Whether you like it or not, you’ll be using cryptocurrencies sooner than you think.

In fact, you may already be using them… without even realizing it.

See, crypto is getting integrated into the financial system, but a lot of its adoption is happening quietly in the background. So it remains unnoticed by the general public.

For example, last December, Visa (V) expanded its stablecoin settlement program so that certain transactions with banking partners can be settled in USD Coin (USDC) – a stablecoin that represents real U.S. dollars. This allows settlements to happen 24/7, almost instantaneously – even on weekends and holidays.

Rubail Birwadker, global head of Growth Products and Strategic Partnerships at Visa, had this to say about the launch…

Visa is expanding stablecoin settlement because our banking partners are not only asking about it – they’re preparing to use it… Financial institutions are looking for faster, programmable settlement options that integrate seamlessly with their existing treasury operations. By bringing USDC settlement to the U.S., Visa is delivering a reliable, bank‑ready capability that improves treasury efficiency while maintaining the security, compliance and resiliency standards our network requires.

Banks and institutions are demanding this infrastructure. It’s making transactions easier, faster, and more secure. So it’s a hard technology for institutions to ignore.

It’s no longer a question of if they’ll adopt it… but when.

So more of your transactions will likely be settled on blockchain rails behind the scenes, whether you know about it or not.

But it’s not bitcoin (BTC) being adopted for this purpose. It’s blockchains like Ethereum (ETH), Hedera (HBAR), and many more that are offering the rails for meaningful institutional adoption.

That’s why it feels like crypto is dying… because bitcoin is still crypto’s poster child. It accounts for more than half of the crypto industry’s entire market cap.

And that means when bitcoin falls, everything will fall.

Bitcoin’s Sell-Off

According to Michael Burry, the Big Short investor best known for predicting the 2008 housing crash, a bitcoin “death spiral” could be just around the corner.

Bitcoin – the largest crypto by market cap – is down 47% from its all-time high of $126,080 in 2025. And it’s down 25% since the beginning of 2026.

This recent crash is due to a variety of factors. But the crypto’s initial break from its highs is largely due to President Donald Trump’s October 2025 announcement of a 100% tariff on Chinese imports… which escalated U.S.-China trade tensions.

This was a clear risk-off signal for investors. And it led to an expected correction in riskier markets like crypto. But overleveraged positions turned that small dip into an avalanche…

In short, many investors were borrowing extra money from exchanges to buy even more bitcoin – what’s called “leverage.” When prices rise, that extra BTC lets them amplify their gains and pay back the loan. So they make a lot more money than if they’d just bought with their own cash and waited for prices to rise.

But as bitcoin prices dropped, exchanges automatically liquidated investors’ leveraged BTC positions to make sure those loans were repaid. That forced selling pushed the price of bitcoin down even further, which triggered more liquidations, and so on. By late November, bitcoin had fallen around 33%.

This is a known mechanic that can cause big crypto sell-offs.

Everyone starts dumping their bitcoin, but not because they want to. Many overleveraged positions got liquidated, and some investors started redistributing their portfolios to lessen their exposure to riskier assets like bitcoin. So the market looks like it’s going into a death spiral.

And there was a lot of BTC to offload… because preceding that drop was one of the biggest run-ups in crypto history. From October 2024 to October 2025, bitcoin roughly doubled in value. Hype was at an all-time high… with new regulatory clarity fueling the flames of institutional adoption.

For example, in July 2025, the Guiding and Establishing National Innovation for U.S. Stablecoins (“GENIUS”) Act was signed. It became the first comprehensive federal digital-asset law in the U.S. and gave payment stablecoins a clear licensing and supervision framework.

It’s this kind of regulatory certainty that allows big institutions like Visa to meaningfully onboard crypto technology like blockchain to streamline their operations.

Blockchains offer near-instant settlements, cheap fees, and high-security smart contract technology that can help make processes easier and reduce friction.

It’s an enticing idea for many institutions stuck with slow transaction layers and risky, centralized data points.

