ServiceNow (NOW) has been one of my favorite software stocks… but lately it has forced me to take a hard look at my bullishness for it.

My team at Stansberry’s Investment Advisory and I recommended the stock seven weeks ago. At the time, it had been nearly cut in half over the preceding year.

Since then, it’s dropped another 25%.

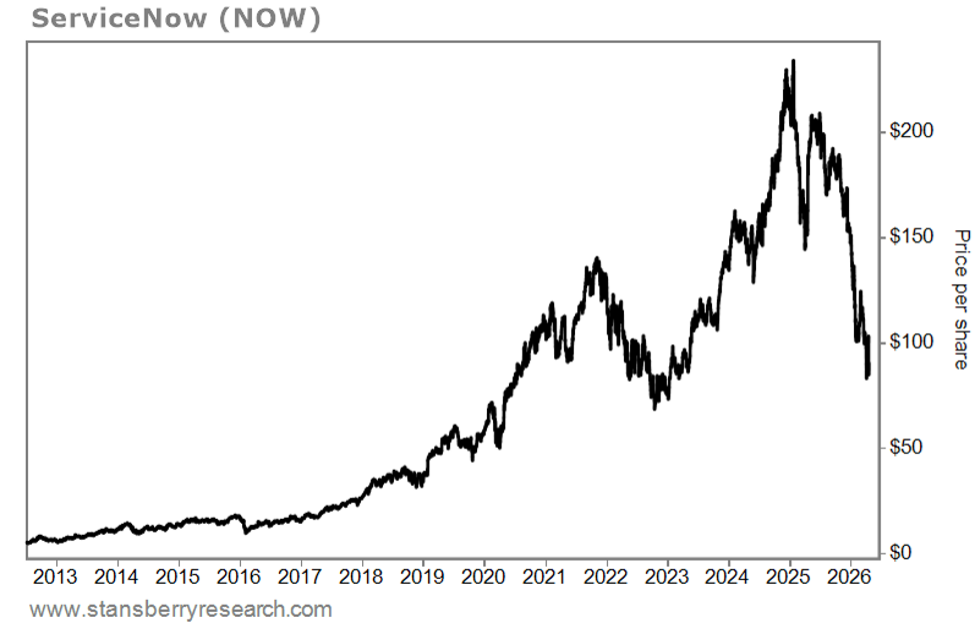

As you can see in the chart below, the stock had been a monster since its 2012 initial public offering. But it has lost 60% of its value in the past 15 months:

Shares tumbled 17.7% on Thursday alone after ServiceNow reported first-quarter earnings (earnings release here and investor presentation here).

Just looking at the stock, you might think that ServiceNow had reported terrible numbers. But that’s not the case…

Revenues and earnings were in line with expectations, and the company raised full-year subscription revenue guidance. Management also said its backlog is strong:

As of March 31, 2026, current remaining performance obligations (“cRPO”), contract revenue that will be recognized as revenue in the next 12 months, was $12.64 billion, representing 22.5% year-over-year growth and 21% in constant currency.

CEO Bill McDermott commented on the company’s strong customer retention, with a 97% renewal rate within the historical range. Demand and high renewal confidence for its Now Platform remains strong. And he continues to expect renewal rates to remain consistently high over time, as they have historically.

