On February 10, Vertiv (VRT) stock closed at just under $200. On February 11, after Vertiv reported its 2025 fourth-quarter earnings, its stock soared to $249.95 before finishing the day at an all-time closing high of $248.51… an increase of nearly 25%.

It was a strong fourth quarter for Vertiv, a large-cap (roughly $90 billion market cap) company that specializes in the critical power, integrated infrastructure, and precision cooling that support the massive workloads of artificial intelligence (“AI”) data centers.

As my colleague John Robertson wrote back in May, when Vertiv stock was surging:

Increasingly, the company is also known for whole, prefabricated “AI factories” that arrive on site like giant Lego blocks, ready to energize graphics processing units (“GPUs”).

Think of Vertiv as the “plumbing” underneath critical AI infrastructure.

That might not sound exciting. But providing AI “plumbing” may make Vertiv one of the most valuable companies of the coming AI revolution.

Based on Vertiv’s fourth-quarter earnings and 2026 projections, it looks like John nailed it.

How Vertiv Powers AI Data Centers and Why That’s Important

Vertiv describes itself as “a global leader in critical digital infrastructure for applications in data centers, communication networks, and commercial and industrial environments.”

The Ohio-based company offers end-to-end infrastructure in these environments. That infrastructure encompasses power management, cooling, plug-and-play data-center modules and racks, and services such as remote monitoring, predictive maintenance, and life-cycle management.

Among Vertiv’s core offerings are:

- Power distribution units (“PDUs”) designed to handle the high-voltage needs of AI data centers.

- AI-ready uninterruptible power supply (“UPS”) systems that effectively handle rapid power load changes for smooth and consistent operation.

- Battery energy storage systems (“BESS”) and other solutions that allow data centers to build microgrids, which reduce dependency on the utility grid.

- A wide range of cooling solutions that are critical to AI computing performance.

- A line of prefabricated infrastructure and power solutions – including new products OneCore and SmartRun – designed for easy and fast deployment.

Put simply, Vertiv’s products and services help power data centers and cool the equipment within those data centers across the globe.

As more AI data centers are built, Vertiv is poised to provide the solutions they need to perform optimally.

And Vertiv’s services are in high demand.

Vertiv’s Fourth-Quarter and Full-Year 2025 Success Drives Stock Price up

Vertiv’s 2025 fourth-quarter earnings call offered plenty of highlights…

The company reported year-over-year organic sales growth of 26% for the full year. Its cash flow also grew significantly… Vertiv’s 2025 operating cash flow was $2.11 billion (up 60%), and its adjusted free cash flow hit roughly $1.9 billion (a 66% increase).

Vertiv also reported full-year diluted earnings-per-share (“EPS”) growth of 166% and adjusted diluted EPS growth of 47%. Additionally, its fourth-quarter revenue of $2.88 billion marked a 23% year-over-year increase.

But it’s another number that has investors bullish on Vertiv… its $15 billion backlog.

In the fourth quarter of 2025, Vertiv’s organic orders skyrocketed about 252% year over year. That increased the company’s book-to-bill ratio to roughly 2.9… more than doubling (109% increase) its 2024 fourth-quarter backlog. That backlog also grew sequentially, up nearly 58% from the book-to-bill ratio in the third quarter of 2025.

This is what we meant when we said Vertiv’s products and services are in demand. And that paves the way for a profitable 2026.

Vertiv’s 2026 Outlook Is Promising

Vertiv’s robust 2025 earnings bolstered its position as a data-center and AI-infrastructure leader. And its 2026 outlook illustrates the confidence the company has in its performance and its offerings.

Let’s take a quick look at Vertiv’s full-year 2026 projections:

- Net sales in the $13.25 billion to $13.75 billion range

- Organic sales growth of 27% to 29% versus 2025

- Diluted EPS between $5.27 and $5.37 (a year-over-year increase of 56% at the midpoint) and adjusted diluted EPS $5.97 and $6.07 (a 43% increase at the midpoint)

- Adjusted free cash flow between $2.1 billion and $2.3 billion

The targets are ambitious, but Vertiv is planning accordingly. The company is looking to increase capital expenditures (“capex”) to 3% to 4% of sales (it typically spends around 2% to 3% of sales on capex), as well as grow its manufacturing capacity for power solutions and thermal management in 2026.

