Key Points

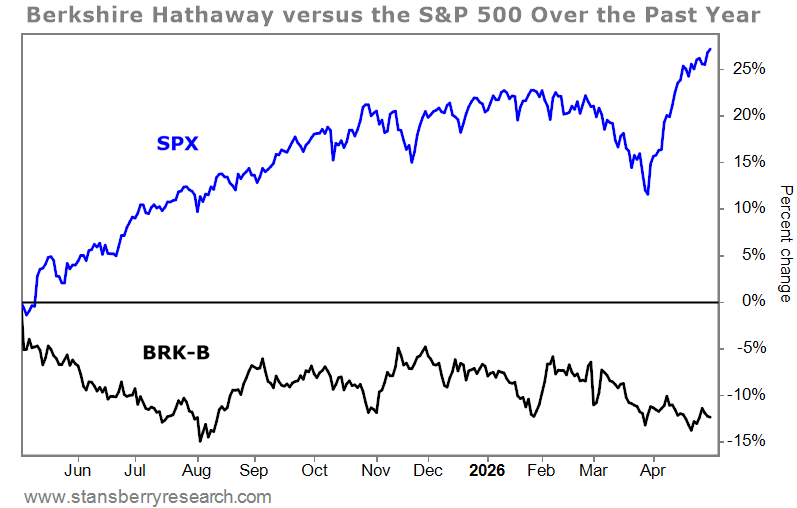

- Berkshire Hathaway stock has lagged the S&P 500 over the past year, underperforming by roughly 36 percentage points.

- Berkshire recently held its first annual shareholders meeting without Warren Buffett on stage, with new CEO Greg Abel taking questions from attendees.

- The stock may still offer attractive value given Berkshire’s collection of businesses, investment expertise, and nearly $400 billion cash position.

It’s been a rough year for Berkshire Hathaway (BRK-B). Legendary investor and business icon Warren Buffett stepped down as CEO. Since then, the stock has massively underperformed the benchmark S&P 500 index.

Berkshire stock is down about 9% from when Buffett announced his departure from the CEO role a year ago. In the meantime, the broader market, as represented by the S&P 500, has risen by more than 27%. At 36%, it’s not the kind of underperformance that characterized Buffett’s time as CEO.

So, coming off Berkshire’s latest annual meeting last weekend, it’s hard not to look back and be wistful. It was the first annual meeting without Buffett presiding. Of course, it was also the first one without the dynamic duo of Buffett and long-time investing partner Charlie Munger, who passed in 2023. In short order, the Berkshire guard has been changed.

New CEO Greg Abel now leads the annual meeting in Omaha, with chairman Buffett sitting in the audience. While Abel is a Berkshire veteran and Buffett has given him a stamp of approval, including at this most recent meeting, it’s been a hard sell for some Berkshire investors.

But if you look closer, you’ll see a stock that looks primed to earn market-beating returns once again.

Investors can’t earn last year’s returns. They can only shoot for future ones. So, the stock’s poor showing over the past year is a fat pitch waiting for Abel to hit a home run.

Berkshire’s Profit Rises in First Quarter Under Abel

Berkshire’s first quarter under Abel was a solid, maybe even great, performance. Operating profit came in at $11.3 billion, rising 18% year over year. Meanwhile, first-quarter net income rose from $4.6 billion last year to $10.1 billion in 2026, helped by investment gains.

With Berkshire’s wide range of subsidiaries – insurance, energy, railroads, and more – operating earnings provide a better measure of its fundamental performance than net income. Net income can be affected by the paper investment gains and losses from Berkshire’s $288 billion portfolio.

Abel addressed some of shareholders’ key concerns, in particular how Berkshire would change under his leadership. On the one hand, he suggested that the broader culture would remain the same. On the other hand, Abel suggested that Berkshire has “gaps” to fill in various businesses, but that the company has “exceptional teams” to solve them.

In practical terms, this distinction means that Abel may not make significant changes in some of Berkshire’s long-time investments, such as Coca-Cola (KO) or American Express (AXP). At the same time, it may mean incorporating artificial intelligence (“AI”) tools where they’re useful.

“We’re not going to do AI for the sake of AI,” Abel said. Instead, AI is being used “to solve logical problems in our businesses.” He added that Berkshire’s railway, BNSF, was starting to use AI tools.

Particularly interesting was the fact that Berkshire continues to amass cash rather than invest in stocks. It is now sitting on a staggering $397 billion in cash. Berkshire has been a net seller of stocks for 14 straight quarters, the longest streak in its history. Buffett has pared huge portions of his highly profitable stake in Apple (AAPL), for example, as the tech stock has reached all-time highs.

This pile of cash should provide another source of insight to forward-looking investors. Berkshire’s move seems to indicate that they’re not finding attractive places for money, so they’re holding on to it.

Is Berkshire Hathaway Undervalued Right Now?

If you peek at Berkshire’s expected earnings for 2026, it may not be obviously cheap. The average earnings estimate is $20.56 per B share, putting the stock at a price-to-earnings ratio of 22.7 times. That’s in line with the S&P 500, and not cheap in absolute or relative terms.

But Berkshire is playing with about $400 billion behind its back. That is, the company has $397 billion in cash that is not invested in its operating businesses or in stocks. This money is stuffed in short-term Treasurys that earn a low return but do offer the advantage of optionality. In fact, it’s enough cash to buy 479 of the 500 or so companies that comprise the S&P 500.

The cash hoard is one reason that the stock’s price-to-book ratio is a better measure of value, and also why it’s trading cheaper. (It’s a better yardstick for an insurance-heavy company, too.) On that basis, the stock is trading at about 1.37 times, as of its first-quarter numbers.

Factor in this cash against Berkshire’s $1 trillion market capitalization, and suddenly, Berkshire may not look like it’s under-earning. It has a lot of dry powder that can be put to work. Buffett and Berkshire have a habit of holding cash just when many other companies desperately need it.

Buffett did exactly this kind of maneuver during the 2008-2009 financial crisis, finding attractive investments for his war chest and lending to blue chips such as Goldman Sachs (GS) on favorable terms.

While investors may be loath to trust other executive teams with so much cash, Berkshire’s investment bench is legendary. So, investors are right to leave them to find the best uses for the money. That may mean lower short-term earnings in exchange for higher long-term earnings.

Berkshire has also been holding back on repurchasing its own stock, with buybacks declining to little more than a trickle over the past couple of years. Is that a negative vote for his own stock?

Maybe, but Buffett has long shown that he prefers having cash during a market decline. He (or Abel) is ready to make deals on good businesses at what may turn out to be wonderful prices.

In fact, Abel just addressed this issue at the annual meeting, indicating that Berkshire has a shortlist of candidates it would acquire, in part or in whole, if it can get the price it wants. “There will be dislocations in markets that will allow us to act,” said Abel.

So, with Berkshire stock, investors get that optionality on investing wizardry during a downturn, just the time when it’s best to have cash at the ready – all at a reasonable price.

Regards,

James Royal, Ph.D.

Editor’s note: Greg Abel’s first letter to Berkshire shareholders pointed out how much Warren Buffett had been influenced by baseball legend Ted Williams. It fascinated me because Altimetry’s Rob Spivey referenced the very same player in his recent investigation into why Buffett has chosen 2026 to step down. If you haven’t seen it yourself, you should take a look – it could have huge implications for the market this year.