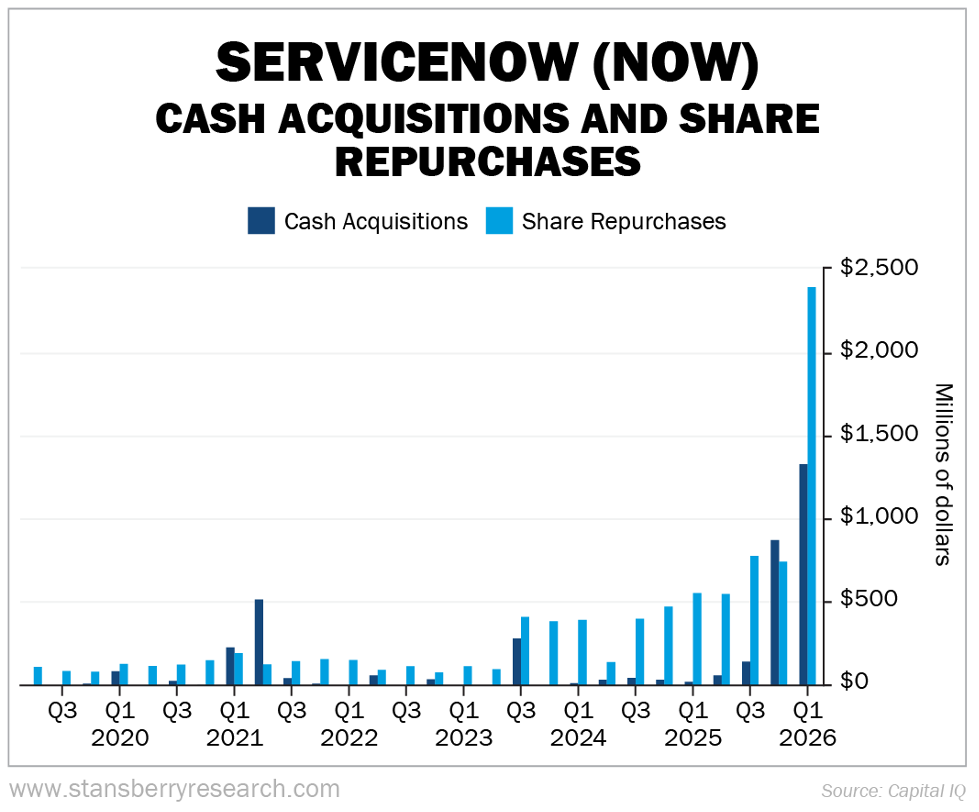

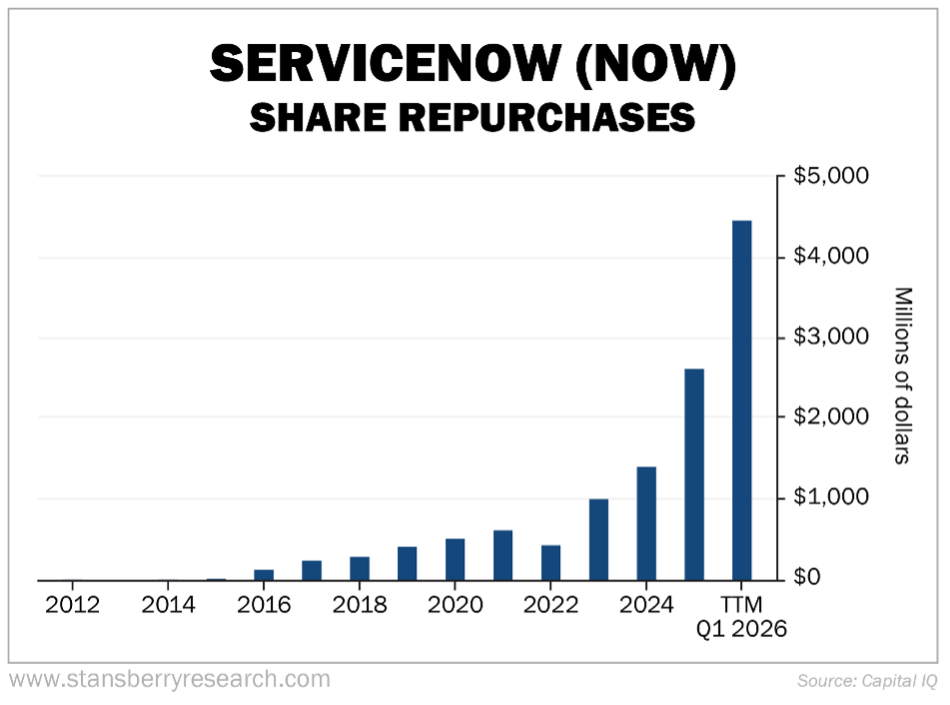

The company also took advantage of its much lower stock price by tripling its share repurchases this quarter relative to the previous two quarters:

This all seems like good news. But when a stock you own falls a lot, it’s important to test your view. Assume the market knows something you don’t and seek out information that challenges your conclusions. Is your investment thesis still intact?

