Listen to the audio version of this article (generated by AI).

I’m keeping a bit of wisdom from my mentor Warren Buffett in mind as I take a closer look at the financials and valuation of the streaming giant Netflix (NFLX)…

“It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price…” Buffett wrote in his 1989 annual letter to Berkshire Hathaway shareholders. “[W]hen buying companies or common stocks, we look for first-class businesses accompanied by first-class managements.”

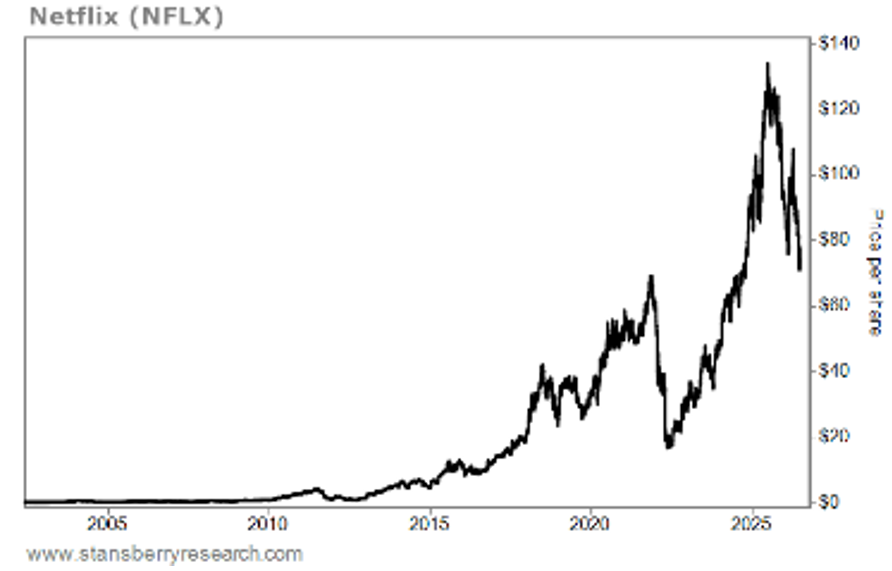

In my June 23 e-mail, I described Netflix as exactly that: “another fantastic company whose stock has pulled back quite a bit.”

The stock is up 5% since then, but it’s still down more than 40% from its June 2025 high of $133.91 a share:

So let’s dig in to see if Netflix remains a “wonderful company” and whether it’s hit a “fair price.” (And for a surprising bearish call on Netflix, check out this deep dive article into Marc Chaikin’s latest prediction… His Power Gauge has liked Netflix for years – including up to a 4X gain for investors – but it now ranks Netflix as Very Bearish. Learn why and get several free “sell this, buy that” recommendations by clicking here.)

