Over the weekend, I attended the Berkshire Hathaway (BRK-B) annual meeting in Omaha, Nebraska for the 27th time…

I had a great time speaking at two events, running the 5K race, meeting new people, and connecting with old friends.

The arena for the meeting was full. Attendance was down only 20% compared with last year – better than I expected.

The meeting itself was… sort of boring. (You can watch it in full on YouTube here.)

In the past, when Warren Buffett and the late Charlie Munger held the stage, shareholders paid attention, waiting for one of Charlie’s zingers or a pearl of wisdom about business or life.

CEO Greg Abel and the other Berkshire executives who spoke this weekend offered no such catnip. Their answers were so long-winded that shareholders were only able to ask roughly half the number of questions compared with previous years.

But that’s OK. Shareholders don’t need Abel to be charismatic or dispense folksy wisdom. They need him to do two things well: manage the business and allocate capital.

Based on what I heard on Saturday – and my confidence in Buffett getting the most important decision of his career right (appointing Abel as CEO) – I share Buffett’s optimism that Abel is up to the job.

And as I’ll explain… Berkshire’s stock represents a great value right now.

Berkshire Hathaway’s Results Reveal Abel’s Strong Start

At the beginning of the meeting, Buffett commented, “Greg is doing everything I did and then some, and he’s doing it better in all cases. He’s the right person.” (Here’s the clip on YouTube.)

Buffett also introduced and thanked Apple (AAPL) CEO Tim Cook, who recently announced that he’ll be stepping down at the end of August after an extraordinary 15-year run. During his time as CEO, Apple’s market capitalization increased from $350 billion to today’s $4.1 trillion. He trails only Nvidia (NVDA) CEO Jensen Huang in record value creation.

I think the analogy between Apple in 2011 and Berkshire today is apt. In both cases, boring, nut-and-bolts operators took over exceptionally strong businesses from visionary, legendary founders with a cult-like following. I think there’s a good chance that Berkshire under Abel’s leadership will also do well.

At the meeting, Abel shared his focus on maintaining Berkshire’s unique and powerful culture and achieving operational excellence. He wasn’t shy about recognizing where Berkshire needs improvement. And he clearly understands that capital allocation will be a key driver of value creation.

Here are several video clips on YouTube of his important comments:

And here’s a 15-minute interview CNBC’s Becky Quick did with him, discussing Berkshire’s risk-management legacy, stock portfolio, and more.

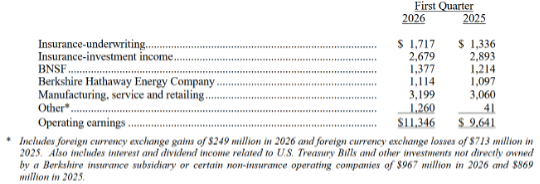

Abel is off to a good start based on Berkshire’s first-quarter earnings, reported on Saturday (press release here and 10-Q here).

I turn to my friend and former colleague, Glenn Tongue, for his thoughts as well. The CEO succession has been “business as usual” at the company. By all accounts, Berkshire enjoyed a strong quarter:

Glenn continued:

Headlines proclaimed that operating earnings grew 17.7% year over year. This is somewhat misleading as the foreign currency headwind a year ago (a $713 million loss) was a tailwind in the most recent quarter (a $249 million gain). Adjusting for this, operating earnings still grew a solid 7.2%.

Regarding insurance results, Glenn said they require a little more analysis:

Digging into the 10-Q shows that Geico’s decline in year-over-year earnings resulted from a $338 million increase in marketing spend, which should pay off in accelerating growth.

While the remaining insurance businesses had strong results, the insurance market has been softening, so maintaining the current level of underwriting and profitability will be challenging.

As for share repurchases, Glenn noted:

As I predicted last quarter, there were finally some share repurchases after many quarters of inactivity. The company bought back $235 million of stock at an average price of approximately $487 per B share. This is a small amount, and there were no additional buybacks in April. I would guess the company will buy more shares this quarter if the stock remains at current levels.

He also analyzed Berkshire’s stock buys and sells:

Another big capital allocation lever is the sale and purchase of various stocks. The company bought $15.9 billion in equities and sold $24.1 billion. This is a huge increase in activity.

In the same quarter last year, Berkshire only bought $3.2 billion and sold $4.7 billion. But the direction remained the same: This was the 14th consecutive quarter in which Berkshire was a net seller.

