Natural gas is certainly in demand these days. Just months ago, I wrote about data centers and how their seemingly unquenchable thirst for power put natural gas in the spotlight as a solution:

According to Deloitte analysis, the power demand from AI data centers alone could increase more than 30 times in the U.S., going from 4 GW in 2024 to 123 GW by 2035. That’s enough to electrify nearly every household on the East Coast, or 100 million homes.

The report noted that AI only accounted for 12% of the 33 GW U.S. data-center power demand in 2024… a figure set to grow to 70% in 10 years…

Today, America simply does not generate enough power to meet the expected demand of data centers… natural gas will be the energy source that helps fuel the AI boom, at least in the near term.

This all remains true. But now there’s one more reason to be bullish on natural gas… and it’s an unfortunate one.

The conflict between the United States, Israel, and Iran is disrupting the world’s liquefied natural gas (“LNG”) supply.

The Strait of Hormuz, a critical waterway separating Iran’s southern border and the northern borders of Oman and the United Arab Emirates (“UAE”), is effectively closed to most commercial ships.

Why does this matter?

Because roughly 20% of the world’s globally traded LNG (and oil) flows through the Strait of Hormuz.

Even a minor shipping disruption is enough to make the market react. This is why global crude oil prices soared more than 10% in the immediate aftermath of the initial U.S.-Israeli strikes on Iran. And why natural gas prices in Europe and Asia, which rely heavily on LNG imported from Qatar and the UAE, have jumped even more.

On Tuesday, March 3, the Dutch Title Transfer Facility (“TTF”) – the main hub for buying and selling natural gas in Europe, and the European benchmark – skyrocketed nearly 70% to roughly 54 euros per megawatt-hour (“MWh”) from the previous Friday, based on data from the Intercontinental Exchange (“ICE”) Index. The United Kingdom saw a similar jump as natural gas prices surged 40% over that same weekend.

While these price increases severely tighten energy markets, they also benefit natural gas investors due to the threat of a worldwide energy supply shortage.

The LNG Bottleneck Is the Real Story

On March 4, a drone attacked Saudi Aramco’s Ras Tanura oil refinery, the country’s largest refinery and an important crude oil export terminal. While there was no reported damage or interruption in service, it signals Iran’s willingness to attack key energy hubs in the region.

Since the Iran war began on February 28, critical Persian Gulf oil producers such as Saudi Arabia, Iraq, the UAE, and Kuwait haven’t been able to move their oil through the Strait of Hormuz. As of March 2, traffic in the strait for both LNG and oil had declined by 86 percent. The fear of Iranian attacks on tankers has roughly 700 ships anchored on each end of the strait.

More than 20 million barrels of crude oil pass through this waterway every day, so the lack of movement is choking the global oil supply.

Without the typical supply of oil, LNG becomes even more important. However, LNG coming from the region – particularly Qatar – remains in a holding pattern as well.

On Monday, March 2, QatarEnergy – the world’s leading LNG company and producer – announced it would be shutting down its LNG operations after being hit by an Iranian drone. The stoppage could potentially last weeks. The attack also prompted the company to push a major LNG expansion project back to at least 2027.

Qatar, primarily through QatarEnergy, accounts for roughly 20% of the world’s liquefied natural gas exports. That’s second in the world after the U.S.

Even if QatarEnergy hadn’t been attacked, its entire LNG supply travels through the Strait of Hormuz. So, 20% of the world’s LNG exports would be cut off either way.

This is a big problem, particularly for Europe and Asia. More than 80% of QatarEnergy’s LNG exports go to Asian markets, and around 10% to 15% go to Europe.

Adding another layer of complexity to the situation is how immensely vulnerable the world’s energy supply is to any type of geopolitical tumult in the Middle East.

The LNG market, unlike oil, offers little to no spare capacity. And with roughly one-fifth of the world’s total LNG supply passing through the Strait of Hormuz, any event that impacts passage along this waterway results in instant, massive worldwide supply constraints and huge price surges.

Can the U.S., as the world’s largest exporter of liquefied natural gas, help solve the crisis?