Finally ask yourself: If I didn’t already own this stock, would I buy it today?

So with that in mind, let’s start by looking at ServiceNow’s long-term financials.

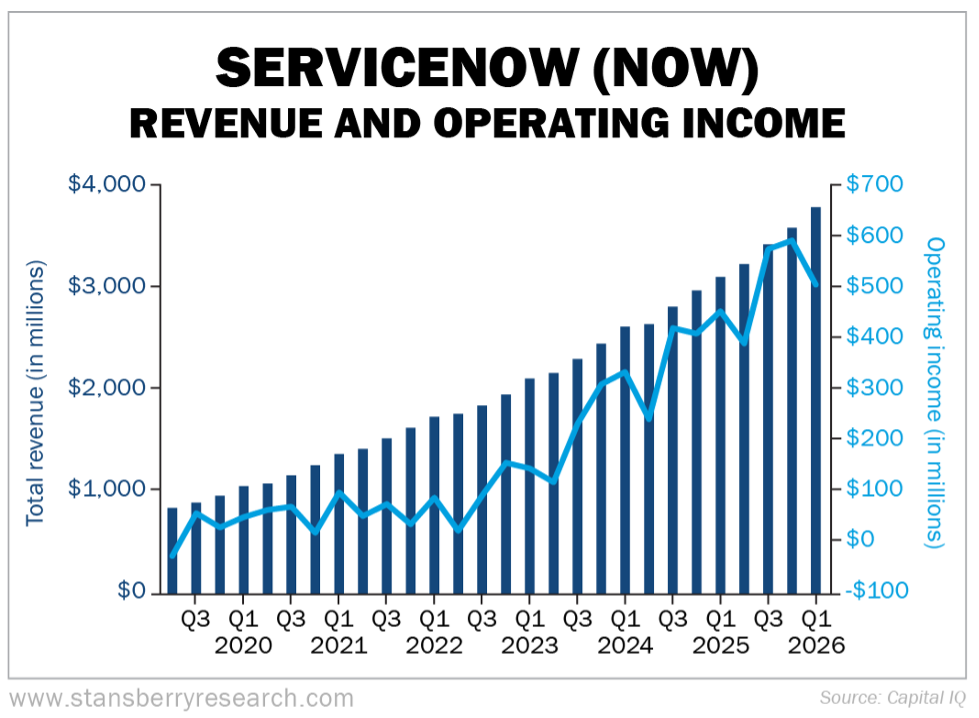

Revenue has risen steadily every quarter for the past seven years. And operating income, while a bit seasonal, has kept pace:

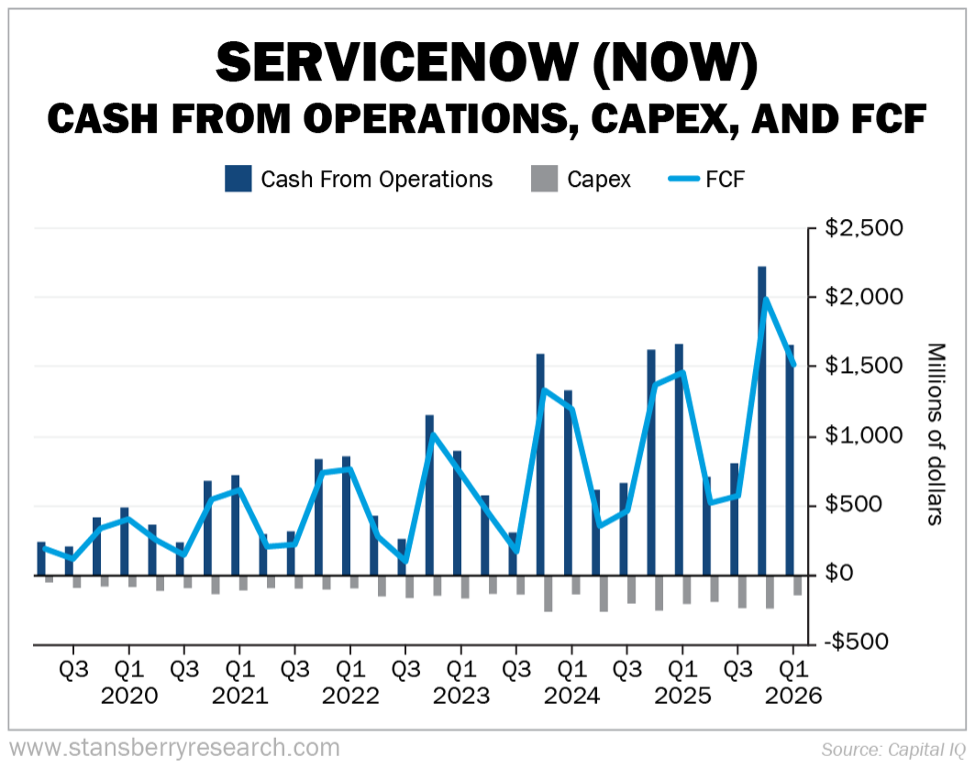

The business generates high and rising (albeit seasonal) free cash flow (“FCF”), with minimal capital expenditures (“capex”):

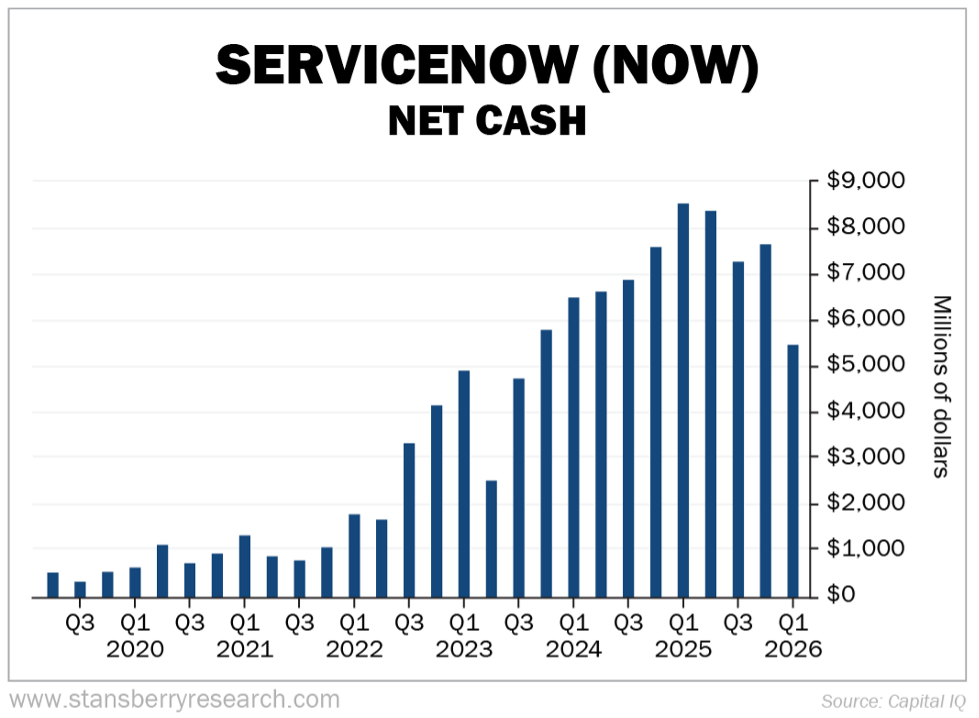

And the balance sheet is strong, with a healthy net cash position of $5.5 billion:

ServiceNow’s historical financials don’t explain the stock’s massive sell-off. So what does?

Two words: “SaaSpocalypse” and valuation.