Netflix Built a Cash-Generating Juggernaut

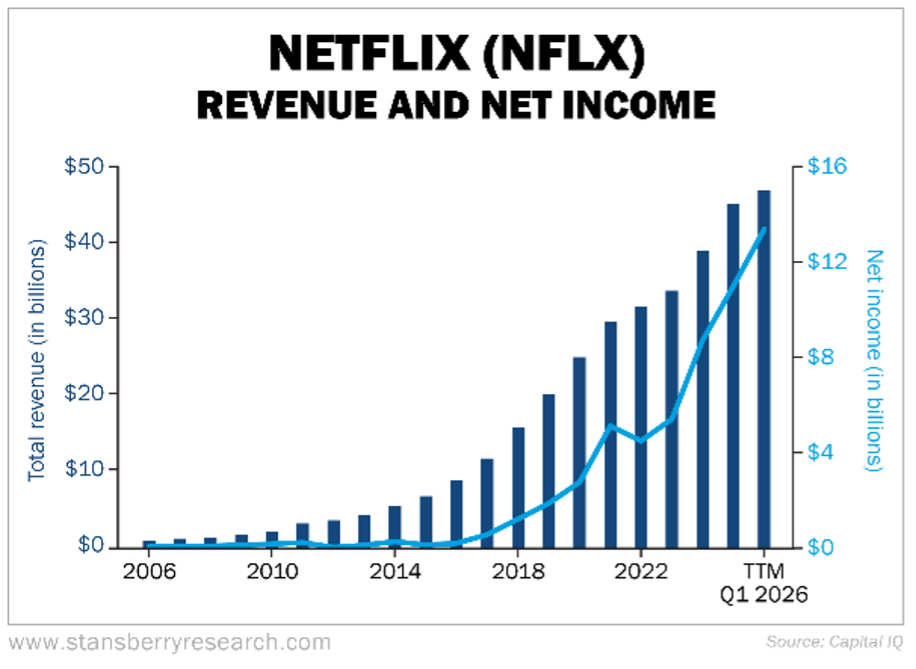

Netflix has been one of the greatest growth stories of all time. Revenue and net income have risen 47 times and 274 times, respectively, in the past two decades. And they show no signs of a slowdown:

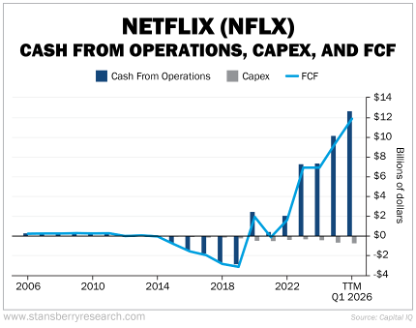

The company had five years of negative free cash flow (“FCF”) in the mid-2010s to fund international expansion and the growth of its content library – both highly successful ventures. Since then, FCF has exploded:

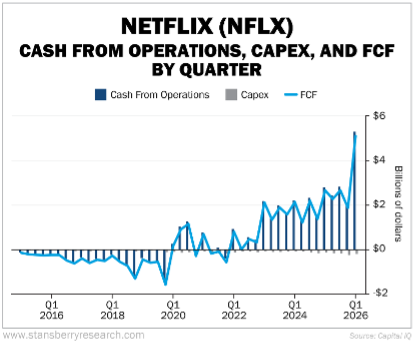

Whenever I see a stock that has fallen a lot, I want to see if its financials reveal any sign of weakening in recent quarters. That’s not the case with Netflix. It reported its highest FCF ever in the first quarter:

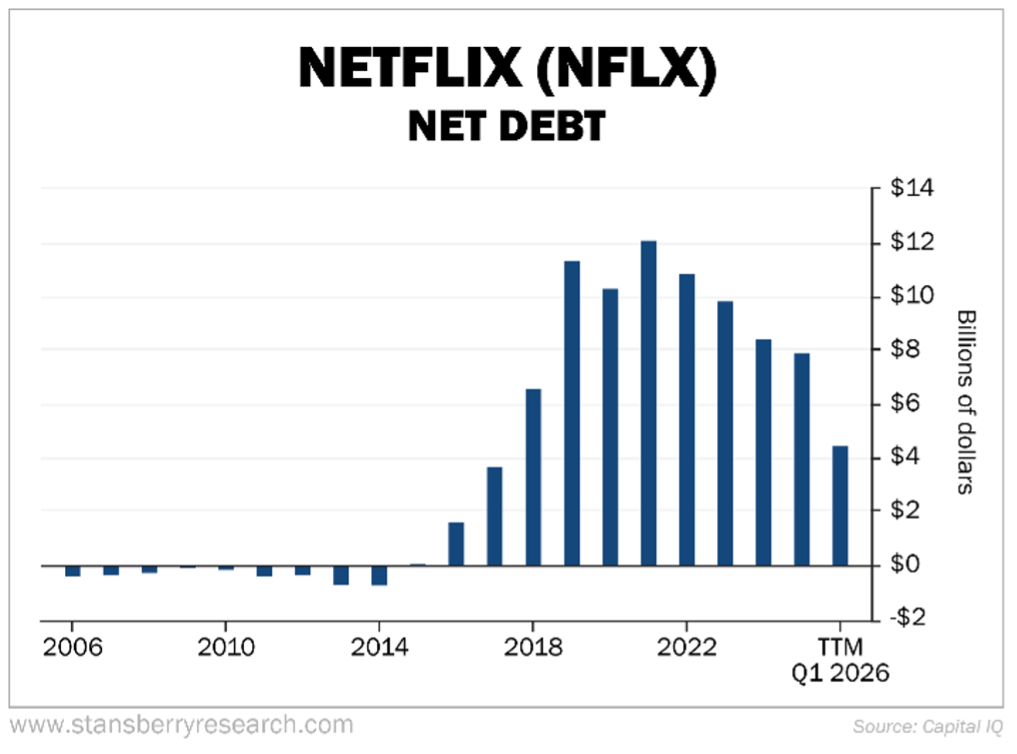

Netflix has used its FCF to pay down debt and buy back shares. Net debt is down from around $12 billion in 2021 to $4.5 billion today. That’s a fraction of the $11.9 billion of FCF the company generated in the past year:

It has also ramped up share repurchases since it started generating substantial FCF. As a result, the company’s diluted shares outstanding have started to decline, albeit only by 1.6% in the past year.

This is an A+ financial picture. Netflix continues to grow rapidly, FCF is soaring, and its balance sheet is strong.

Netflix Shares Cheap Despite A+ Financials

Turning to valuation, here’s what I wrote in June:

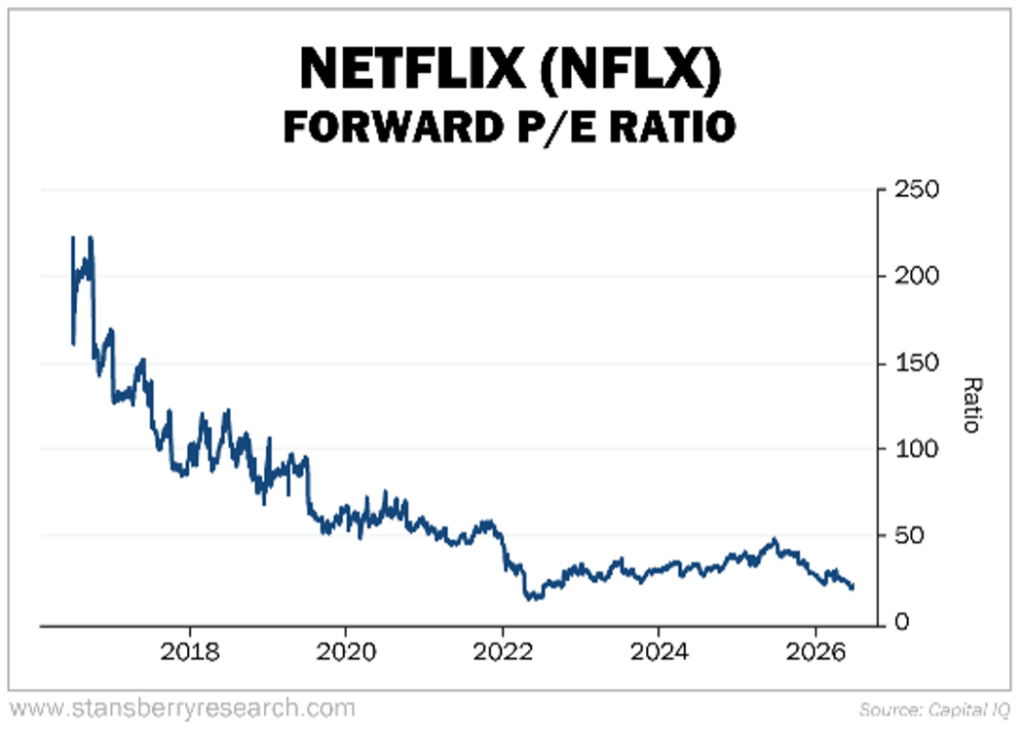

[Its] valuation got ahead of itself. A year ago, it was trading at more than 50 times forward earnings. Today, with the stock down and earnings up, it trades at only 20.3 times this year’s estimates – a below-market multiple for a far-above-market-quality business.

The stock is up a bit since then, closing at $77.65 a share on Thursday. And consensus estimates for this year are $3.59 in earnings per share. That means the stock is currently trading at 21.6 times this year’s estimates – slightly below the average for the S&P 500 Index.

In addition, it’s trading far below its average forward price-to-earnings (P/E) multiple of 65.1 times over the past decade, as you can see in this chart:

Netflix’s stock is interesting at these levels. The company reports second-quarter earnings in 10 days, which my team and I will be reviewing carefully.

Could NFLX Return to Recent Highs?

