It’s official… SpaceX is the most overhyped, overvalued initial public offering in history (for now, at least, until cash-burning Open AI makes its debut)…

Just how foolish is SpaceX’s valuation? In a Substack post yesterday (for paid subscribers), Michael Burry, of The Big Short fame gave some perspective:

At a $2.8 TRILLION market cap, SpaceX, which is fundamentally a small space company, a niche telecom, a bedeviled social media company, and a CoreWeave-light, has less than $20 billion in total revenue.

With that $2.8 trillion, SpaceX’s market cap could buy Page, Brin, Bezos, Zuckerberg, Ellison, Arnault, Huang, Buffett, and Ortega and still have $1 trillion left over. Those are the… richest people in the world, after Elon.

SpaceX’s market cap is now, or a few moments from now, larger than each of Russia, Italy, and Canada.

Berkshire Hathaway has been eclipsed 2 1/2 times over in just three days…

SpaceX’s net worth could buy every single U.S. aerospace and defense company and have money left to buy every gold miner and airline in the world.

Elon Musk himself is now worth more than Berkshire Hathaway.

When SpaceX went public at $135 per share last week, I thought it was roughly 10 times overvalued – not 10%, but 10 times.

I wouldn’t have shorted the stock then – or even now, with it up to around $200. (And in any case, I don’t recommend most investors short stocks.)

That’s because in the short run, stocks like this can trade anywhere. It’s a good reminder of this old saying: “The market can stay irrational longer than you can stay solvent.“

SpaceX’s Stock Looks a Lot Like Cisco and Avis

I’ve heard people justify buying into SpaceX’s IPO by pointing to how well investors did buying into the Amazon (AMZN) and Tesla (TSLA) IPOs.

This is a silly analogy. After the first day of trading, those companies had market caps of $560 million and $2.27 billion, respectively.

SpaceX’s market cap today is approximately 5,000 and 1,200 times greater. At $2.7 trillion, SpaceX is trading at 140 times trailing revenue.

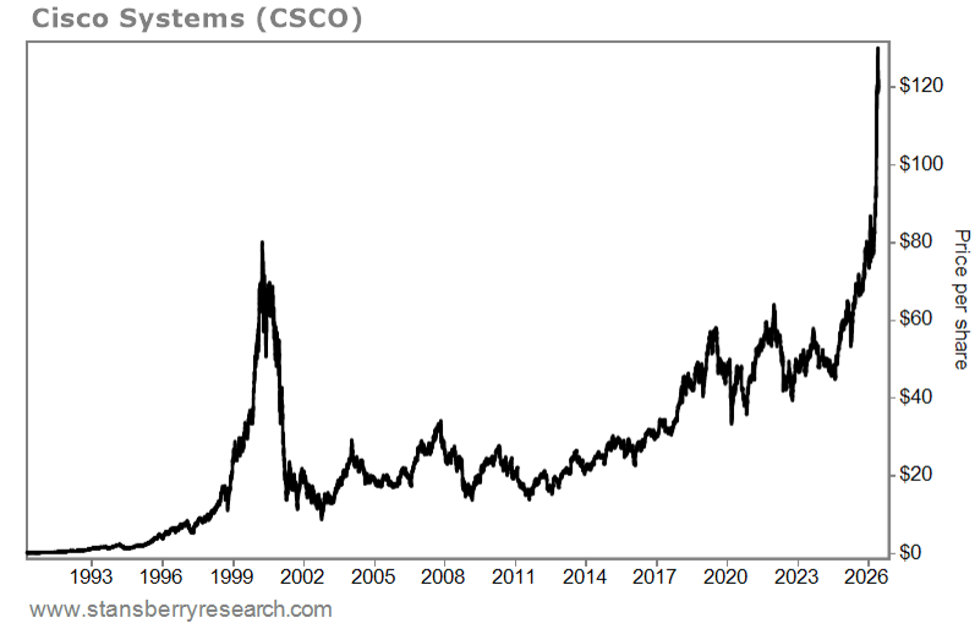

This reminds me of Cisco Systems (CSCO) when it briefly had a $570 billion market cap and traded at 232 times trailing earnings at the peak of the Internet bubble in March 2000…

Cisco’s earnings and revenue continued to grow rapidly in subsequent years. But because of its extreme valuation, the stock fell by 88% and didn’t recover for 25 years, as you can see in this chart:

SpaceX also reminds me of Avis Budget (CAR) earlier this year, when it spiked from around $100 per share to nearly $850 in less than a month – thanks to an epic short squeeze, which I covered on April 17, April 24, and May 7.