Why U.S. LNG Exports Matter More Now

As soon as the Qatari LNG industry was stopped in its tracks, the United States became the likely beneficiary of the shutdown.

But it won’t be because the U.S. LNG industry can boost its current production levels. American producers are already nearly maxed out. As it stands now, the world’s LNG supply is 20% short until QatarEnergy is up and running at peak capacity again.

Where the U.S. can help, however, is in determining where its LNG can go. American customers’ contracts don’t include fixed destinations. That flexible capacity, which is unique to the U.S. LNG industry, allows LNG to be rerouted to wherever it’s needed.

A similar situation occurred in 2022 after Russia invaded Ukraine, leaving Europe short of LNG supplies. U.S. producers were able to step in and deliver LNG to Europe.

In doing so, Henry Hub prices – an important pricing point based on actual natural gas supply and demand, which serves as a benchmark for the North American natural gas market – soared.

With American LNG in high demand during the Russia-Ukraine war in 2022, Henry Hub prices averaged $6.45 per million British thermal units… significantly more than their 2021 average of $3.89.

Henry Hub pricing comes into play during the Iran war through arbitrage. This, according to Natural Gas Intelligence, “occurs when the cost of shipping LNG between points A and B is less than the price spread between those two points.”

In other words, arbitrage exploits the price differences for LNG between at least two regional markets by purchasing the gas in a lower-priced region and then selling it in a higher-priced one. A profitable arbitrage “window” opens when the price spread exceeds shipping and operational costs.

With Henry Hub pricing serving as the cost benchmark for U.S. LNG exports, traders can profit from arbitrage through the price spread between cheaper domestic LNG and the more expensive international markets… such as the European TTF benchmark and the Asian Japan Korea Marker (“JKM”) benchmark.

When those prices rise in comparison with Henry Hub, the arbitrage window grows and pulls more U.S. LNG exports into the global markets.

Iran’s Gas Wealth Doesn’t Solve the Problem

Iran is sitting on plenty of proven natural gas reserves… roughly 1,200 trillion cubic feet, second worldwide to only Russia. Iran also produces the third-most natural gas in the world, behind only the U.S. and Russia.

But volume and production aren’t the problem.

Exporting is the issue for Iran.

A combination of sanctions and infrastructure shortcomings prevents the country from reliably exporting its massive amounts of natural gas globally. Instead, Iran primarily exports only to its neighbors, Turkey and Iraq.

So, even with an abundance of natural gas at its disposal, Iran can’t quickly replace disrupted LNG resources. That means the global LNG market remains dependent on the top three exporters: the U.S, Qatar, and Australia.

And with Qatar’s LNG supply currently in limbo, the United States becomes the world’s marginal supplier of liquefied natural gas.

Natural Gas Stocks Positioned for Export Leverage

Here are three American natural gas stocks that could benefit from increased exporting of LNG while Middle Eastern supplies are limited.