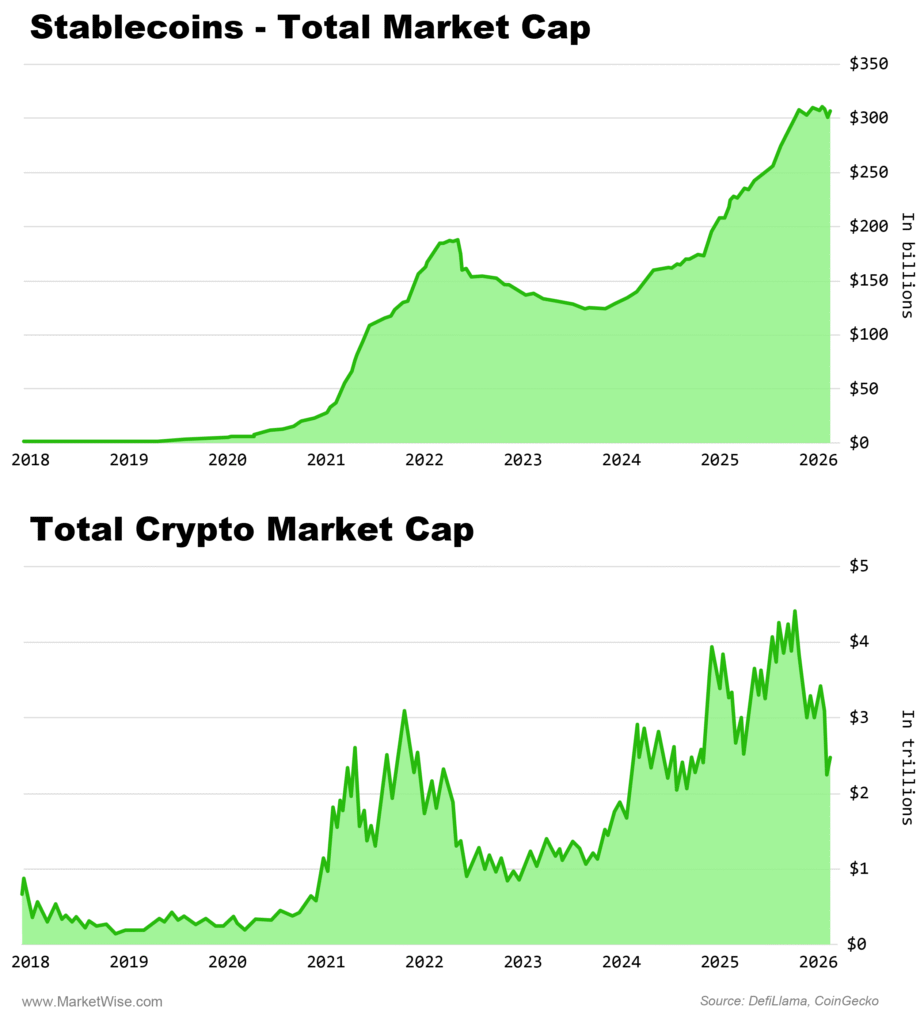

That’s why stablecoins’ total market cap has been steadily rising, even while crypto plummets…

Here’s the thing to pay attention to…

That recent regulatory news is still relevant.

It takes time to put this sort of adoption into effect at a national scale. It takes hiring crypto advisors, building teams, understanding frameworks, and cross-company cooperation to create that sort of infrastructure.

Developers are currently working with their heads down, ignoring the market doom and gloom, and finally putting blockchain’s promise of cheap, decentralized infrastructure into action.

BlackRock (BLK), Goldman Sachs (GS), Morgan Stanley (MS), and Citigroup (C) are just some of the major traditional-finance institutions expanding their workforce with blockchain engineers and advisors this year.

While headlines are screaming “crypto is dead,” some of the oldest players in traditional finance are preparing for the new age of decentralized finance.

And that’s the type of value that offers more stable, predictable price patterns over time.

The Crypto Revival May Look Very Different This Time

While bitcoin will likely maintain its title as the No. 1 crypto for years to come… with plenty of upside ahead of it… the real bet for crypto infrastructure lies with altcoins.