In the first, I concluded:

I would guess that we’re very close to the top and that Avis’ stock will soon be back to around $100 per share.

Sure enough, Avis’ stock closed yesterday at $185.49 a share – on its way back to $100, I predict.

The Three Factors Driving SpaceX’s Share Higher

Unlike Avis, I don’t think a short squeeze is what’s driving SpaceX to such absurd levels. Rather, it’s due to three factors…

First, there’s a very limited float – only about 5% of SpaceX’s shares are trading.

Second, I suspect there’s a feedback loop in which investors (in this case, I’d say speculators) are buying SpaceX’s call options. The market makers who sell the options (big banks, mostly) then buy the stock to protect themselves – this is called “delta hedging.”

This buying pushes up the stock, requiring the market makers to buy more stock. That’s because as the stock price moves up through the option’s strike price, it’s more likely the option will be exercised. This cycle can push a stock up and up… which I think is happening with SpaceX.

Lastly, one of the primary beliefs underpinning SpaceX’s valuation is that you can blindly invest with CEO Elon Musk and he’ll make you a lot of money. Exhibit A, of course, is Tesla.

For more than 14 years, this belief may have been true. But not today…

Tesla’s stock rose more than 250 times from its split-adjusted IPO closing price of $1.59 to a peak of $409.97 on November 4, 2021. But Tesla’s extreme valuation and deteriorating fundamentals have weighed on the stock since then…