Lastly, he commented on Berkshire’s record cash hoard:

The combination of $5.5 billion of free cash flow and $8.1 billion of net stock sales, partially offset by $9.7 billion spent on acquisitions and $235 million of share repurchases, led cash to rise to a record level of $380.2 billion. This is a staggering number – larger than the entire market caps of all but 30 companies in the world and equal to 37% of Berkshire’s market cap.

With stocks at all-time highs, this “dry powder” (a phrase Abel used in Berkshire’s annual letter) should be a strategic asset in this ever volatile world.

Berkshire’s Stock Lagged the Market Last Year – as Expected

Today, I’ll take a look at the stock and update my estimate of Berkshire’s intrinsic value…

I’ve long called Berkshire “America’s No. 1 legacy stock”… But it has been a stinker over the past year. It has underperformed the S&P 500 Index by 40 percentage points since Warren Buffett announced he’d be stepping down at last year’s annual meeting.

The stock closed at an all-time high of $809,350 per A-share on the day before the May 3, 2025, meeting. Since then, Berkshire is down 13.2%. Meanwhile, the S&P 500 is up 26.6%:

I’m not surprised by this outcome. I was bullish on the market back then, and I saw that Berkshire, which had doubled over the previous two and a half years, had gotten ahead of itself.

In my May 7 e-mail last year, I calculated that the stock’s intrinsic value was only $743,000 per A-share, meaning it was 8.9% overvalued at its peak.

But today, the situation has reversed – making the stock look attractive now…

Berkshire Will Be a Market Beater Over the Next Five Years

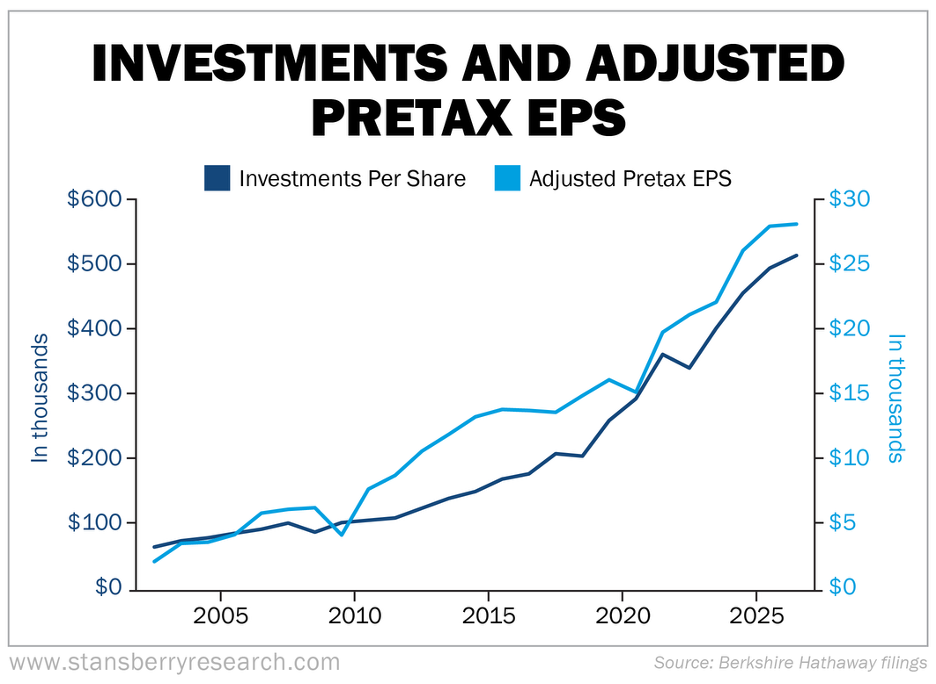

As longtime readers know, to calculate my estimate of intrinsic value, I take Berkshire’s cash and investments per share and add the value of the operating businesses. (I believe Warren Buffett has long used a similar method.)

At the end of the first quarter, cash and investments totaled $503,000 per A-share. Thanks to the market’s strong performance since then, Berkshire’s stock portfolio has gained roughly $10,000 per share. That brings the total to around $513,000.

Next, here’s how I calculate Berkshire’s pretax operating earnings for the quarter…

First, I take the trailing-12-month operating earnings of $52.5 billion. Then I adjust for normalized earnings from Berkshire’s insurance segment. That means subtracting $25 billion of profits from insurance underwriting and investments. Next I add back half of the average over the past two years, which is $13 billion. (I think this is conservative, given that insurance and investment income has averaged $11.5 billion per year over the past decade, and Berkshire is much bigger now.)