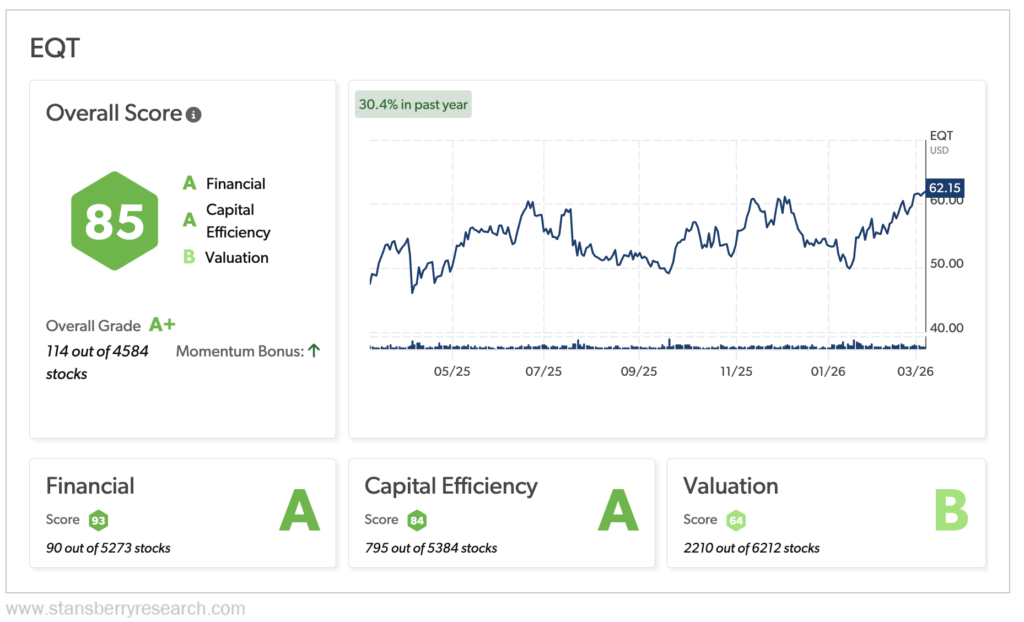

EQT (EQT)

EQT, one of the largest natural gas producers in the U.S., controls the Mountain Valley Pipeline, a 303-mile natural gas pipeline that runs from West Virginia to Virginia.

Its operation in the Appalachian Basin controls roughly 27.6 trillion cubic feet of proved natural gas reserves from the natural gas-rich Marcellus and Utica shale formations across Pennsylvania, West Virginia, and Ohio.

Thanks to its vast reserves, EQT is one American natural gas producer that could see its exports increase due to the conflict in the Middle East. The company’s stock price, profitability, and free cash flow are also highly sensitive to changes in the Henry Hub natural-gas benchmark price. So, when gas prices rise – like they are now – EQT enjoys significant increases in revenue.

This was evident when EQT stock hit its all-time closing high of $62.23 on March 9.

Along with the potential for major short-term increases in LNG exports, EQT is also riding the artificial intelligence (“AI”) data center wave. The company has secured long-term natural gas supply agreements to support data center and AI-related demand through 2030.

EQT’s Stansberry Score (a tool that helps determine the quality and long-term value of thousands of stocks) is outstanding, earning an overall “A+” grade. That ranking is supported by the company’s roughly $8.6 billion in revenue for the 12 months ending December 31, 2025 – a massive increase of more than 62% versus the prior-year period.

EQT also generated nearly $3 billion in free cash flow last year. And its $2.3 billion in net income was a staggering increase from $242 million in 2024.

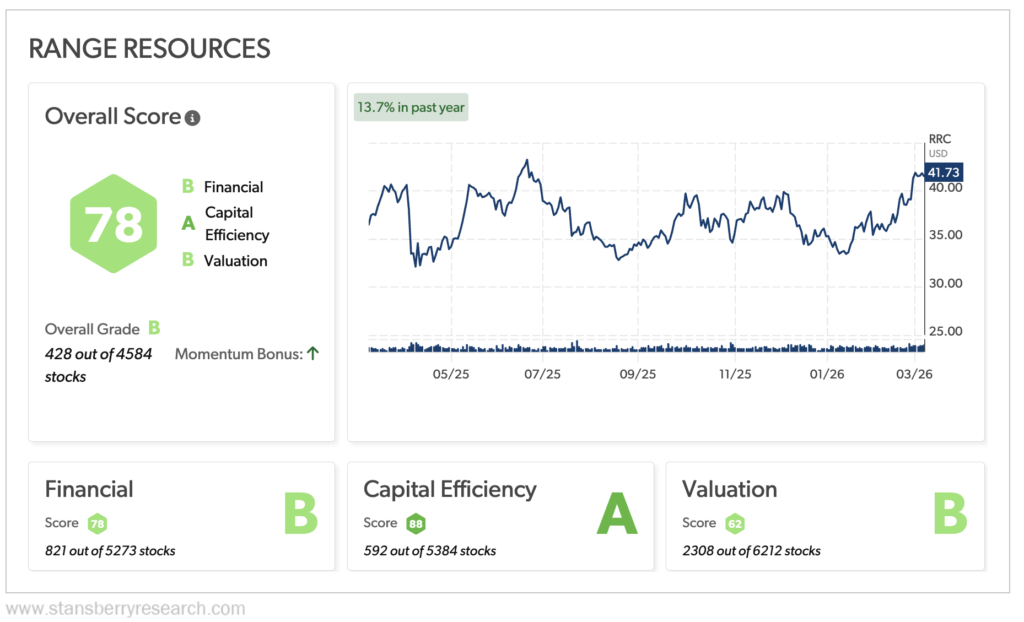

Range Resources (RRC)