ServiceNow Is a Victim of the SaaSpocolypse

Driven by fears that artificial intelligence (“AI”) is going to undermine shares of software-as-a-service (“SaaS”) businesses, investors have dumped these stocks, leading to what’s being called the “SaaSpocalypse.”

I think the sell-off in software stocks is overdone, which is creating wonderful investment opportunities. It’s worth repeating some of what we wrote in the Investment Advisory then before diving back into ServiceNow…

We highlighted why we don’t think companies are likely to rip out mission-critical software in favor of AI:

Major companies choose big software vendors with established reputations because they can trust them. They want someone they can rely on.

No less important, they want someone to blame when things go wrong. In the business world, folks call this “one throat to choke.”

If you’re an executive who cheaps out by developing software internally or switching to an unknown startup, you’ll shoulder the blame if things go wrong. You’d rather deal with a big company with deep pockets… round-the-clock customer service… proven data security… and the staying power to still be in business in five years.

We think AI will prove to actually be a good thing for many software companies, as it expands markets and creates new ways to profit:

AI will do what SaaS did for the software market 20 years ago… grow the software pie. It will make software available to far more companies and embed it deeply into more business processes.

That doesn’t mean every software company will survive this rapid AI transition. It will be painful for some. But still others will do better than ever. The problem is, the market hasn’t figured out which is which.

So my team and I developed a proprietary framework for evaluating software companies – including their resilience against AI:

[We] started by evaluating all 258 publicly traded software companies against 12 criteria. These included things like whether software is a “system of record” that controls proprietary customer data, has embedded workflows and can “talk” to other software programs, has high switching costs, and is a platform rather than simply a user interface…

Large SaaS platforms that have proprietary customer data, years of usage patterns, and embedded workflows will survive. Companies that make nothing more than a slick user interface or a fancy dashboard are toast.

Simple applications can be swapped out. Other types of software are so embedded, they’re like connective tissue – very hard to replicate and replace.

Then we applied a scoring system:

With the help of AI, we scored each company on all 12 criteria on a scale of 1 (highly vulnerable to AI substitution) to 10 (structurally resistant).

We weighted the 12 factors by importance. We then took the weighted average of the grades to rank which companies are most durable… and which are most at risk. The higher the score, the more resilient the company is. The lower the score, the more vulnerable.

In the March issue of Stansberry’s Investment Advisory, we shared a list of the 20 software companies with the highest score – meaning they’re the least vulnerable to the threat of AI.

ServiceNow was ranked sixth among the 258 companies we evaluated, putting it in the top 2.3%.

The biggest reason my team and I like the company is because its software is positioned to benefit the most from the shift to agentic AI. And the stock today is the cheapest it has ever been.

ServiceNow Is Taking Advantage of AI Advances

In our March write up of ServiceNow, my team and I detailed its expertise:

ServiceNow sells workflow-management and AI-orchestration software. This software sits above a company’s existing enterprise systems…

This ServiceNow software coordinates and manages AI workflows across customers’ software systems through a centralized oversight layer. ServiceNow calls this the “AI Control Tower.”

This isn’t just another agentic AI tool. It’s the governance and orchestration layer for all AI agents and workflows.

This is the type of software companies need to take full advantage of agentic AI.

We highlighted how it began evolving into a broad workflow-based platform long before the term “agentic AI” was commonplace:

[CEO] McDermott has a history as a visionary leader. He was previously CEO of SAP – the German software giant that sells every type of corporate software you can think of. He oversaw SAP’s transition to the [Software as a Service (“SaaS”)] model, doubling its revenue and tripling its market cap from 2010 to 2019.

He’s doing similar things at ServiceNow. Under his leadership, ServiceNow has quadrupled its revenues and doubled its market cap.

As McDermott pointed out on the company’s [fourth-quarter] earnings call, ServiceNow has reached $1 billion, $5 billion, and $10 billion in revenue faster than any other enterprise-software company (not counting acquisitions). And it will hit $15 billion this year.

Investors worry whether this organic growth will continue, as fewer software licenses will be bought by humans when AI agents take over their work. But as we explained, ServiceNow can simply switch to “usage-based” licenses:

ServiceNow began doing this in 2023 with the launch of its generative AI software suite, Now Assist. It charges customers based on the amount of work completed by AI agents rather than the number of humans using its software.

