Image Credit: Associated Press

Alphabet (GOOGL) and Meta Platforms (META), two of my three longtime favorite tech giants – along with Amazon (AMZN) – reported earnings after the close yesterday.

I’ve been recommending investors own these stocks since April 2019. Since then, through yesterday’s close, they’re up 464%, 274%, and 182%, respectively, versus 146% for the S&P 500 Index.

Let’s take a look at the latest numbers from both of these tech giants – starting Alphabet. (Here are its earnings release and slide presentation)

The company reported $109.9 billion in revenue – up 22% year over year (“YOY”) and 19% in constant currency – beating estimates of $107.2 billion. And Google ad revenue grew a healthy 15.5% YOY.

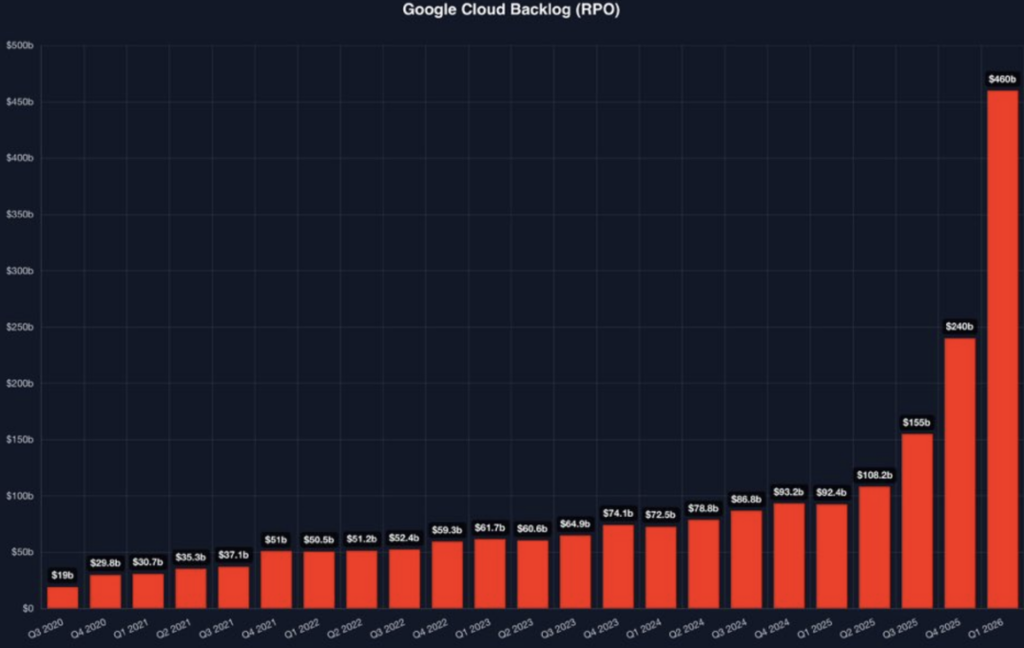

The bigger story was Google Cloud, with $20 billion in revenue – up a staggering 63% YOY. If anything, growth looks to accelerate from here based on its backlog, which is now $460 billion. This chart is almost impossible to believe:

Google Cloud is also highly profitable, with operating profit coming in at a record $6.6 billion – triple last year’s level.

Alphabet’s total costs and expenses grew 18%, slightly slower than revenues. That caused operating margins to expand from an already high 34% to 36%.

Earnings per share (“EPS”) came in at $5.11, up a mind-blowing 82% YOY and obliterating estimates of $2.63.

With trailing-12-month (“TTM”) revenue of more than $400 billion, it’s astounding that a company of this size can keep growing so quickly and profitably.

And its stock surged as much as 10% this morning.

At the same time, Alphabet continues to spend massively on the cloud and artificial intelligence (“AI”)…

Last year, it had $91 billion in capital expenditures (“capex”). And it plans to double that figure in 2026 to between $180 billion and $190 billion – up $5 billion from prior estimates.

In yesterday’s earnings report, the company disclosed that 2027 capex would significantly increase from 2026. This would be roughly all the operating cash flow the company will generate. (TTM operating cash flow is growing rapidly – it was up 27% YOY last quarter.)