The result is adjusted pretax earnings of $40.5 billion, equal to $28,131 per A-share.

Investments and earnings per share (“EPS”) are the two components of Berkshire’s value, which you can see in the chart below. While there have been occasional dips, this is an extraordinary record of consistent growth:

A conservative, below-market multiple on Berkshire’s earnings is 11 times. So at $28,131 in EPS, that equals $309,000 per A-share.

Putting it all together, we add cash and investments of $513,000 to the value of Berkshire’s operating businesses of $309,000. This totals $822,000 per A-share and $548 per B-share.

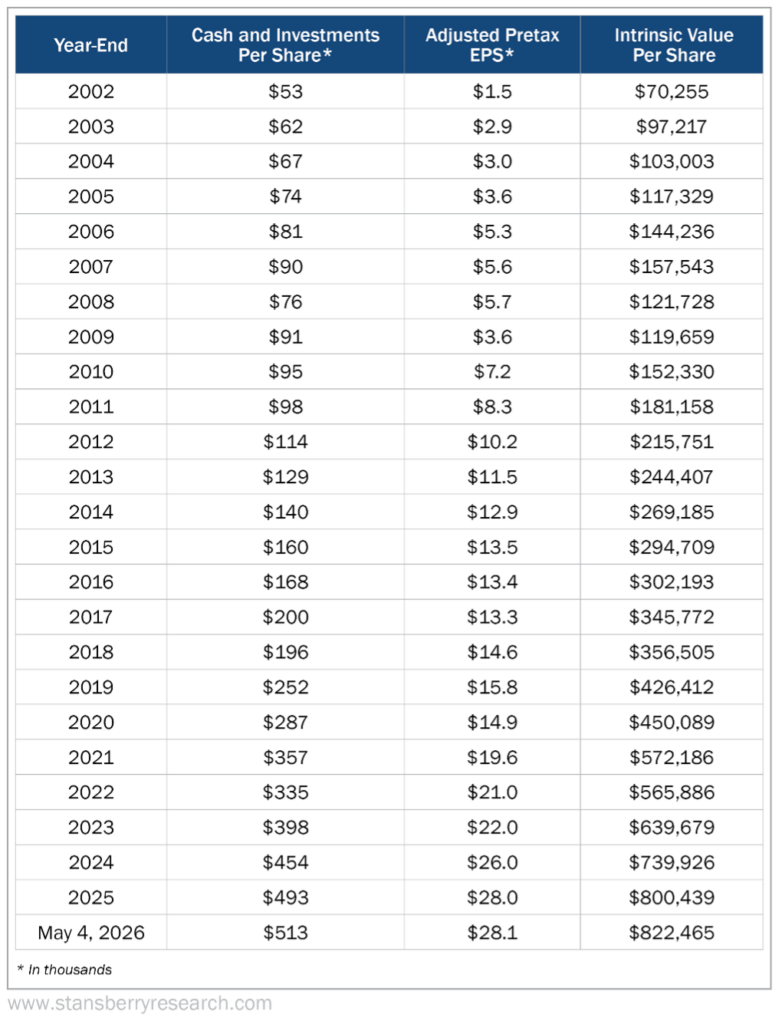

Here’s a table showing this calculation going back to 2002:

Yesterday, Berkshire closed at $702,790 per A-share. That means the stock is trading at a 14.6% discount to my estimate of intrinsic value.

So, in the past year, Berkshire has swung from being 8.9% overvalued to 14.6% undervalued. That’s why it wasn’t attractive then – but is today.

I’m especially bullish because in addition to today’s discounted stock price, I’m optimistic that Abel can create value via operational improvements and capital allocation.

This combination leads me to believe that Berkshire’s stock is highly likely to beat the S&P 500 over the next five years, perhaps by a margin of two to three percentage points. So if the S&P 500 compounds at 5%, I would expect Berkshire to do roughly 7% to 8% – with a bias toward the upside.

My Stansberry’s Investment Advisory team and I recommended buying Berkshire’s B-shares in late 2023, when they were trading at a 14% discount to intrinsic value. Subscribers who followed our advice since then are up 32%.

If you aren’t a subscriber yet, you can find out how to become one right here.