In its latest quarter, bookings of its Now Assist software more than doubled to $600 million in annual contract value. We’ll be keeping an eye on this performance, but we’re optimistic that ServiceNow’s usage-based AI revenue will keep growing faster than any loss of legacy [human]-based revenue.

I’m also bullish on the company’s biggest competitor, Salesforce (CRM). But I like ServiceNow better for highlighted several reasons:

ServiceNow is growing sales twice as fast (about 20% per year versus 10%).

About 5% of ServiceNow’s sales come from Now Assist, while Salesforce’s Agentforce generates just 2% of the company’s sales.

Also, ServiceNow has historically focused on “back office” software (IT, security, human resources, legal, supply chains), while the more narrow “front office” uses (sales and marketing) have been Salesforce’s specialty.

That gives ServiceNow a technological advantage. It built its software from the ground up to work across departments using a single data model. Salesforce did not. Its software often requires custom development for workflows outside of its core sales and marketing software.

ServiceNow Is a Fantastic Company Sell for Dirt Cheap

In summary, ServiceNow is well positioned to continue growing at a high rate and maintain its mouth-watering margins and free cash flows.

Yet amid the SaaSpocalypse, the stock is priced at its lowest valuation ever… as if it’s never going to grow again.

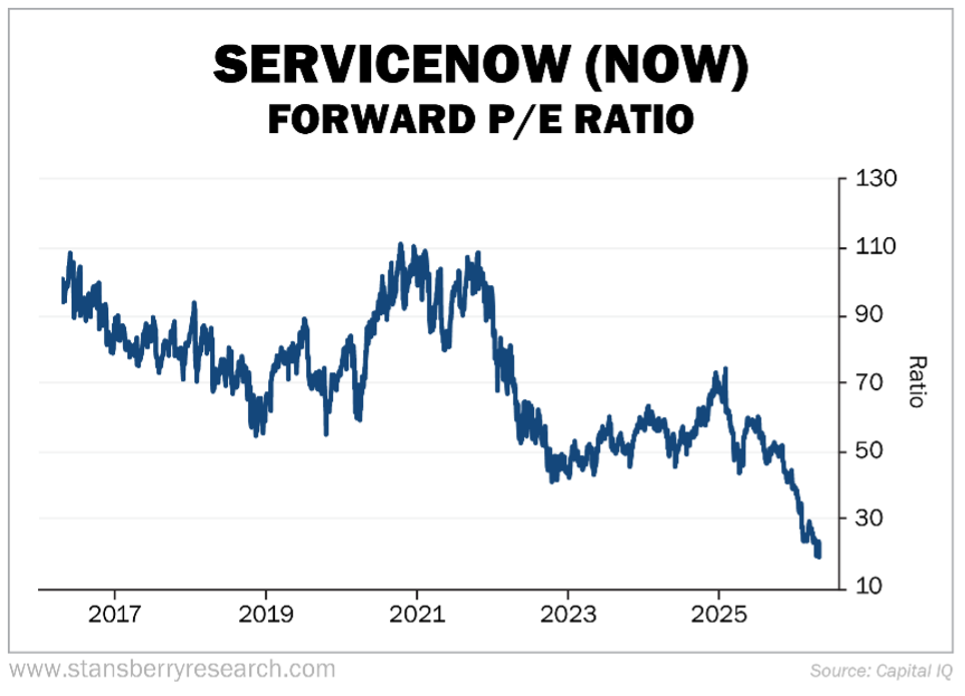

For nearly all of its existence as a public company, investors (rightly) valued ServiceNow at an extremely high earnings multiple. And they were richly rewarded for it, as the stock rose nearly 50 times from its 2012 IPO through mid-December 2024.

The stock has traded at an average 71 times forward price-to-earnings (P/E) multiple over the past decade, peaking at 111 times, as you can see in the chart below:

Yet after the stock’s precipitous decline, it now trades close to its all-time low of just 21.3 times consensus analysts’ estimates for this year and 17.5 times next year’s, based on this morning’s price around $88.