Vertiv, based on its internal data-center trend research, is preparing new products and solutions to address the demands of next-generation AI data centers.

For example, many of today’s data centers rely on 54 volts direct current (“VDC”) levels to power their server racks.

These VDC levels are no longer powerful enough.

New data centers are adopting 800 VDC power architectures, which improve end-to-end efficiency and deliver the necessary power to support the power-hungry 1-megawatt (“MW”) server racks that will soon fill AI data centers.

Semiconductor king Nvidia (NVDA) is helping to lead the 800 VDC power transition in 2027 with its highly anticipated Rubin Ultra GPU platforms, and Vertiv will be a key partner in this endeavor. Vertiv plans to roll out its 800 VDC power portfolio during the second half of this year.

It’s also worth noting that, for Vertiv and Nvidia, this is the continuation of what has been a fruitful partnership. When Nvidia rolled out its Blackwell chips, it chose Vertiv as the lead supplier for its coolant distribution units (“CDUs”). Vertiv also codeveloped architecture with Nvidia to accelerate the deployment of Nvidia’s GB200 NVL72 liquid-cooled rack-scale platform.

As John Robertson succinctly stated in May:

Put simply, as Nvidia keeps pushing the thermal envelope, Vertiv sells the only plumbing certified to keep those chips from melting down − and it gets a clear, early signal of demand every time a new GPU launch inches closer.

On Vertiv’s docket for 2026, along with its continuing partnership with Nvidia, are:

- Expansion of liquid cooling capacity, including new configurations of Vertiv’s MegaMod HDX prefabricated power and liquid cooling solution. MegaMod HDX uses direct-to-chip liquid cooling along with air-cooled architectures to effectively cool AI equipment and environments.

- Next Predict, an AI-powered service that combines Vertiv’s field expertise (the company employs roughly 4,000 field service engineers globally) and advanced machine learning to identify potential cooling issues before they surface.

- Implementation of a digital twin strategy. This involves Vertiv creating full-scale digital twin simulations of AI data centers before they’re built. These digital twins help optimize data-center layout to improve cooling and power efficiency. And once the data centers are operational, the digital twins serve as “virtual operators” that manage and monitor the data centers in real time.,

- Collaboration with Oklo (OKLO), an advanced nuclear technology company, to develop advanced thermal management and power solutions for colocation and hyperscale AI data centers. The two companies are partnering on a pilot program to power and cool data centers via steam and electricity from Oklo’s nuclear power plants. The pilot is expected to launch in late 2027 or early 2028, when Oklo’s Aurora powerhouse becomes operational.

Vertiv’s profitable 2025 and ambitious 2026 plans offer investors several reasons to be bullish about the company. As always, however, there are a few things to weigh before investing in Vertiv.

Risks to Watch When Considering Investing in Vertiv

There’s plenty of justifiable optimism surrounding Vertiv. But it’s always important to consider potential risks before investing.

First and foremost, Vertiv’s 2025 success and 2026 forecast put the company in the spotlight. Now Vertiv must keep performing. With VRT shares on a lengthy bull run, the stock is priced with high expectations built in. If the company falters even a little bit or misses analysts’ expectations, its stock suddenly becomes very vulnerable.

Second, that $15 billion backlog is impressive. But now Vertiv has to execute on and fulfill that backlog… even if there are factors beyond its control, such as tariff costs and supply chain or logistical issues that eat into the company’s margins.

Then there’s the competition. AI infrastructure has become an increasingly crowded area, and Vertiv has its share of formidable competitors. Schneider Electric (SU.PA) and Eaton (ETN) are two reputable and successful power players in the AI-data-center space. Even Caterpillar (CAT) has gotten into the action with its backup generators designed for data centers.

On the thermal management front, Hewlett Packard Enterprise (HPE) and Super Micro Computer (SMCI) produce high-quality liquid cooling solutions of their own.

Finally, Vertiv is highly dependent on the AI industry. Thus far, the company has reaped the benefits of global AI-data-center expansion. And it’s in prime position to continue doing so.

However, AI is a highly volatile sector.

If AI infrastructure growth slows or spending decreases, Vertiv (and many other companies) will feel that impact, and it will hurt.