Range Resources is another major American natural company poised to benefit from the Middle East conflict. The company is a low-cost Appalachian gas producer and proclaims itself the “pioneer of the Marcellus Shale.”

Range Resources, through long-term transportation agreements, moves its Marcellus Shale gas to export terminals and premium LNG export markets.

For example, Range Resources has a 20-year deal with Energy Transfer (ET) to transport gas to its Gulf Coast ports. The company is also instrumental in the Mariner East project, which delivers natural gas liquids from the Marcellus Shale to Sunoco’s (SUN) international port in Marcus Hook, Pennsylvania.

And during Range Resources’ 2025 fourth quarter, the company secured a 10-year agreement to supply natural gas to a Midwestern power plant starting in late 2027.

Business was already booming for Range Resources. The rising energy prices spurred by the Iran war certainly don’t hurt. Neither does the growing need for U.S. LNG exports to fill in the gaps while Middle Eastern supplies are cut off.

A quick look at RRC’s Stansberry Score shows rock-solid performance, with an overall “B” grade. One highlight is its Financial rating (“B”), thanks to generating more than $3.1 billion in revenue, $1.2 billion in operating cash flow, and $650 million in free cash flow during 2025.

RRC’s Capital Efficiency was also outstanding, earning an “A” in part because of its $317 million in shareholder returns ($86 million in dividends and $231 million in share repurchases).

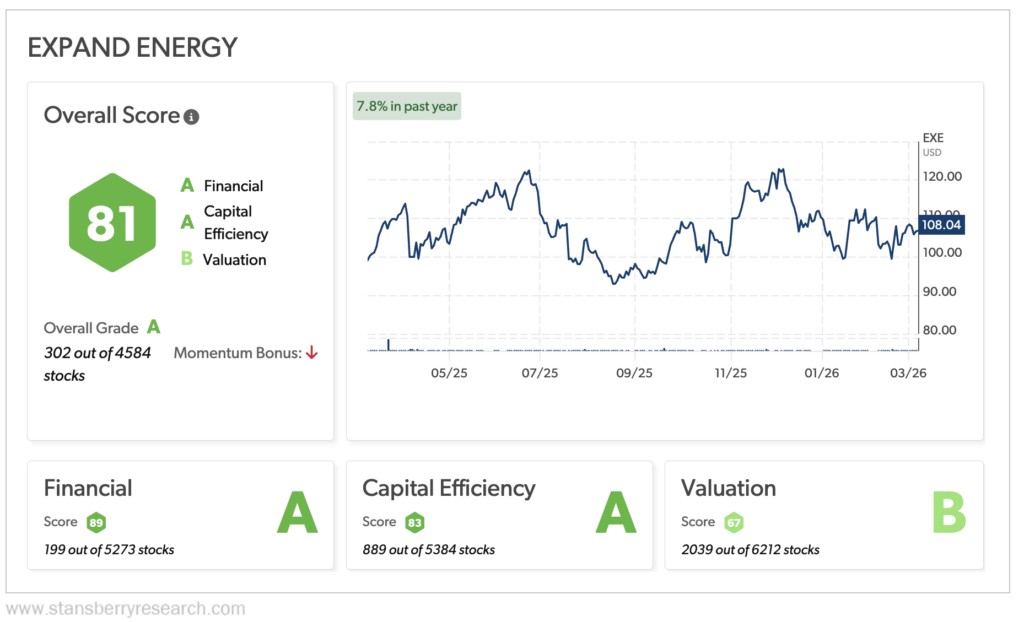

Expand Energy (EXE)

As the largest natural gas producer in the United States, Expand Energy is a prime candidate to benefit from the Middle East LNG supply shortages.

