns will likely already be gone.

Jeff’s case for Orbital AI is not that it’s risk-free. It’s that the potential upside is large enough, and the infrastructure commitment is concrete enough, that investors who ignore the trend are likely to regret it later.