These are all the cryptos alternative (hence the “alt”) to bitcoin. They come in all shapes and sizes. But the best ones have smart contract technology, decentralized governance, and utility behind their cryptocurrencies.

Altcoins are where we can find the rails that will carry much of our future financial landscape.

Of course, when many people hear “altcoins,” their mind may go to “meme” cryptos like Dogecoin (DOGE)… or non-fungible tokens (“NFTs”) of pictures of apes that once sold for millions of dollars but now are near-worthless.

It’s important to remember that anyone can make cryptocurrencies. So the market is flooded with worthless, story-driven coins that make big promises and don’t deliver.

In 2025, Coinbase Global (COIN) CEO Brian Armstrong stated that 1 million cryptocurrencies are created every week. That’s a lot of noise to comb through.

But like a needle in a haystack, some cryptos really do offer technology that can change the way we interact with the world in meaningful ways. For example…

- Health care: Blockchains can be used to store and share medical records in a way that’s tamper-resistant and interoperable. That means your lab results, prescriptions, and history can be shared securely and privately between hospitals and clinics. So you get the right care when you need it, without repeating tests or losing critical information.

- Real-world assets: Treasurys, bonds, real estate, and private credit can be tokenized and traded 24/7 with lower minimums. That means…

- A small investor can get exposure to institutional-grade assets that used to be “accredited only.”

- Companies can raise capital faster and cheaper by issuing tokenized securities instead of wading through legacy plumbing.

- Supply-chain transparency: Products can be tracked from factory to store shelf on a shared ledger. That helps:

- Prove authenticity (anti-counterfeiting for luxury goods or pharmaceuticals)

- Track food from farm to table so recalls are faster and safer

- Verify environmental, social, and governance (“ESG”) claims (where materials came from, how they were produced)

- Micropayments and creator economies: With traditional rails, charging fractions of a cent per view doesn’t make economic sense. Crypto rails make tiny, automated payments possible:

- Pay-per-article instead of subscription walls

- Machine-to-machine payments (one device paying another for data or bandwidth)

- Streamed payments to creators instead of chunky, delayed payouts

- Disaster and crisis payouts: Aid organizations can use stablecoins to send instant, transparent relief payments directly to recipients’ phones, instead of relying on slow banking systems or intermediaries that take a cut or get blocked.

And that’s just the beginning.

But the truth is that most coins will never touch any of this. They’re like penny stocks with a mascot and a meme attached to them.

Instead, a small set of networks and protocols is quietly wiring up health care, payments, identity, and capital markets behind the scenes. Those are the ones that will rise from the ashes and grow exponentially in the coming onboarding of blockchain technology.

If you want to hear more about which cryptos will take the world by storm, you can read more in Crypto Capital. In this monthly newsletter, my colleague Eric Wade and I research and recommend cryptocurrencies that are set up for massive gains thanks to the real utility they provide.

We look at all kinds of cryptos and run them through our UPDRAFT scoring system that looks at important factors like users and community, decentralization, how easy it is to invest, the team behind each project, and their future plans.

We’ve built out a portfolio full of everything from decentralized music protocols and ticketing services to projects that are tokenizing real-world assets so that almost anyone from around the world can participate in this emerging market.

Good investing,

Stephen Wooldridge II

Editor’s Note: “A strange day is coming to America.”

That’s according to a former Goldman Sachs executive who predicted everything from the 2022 crash, the death of the 60/40 portfolio, and even the rise of blockchain.

He’s not the only one sounding the alarm:

- The Wall Street Journal calls it a ‘New World Order.’

- The Financial Times says, “the unimaginable is becoming imaginable”… and that it could “upend the global monetary system.”

- And one of President Trump’s senior advisers has already laid out the plan to accelerate this trend. It’s all written out, point-by-point, in black and white. (Details here.)

So, what should you do right now to come out ahead?

Click here to learn more in Dr. Eifrig’s new free presentation… and get the three money moves to capture the biggest potential gains as this seismic change unfolds.