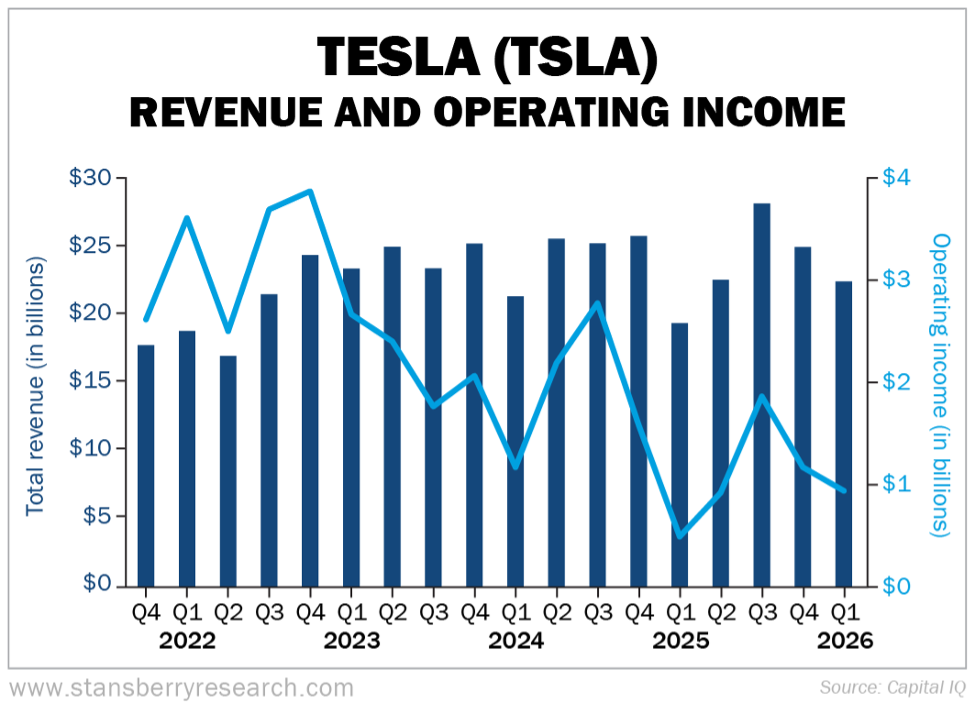

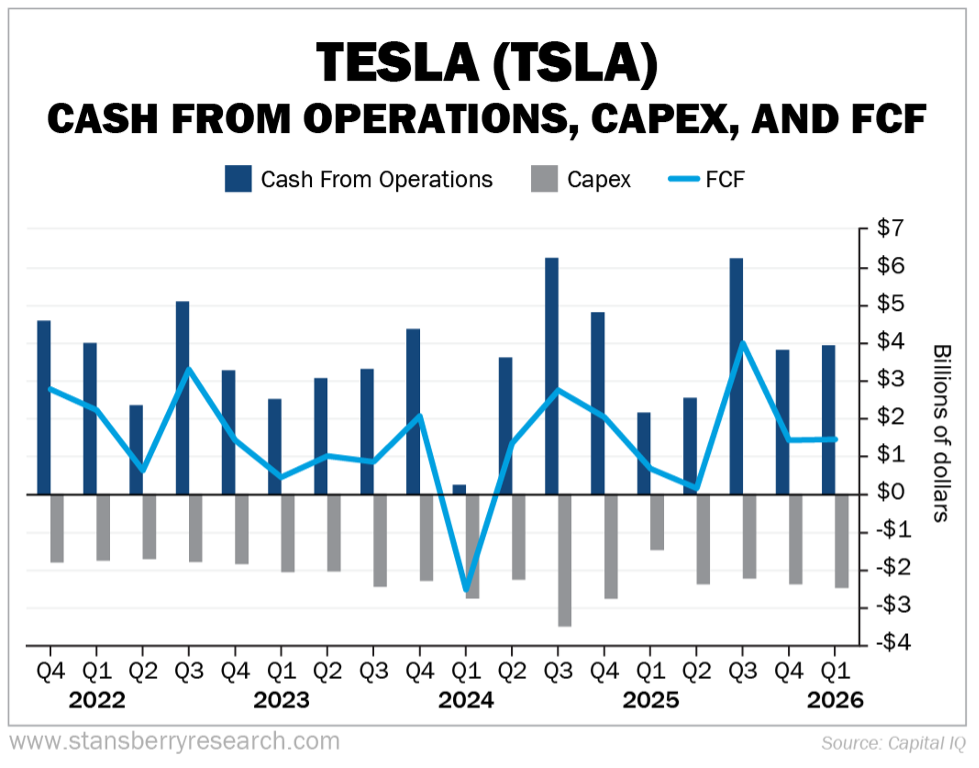

Revenue has stagnated since the fourth quarter of 2021, while profitability has steadily declined. And operating income has crashed by 64%, from its peak of $13.7 billion in 2022 to $4.9 billion over the past four quarters:

Meanwhile, FCF is roughly flat:

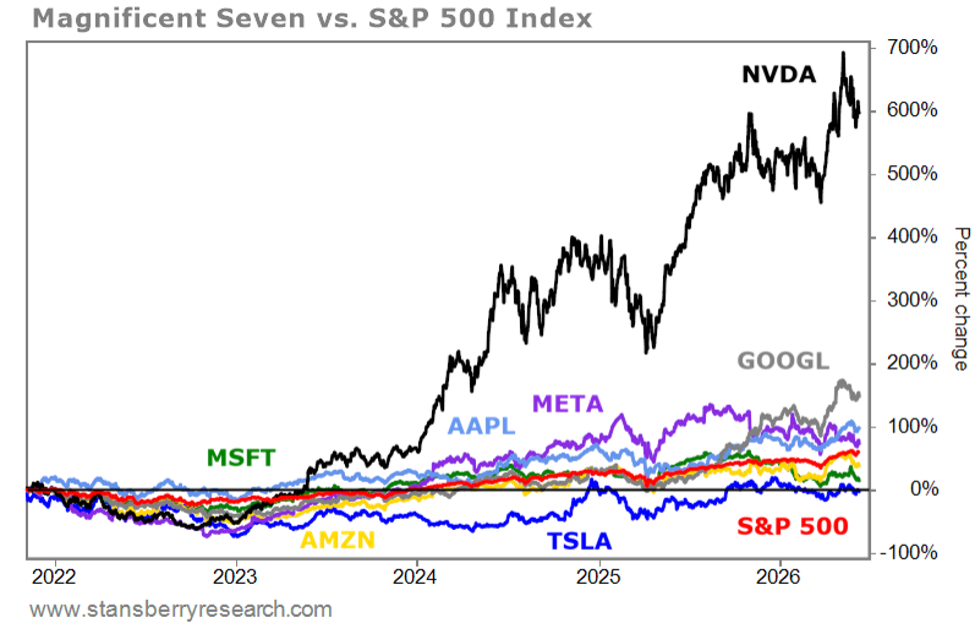

As a result, since November 4, 2021, Tesla’s stock is down 1.3%. That not only badly lags the S&P 500 Index, which is up 60.5% over the same time frame, but also every other stock in the Magnificent Seven:

- Microsoft (MSFT), up 17.1%

- Amazon (AMZN), up 41.5%

- Meta Platforms (META), up 78.7%

- Apple (AAPL), up 98.2%

- Alphabet (GOOGL), up 151.7%

- Nvidia (NVDA), up 596%

You can see the comparative performance in this chart:

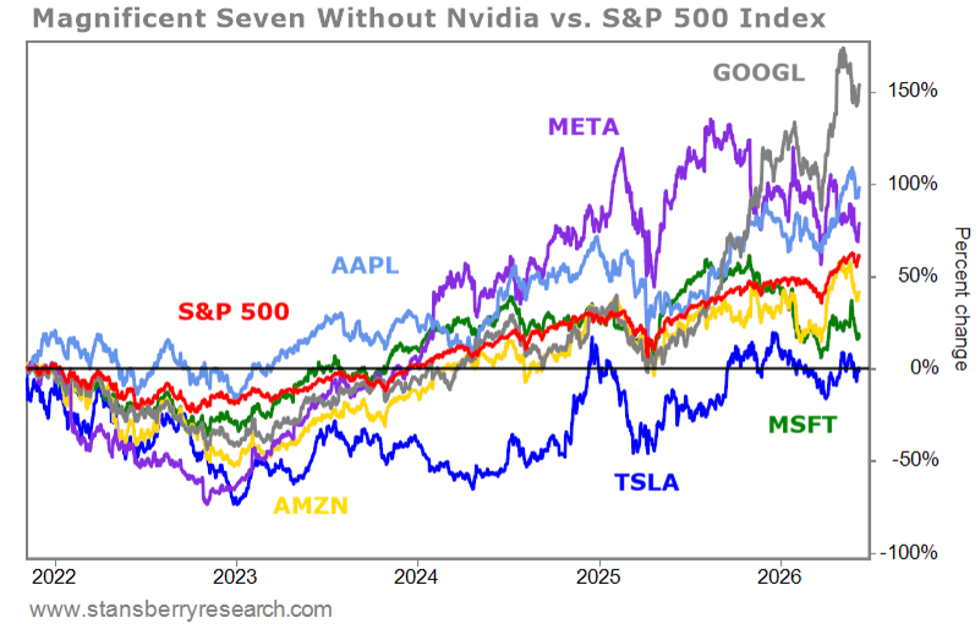

And this chart removes Nvidia so you can better see the other stocks:

Frankly, I’m shocked that Tesla’s stock has held up so well. If it were any other stock, with rational investors instead of Musk worshippers, it would be down by at least 50%.

But instead, the decline in earnings has been offset by a rise in Tesla’s price-to-earnings multiple. At yesterday’s closing price of $404.66, it’s trading at 196 times this year’s consensus analysts’ estimate of $2.06 per share. Go figure…

SpaceX’s valuation absurd… and its IPO has put millions of Americans’ retirement savings in danger – even if you haven’t bought a single share.

That’s because of a new financial rule surrounding the nature of IPOs. When it’s put into place on July 6, it will have dramatic implications for anyone holding index funds, exchanged-traded funds of all kinds, and more.

I’ve just recorded an emergency briefing with one of my most trusted analysts explaining the details of this looming disaster… and one move you need to make to protect your wealth. This is a critical warning I want heard by as many people as possible. I urge you to listen to the full story here.

Recent Articles

AMD vs. Nvidia: What AMD’s Major $5 Billion AI-Chip Deal With Anthropic Means for Investors

Nvidia Is Becoming the ‘Central Bank of AI,’ As It Weighs $250 Billion OpenAI Data-Center Backstop