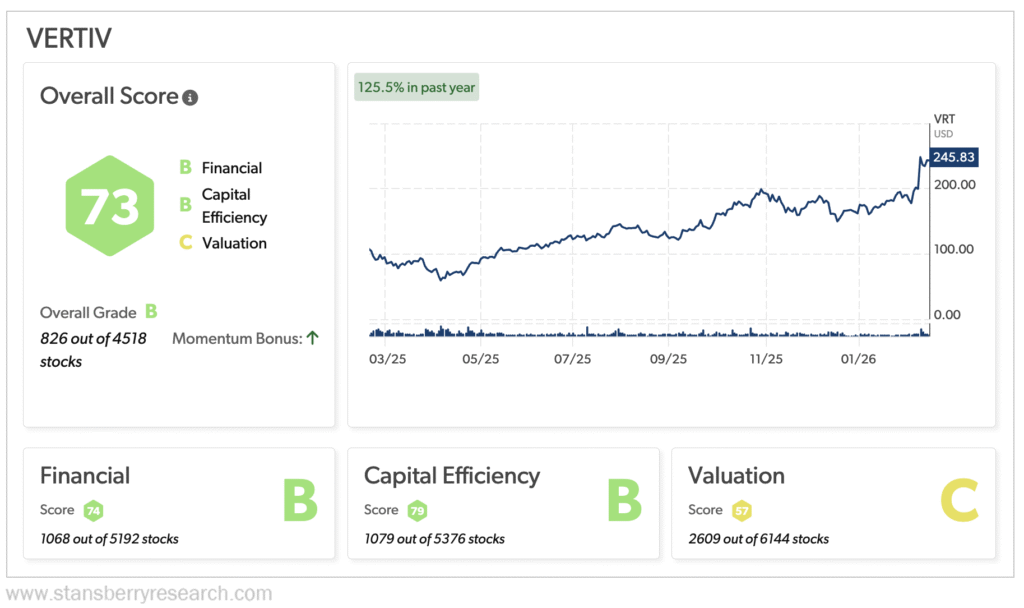

A Look at VRT Stock

Overall, VRT stock is on solid ground. A look at its Stansberry Score, a tool that helps determine the quality and long-term value of thousands of stocks, shows generally strong performance with an overall “B” grade.

Thanks to Vertiv’s profitable 2025 and promising 2026, it earns a “B” grade in the Financial and Capital Efficiency categories. Its “C” grade for Valuation, however, is cause for some concern.

Many analysts view VRT as overvalued, and its Stansberry Score reflects that opinion. The stock surged more than 120% over the past year, driven by AI-data-center demand, one reason Wall Street sees VRT’s price dropping in the next 12 months.

Plus, Vertiv’s trailing-12-month (“TTM”) price-to-earnings (“P/E”) ratio is high at roughly 70. For comparison, the U.S. electrical industry average P/E ratio is around 35, and Vertiv’s direct peer average P/E ratio ranges between 35 and 45.

The bearish argument? Those P/E ratios make VRT an expensive proposition versus its competitors.

On the bullish side, however, its forward P/E ratios are substantially lower, ranging from 39 to 43. That reflects Vertiv’s healthy growth prospects from here, driven by the company’s $15 billion backlog and projected sales for 2026.

Vertiv Is an AI Stock to Watch

Vertiv is a company that can address arguably the biggest challenges and bottlenecks AI data centers face today: power and cooling. It also happens to meet these challenges rather successfully… looking at Vertiv’s 2025 financials and 2026 forecasts will tell you as much.

More importantly, Vertiv has built something of a moat in the increasingly critical area of AI infrastructure with its innovative cooling and power solutions. The company continues to look forward as it anticipates future AI-data-center demands and needs and then creates the solutions to address them.

It should be a fascinating year for Vertiv, given everything it has on the horizon. Can it build on its strong 2025? How will the company handle its impressive backlog? And will its earnings justify its high share price?

There’s only one way to find out. Keep a close eye on Vertiv in 2026.

Regards,

David Engle

P.S. It’s no secret that artificial intelligence is gobbling up energy at an unprecedented rate… straining America’s already vulnerable power grid.

All the big players are racing to find a new way to meet AI’s power-hungry daily demands, pouring in billions of dollars for alternative energy sources.

Regular folks can still get in on this tech, too – but time is running out.

Because Amazon (AMZN) may have just cracked the code.

This breakthrough technology is being hailed as “the Holy Grail of Power,” and Amazon just went all-in on it…

Get the details right here, including how to prepare and what to buy.