Along with its massive production volume (roughly 7.18 billion cubic feet of gas equivalent per day, consisting of 92% natural gas), location is key for Expand.

Its Haynesville Shale (spread across Northwest Louisiana, East Texas, and Southwestern Arkansas) is close to Gulf Coast LNG export terminals, making exporting gas internationally quite easy.

Between its natural gas volume, its ideal position near LNG export infrastructure, and low-cost production, Expand Energy is a logical candidate to provide Europe and Asia with the LNG they’re not currently getting from Qatar.

Like EQT and Range Resources, Expand Energy is a highly profitable business. In 2025, it reported cash flow provided by operating activities of nearly $4.6 billion and net income of more than $1.8 billion.

Expand also reduced its gross debt by an impressive $660 million in 2025.

That’s why EXE earns an “A” for its Stansberry Score. Not surprisingly, the company’s Financial score is also an “A,” as is its Capital Efficiency… thanks to $865 million returned to shareholders in 2025.

Risks for Investors to Watch

The conflict in the Middle East is undoubtedly helping American LNG producers and exporters. And that can certainly benefit those investing in American LNG and energy companies, especially in the short term.

But there are risks involved when investing in these types of stocks during wartime.

For one, whenever the situation de-escalates, LNG operations in the Middle East will resume. It may take QatarEnergy some time to reach previous levels of LNG production, but that will happen eventually. And when it does, natural gas prices should normalize. Natural gas stocks will likely follow suit.

Second, as liquefied natural gas exporters ramp up production, there’s some fear of an imminent LNG glut.

According to September 2025 reporting from oilprice.com, “Huge export capacity additions, mostly in the United States and Qatar, are set to tip the global LNG market into an oversupply as soon as next year, depressing prices and eating into the profit margins of the U.S. LNG exporters.”

Of course, this timeline will be delayed because of the disruption in Qatari LNG production and export. But you don’t need to read between the lines to see that an LNG oversupply represents a major risk to both American LNG exporters and their investors.

Looking at the longer term, a somewhat recent regulation change could also give investors pause.

Last year, the U.S. Trade Representative announced that, starting in 2028, at least 1% of American LNG exports must be transported on U.S.-flagged vessels.

By 2029, 1% of LNG export vessels must be built in the U.S. By 2047, 15% of LNG exports must be shipped on U.S.-flagged and U.S-built vessels.

That 1% may not seem like much. But it’s worth noting that as of August 2025, the United States – the world’s largest LNG exporter – had a grand total of one U.S.-flagged vessel among the global operational LNG fleet.

One. And it was built in France.

Perhaps that’s nothing to worry about now. But building LNG tankers is going to cost American exporters a lot of money.

For perspective, it costs around $250 million to build one large-scale LNG vessel in Korea. It may cost five times as much to build that same vessel in America.

Compliance with this new regulation will cost American LNG exporters several billions of dollars.

The Natural Gas Bull Case Is Growing

AI data centers and their never-ending need for power are clearly the primary driver of the natural gas bull market. But geopolitical tensions and events are expanding that bull case.

The Iran war, sadly, has proven that, with global LNG supplies severely choked off in the Strait of Hormuz.

The loss of roughly 20% of the world’s LNG exports from Qatar to Europe and Asia has not only tightened supply and raised natural gas prices in the process, but it has also opened the door for American LNG exporters to reroute their supplies to those continents.

And by doing so, they put U.S. natural gas in even higher demand. The three stocks we covered today look like solid bets to reap the benefits of this market shift, especially in the short term.

Regards,

David Engle

Editor’s note: It’s no secret that artificial intelligence is gobbling up energy at an unprecedented rate… straining America’s already vulnerable power grid.

All the big players are racing to find a new way to meet AI’s power-hungry daily demands, pouring in billions of dollars for alternative energy sources.

Regular folks can still get in on this tech, too – but time is running out.

Because Amazon (AMZN) may have just cracked the code.

This breakthrough technology is being hailed as “the Holy Grail of Power,” and Amazon just went all-in on it…

Get the details right here, including how to prepare and what to buy.