A few months ago, someone posting under the handle “ThinkAnew” pitched Netflix on the Value Investors Club website. Since the site is only open to members, I’d like to share a few excerpts…

First, ThinkAnew highlights the virtuous cycle Netflix has created:

[F]rom DVDs-by-mail to streaming, their strategy has always been distribution first, content second. Once you have built up the silky-smooth tech, the back-end-infrastructure, the brand name, and became the de-facto #1 in streaming and cornered the distribution channel that consumers get and discover content (with low churn), it becomes very hard for anyone else to uproot you. And each new customer means almost pure profits and even more revenue to re-invest in better tech…

And once Netflix became the dominant distributor and its algorithms [could] determine what you watch, they have so much power that suppliers (the actual content makers) flocked to them… [So then Netflix had] lower per unit content costs, suppliers willing to forgo more money for the opportunity to be on Netflix, etc… and they dominated the value chain. And consumers get a great service that is still arguably cheaper and better than what they can get elsewhere. And it becomes harder to cancel Netflix because they have the content budget to put something worth watching in a more rapid cadence than anyone else.

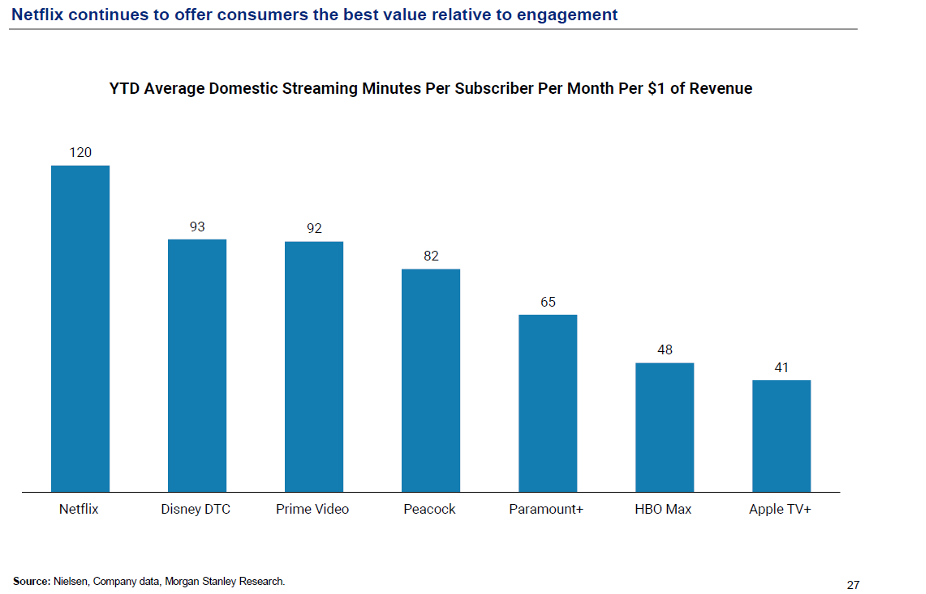

ThinkAnew shares a chart from Morgan Stanley Research showing that Netflix offers the best value of any streaming service, as measured by how many minutes per month the average subscriber watches per dollar paid in subscription fees:

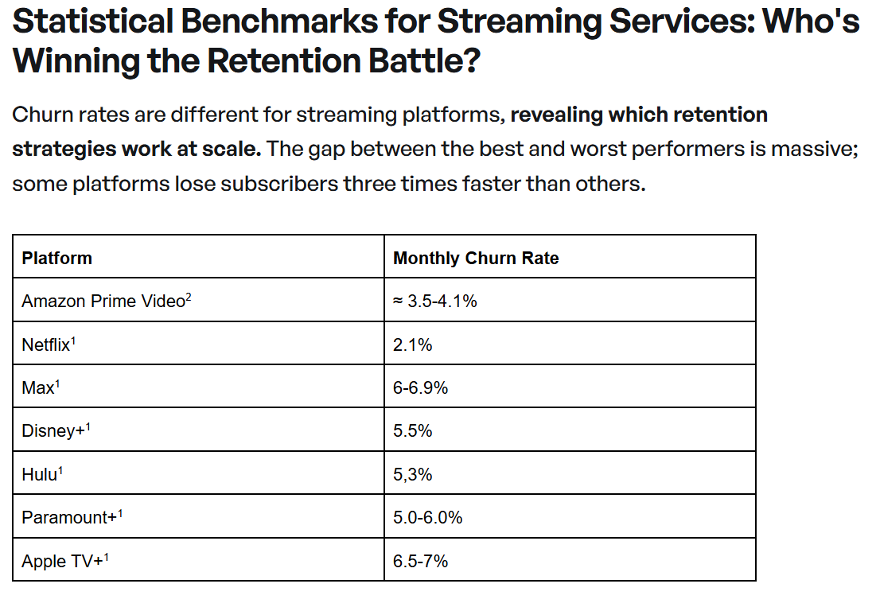

ThinkAnew also notes that Netflix’s monthly customer churn rate is far lower than its peers, according to this chart from Churnkey.co:

ThinkAnew shows the financial implications of Netflix’s virtuous cycle:

This is the result when you have over 325M paid memberships and one billion people globally using your service. The same $20B of annual content cost just costs a lot less per customer and you can pass on the unit cost efficiencies to each of them. Again, scale wins.

And dominance clearly shows up [in] the numbers. Between 2018 and 2025, content cost as [a percentage] of revenue went from 48% to 36% and sales & marketing from 15% to 7%. And they can spend 3x the amount in research and development and general & administrative expenses over the years and EBIT [earnings before interest and taxes] went from 10% to 29.5%. ROIC [return on invested capital] is a mouth-watering 28%…

This is not core to the thesis, but advertising revenue grew 2.5x in 2025 and they think it’ll double again in 2026 to $3B. Not insignificant for a $52B revenue (2026) and presumably most drops to bottom line.

Netflix’s huge audience gives the company the ability to create value for its content. ThinkAnew points to the influence of its Drive to Survive series about the Formula 1 auto racing circuit…

Who in the U.S. (except the hardcore fans) knew about F1 before Drive to Survive? Broadcast rights that were given for free by Liberty Media in 2018 suddenly were suddenly worth $150M a year when Apple signed it last year. Who created the value? Netflix!

The writer also notes that AI “in theory” could generate a flood of new content for other platforms that could dilute the attention Netflix commands. But Netflix is just as likely to leverage that flood of content: “[When content producers] create the next big thing… where would they put their content? Netflix!”

Netflix’s is forecasting 2026 revenue of $50.7 billion to $51.7 billion, a 12%-14% year over year growth. And it projects 2026 operating margin of 31.5%, up from 29.5% in 2025.

“Basically, it means incremental EBIT margin of 45-47% (even with acquisition-related expenses; stripping them out, incremental EBIT margin is 50%),” ThinkAnew writes.

The writer concludes by calculating Netflix’s valuation:

When I plug in the numbers, and assume a 14% topline growth that declines to ~13% in 2030 (there’s still quite a bit of international penetration to go after and each additional subscriber is highly profitable), and 45% incremental EBIT margins (you can easily argue this should be higher over time), I get to ~$31.8B EBIT. 17x forward [enterprise value (“EV”)]/EBIT for dominance and EBIT that’s still growing 16-17% is not outrageous.

This means $542B of EV in 2029, and I give them $47B in cash generation credit between 2026 and 2028 (assume 80% EBIT converts to real cash) and take out the $8B in debt, that means equity value by 2029 of $581B and about $134/share in a no-buyback scenario.

I think these numbers are reasonable…

With the stock trading for around $76 a share, ThinkAnew’s $134-a-share target in 2029 would be a gain of roughly 76%. That’s 21% compounded annually over the next three years.

Netflix’s stock is extremely interesting at these levels. The company reports second-quarter earnings next week on July 16, which my team and I will be reviewing carefully.

Editor’s Note: This article was adapted from today’s edition of Whitney Tilson’s Daily. Every day, Whitney emails his readers with his comments on the most important topics of the day, including stocks he’s investigating… great articles he has read… his media and podcast appearances. You can sign up here to receive all of Whitney’s daily thoughts and insights.

Recent Articles

AMD vs. Nvidia: What AMD’s Major $5 Billion AI-Chip Deal With Anthropic Means for Investors

Nvidia Is Becoming the ‘Central Bank of AI,’ As It Weighs $250 Billion OpenAI Data-Center Backstop