Alphabet’s capex spending is breathtakingly huge, but I believe it will pay off. CEO Sundar Pichai noted that AI is “lighting up every part of the business.”

Frankly, I have no idea what the right capex number is for the company. But as I’ve written many times, I think management is smart to spend however much it takes to win the AI race. Established companies like Alphabet, Meta, Amazon, and Microsoft (MSFT) can leverage AI to grow their dominant businesses (unlike OpenAI, for instance), as I discussed in my February 11 e-mail.

Finally, let’s look at Alphabet’s current valuation…

The stock was trading around $368 a share early this morning, and its 2026 EPS estimate is $14.12 (the $11.64 estimate coming into earnings, plus the $2.48 beat). That would give it a forward price-to-earnings (P/E) multiple of about 26 times.

That’s higher than it has been in a while, thanks to the huge run up over the past year. (Last May, it was trading at around a mere 16 times earnings.) But it’s still only a modest premium to the S&P 500’s current forward multiple of roughly 22 times.

My view today is still the same as it has been for more than seven years: Alphabet is a great stock for conservative, long-term-oriented investors.

META: An All-time Great Business Growing Like a Weed

I’ve consistently been bullish on Meta for the past seven years as well…

Like Alphabet, the company reported great numbers. (You can see the earnings release here and slide presentation here.)

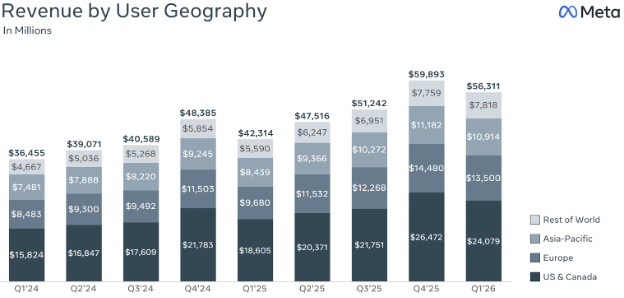

Revenue grew 33% YOY, its biggest quarterly revenue jump in nearly five years. As you can see in the chart below, revenue growth has been excellent over the past two years:

The number of “family daily active people” grew 4% YOY. But this figure declined slightly from last quarter, which management says was due to Internet disruptions in Iran and a restriction on access to WhatsApp in Russia.

Meta’s family of apps (Facebook, Instagram, etc.) now has 3.56 billion daily active users.

“Ad impressions delivered” to these users grew 19%, a nice jump from 14% and 18% in the past two quarters. Meta was able to charge a 12% higher average price per ad than the same period last year. These are strong figures.

Costs and expenses rose 35%, roughly in line with revenue growth, so operating margin remained flat at 41%. Meanwhile, operating income grew 30%.

EPS was $7.31 (adjusting for a one-time tax gain), which beat estimates of $6.82.

Similar to Alphabet, these are stellar earnings overall. So why was the stock down as much as 10% this morning?

In part, it was due to disappointment that Meta’s revenue and earnings guidance for next quarter was only in line with expectations.

But mainly, it was because the company increased its projected capex for the year by $10 billion – to a new range of $125 billion to $145 billion, roughly double last year’s $70 billion.

CEO Mark Zuckerberg said the higher estimate is due to a spike in the cost of memory chips, which are in high demand at the moment. But he defended Meta’s soaring capex:

Every sign that we’re seeing in our own work and across the industry gives us confidence in this investment. That said, we are very focused on increasing the efficiency of our investments.

Finally, let’s look at Meta’s current valuation…

The stock was trading around $603 a share early this morning, and its 2026 EPS estimate is $30.13 (the $29.64 estimate coming into earnings, plus the $0.49 beat). That would give it a forward P/E multiple of 20 times.

That means it’s trading below the multiple of the average large U.S. business. This makes no sense for one of the greatest businesses of all time that’s growing like a weed.

If you aren’t a subscriber, you can become one – and gain access to our specific “buy up to” price for the stock and recommended way to protect your capital, as well as our full portfolio of other open recommendations

Recent Articles

KKR, Blackstone, and Brookfield Bet $16 Billion on Kuwait’s Oil Pipeline Deal

Bloom Energy’s Recent Mega Sell-Off Could Be a Buying Opportunity After a Blowout Earnings Report