Those are downright cheap multiples for a business as fantastic as ServiceNow.

Over time, ServiceNow’s usage-based license fees should exceed what it would have earned under its previous model. The company should be able to continue growing revenue at 20% a year, conservatively.

Meanwhile, AI will help the company cut costs on research, development, and customer service. So its earnings should grow even faster than revenue – 25% per year, easily.

Averaging 20% revenue growth and 25% earnings growth over the next five years translates into earnings of around $11 per share.

If we assume that the current panic subsides and investors award the stock a multiple of 30 times earnings – less than half its historical range – that would make the stock worth $330.

That’s almost four times today’s price. And ServiceNow could easily beat those projections and rise even faster.

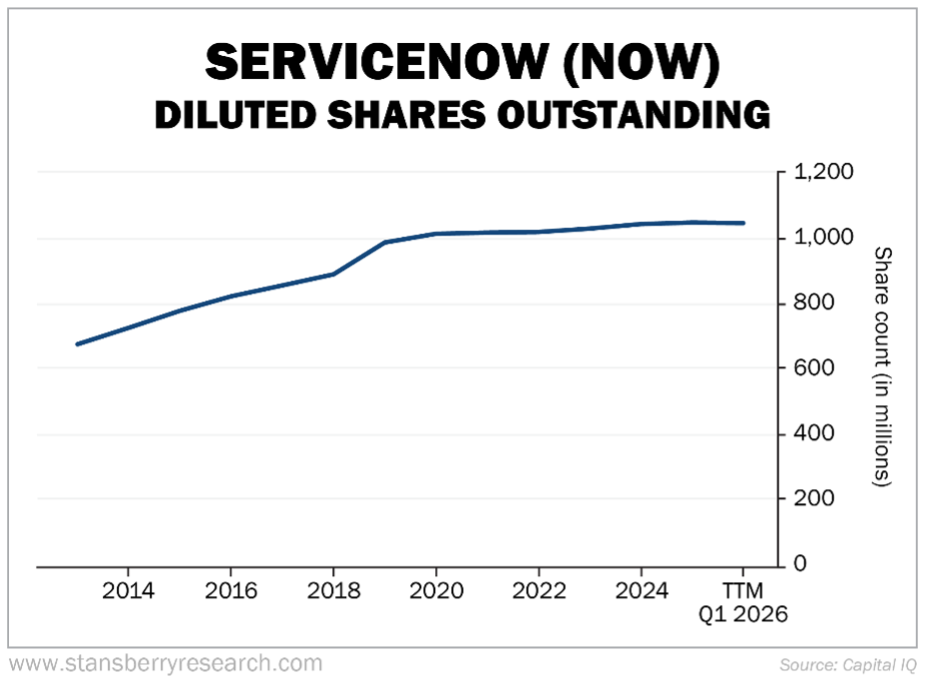

My team and I have only one complaint: ServiceNow – like many software companies – relies heavily on stock-based compensation to reward employees.

As a result, the company’s shares outstanding have increased by 54% since 2013, as you can see in this chart:

That share-count growth, however, has slowed in recent years thanks to well-timed share repurchases. And last year, with the stock price falling, the company massively ramped it up, as you can see here:

Earlier this year, ServiceNow’s board authorized $5 billion more for share repurchases, on top of $1.4 billion it had already reserved for buybacks. And the CEO also thinks the stock is a bargain, as he bought $3 million worth of stock with his own money in February.

I agree with him that this is a “once-in-a-generation moment.” And it helps reinforce why my team and I at Investment Advisory recommended the stock…

As I’ve said previously, the sell-off in software stocks has created wonderful investment opportunities. With ServiceNow, the SaaSpocalypse has given us a bargain on a fantastic business that’s poised to profit further.

If you aren’t a subscriber, you can become one – and gain access to our specific “buy up to” price for the stock and recommended way to protect your capital, as well as our full portfolio of other open recommendations