Image Credit: Vecteezy

Key Points

- Amgen reported strong first-quarter earnings and continued its positive 2025 momentum, though the stock has fallen sharply since the results were released.

- Investor sentiment has weakened due to analyst downgrades, elevated net debt, insider selling, and regulatory setbacks.

- Competition is intensifying across key drug categories, with biosimilars and major pharmaceutical rivals pressuring sales while Amgen works to expand in the fast-growing GLP-1 market.

Amgen (AMGN), the pharmaceutical and biotech company behind products like Otezla, Repatha, Enbrel, and Prolia, saw its stock drop roughly 6.5% between April 30 and May 4 despite strong first-quarter 2026 results and the announcement of another $300 million investment in its Puerto Rico biologics facility.

Since reaching its all-time closing high of $388.16 on February 27, Amgen’s stock has declined nearly 17% based on its May 4 closing price of $323.85.

What’s driving the downturn despite Amgen’s solid recent performance?

Amgen Had a Strong 2025 and First Quarter of 2026

Amgen’s sudden stock dip is a bit surprising given its strong 2025 performance and ongoing momentum through the first quarter of 2026.

Amgen’s 2025 highlights included:

- Total revenue of $36.8 billion, a 10% increase from 2024.

- GAAP (“generally accepted accounting principles”) earnings per share (“EPS”) soared 88% year over year, from $7.56 to $14.23; non-GAAP EPS went up 10%, from $19.84 to $21.84.

- GAAP operating income jumped from $7.3 billion to $9.1 billion year over year; non-GAAP operating income increased from $15 billion to $16.2 billion.

- GAAP operating margin grew 3.1 percentage points to 25.8%; non-GAAP operating margin dipped 0.8 percentage points to 46.1%.

Additionally, 14 Amgen products generated more than $1 billion in sales, 18 products achieved record sales, and 13 reached double-digit sales growth.

Amgen’s first-quarter 2026 results maintained the company’s momentum from last year, with revenue increasing 6% year over year to $8.6 billion. GAAP EPS increased by 4%, and non-GAAP EPS jumped 5% year over year.

The company also raised its 2026 revenue outlook to $37.1 billion to $38.5 billion.

GAAP operating income more than doubled from $1.2 billion to $2.7 billion, and GAAP operating margin soared 17.4 percentage points to 32.4%. Amgen also generated $1.5 billion of free cash flow in the first quarter, a 50% year-over-year jump.

Product sales grew 4% in the first quarter, driven by 16 products that registered at least double-digit sales growth.

To accommodate the increasing sales volume of its products – and to cut down on President Donald Trump’s import tariffs – Amgen just invested another $300 million (on top of $650 million the company invested last year) in its manufacturing facilities in Puerto Rico.

Despite all these positive developments, Amgen shares have taken a hit.

The Factors Behind Amgen’s Recent Decline

Amgen stock has been a relatively consistent target for analyst downgrades throughout 2026. Its most recent came on May 4, when Guggenheim lowered its price target for Amgen by $11 to $340 after the company’s earnings call.

Here are a few reasons for Amgen’s recent poor stock performance relative to the company’s first-quarter earnings beat.

Valuation

Amgen stock isn’t necessarily overvalued. In fact, its average price target is around $358, which isn’t far off from its current trading price in the $320 to $330 range. So, an argument could be made that Amgen stock is actually a bit undervalued.

Consider two key factors.

First, at the end of 2026’s first quarter, Amgen had $45.3 billion in net debt. That plays a big (decidedly negative) role in determining the stock’s valuation.

Second, insider trading has recently skewed bearish. In just the past three months, inside shareholders have sold $21.1 million worth of shares. And there’s been no reported buying of shares in that same time frame. While that’s not necessarily a sign of panic, it could reflect a lack of confidence within the company. If nothing else, it raises some red flags.

Clinical Setbacks

Biotech companies will experience their share of failures. It’s just the cost of doing business. Unfortunately, those setbacks can damage a company’s stock price as well as its reputation.

Amgen has dealt with a few clinical setbacks of late.

- During the first quarter, Amgen stopped working on anvumetostat, a cancer drug, after failing efficacy tests.

- The company also shut down adezkibart, a drug to treat Sjögren’s Syndrome, after failed trials.

- Amgen and its partner Kyowa Kirin also halted all trials for autoimmune drug Rocatinlimab because of safety concerns.

But Amgen’s most high-profile regulatory issue involves autoimmune drug Tavneos.

The Food and Drug Administration (“FDA”) recently pointed to “new information that only became known to CDER [the Center for Drug Evaluation and Research] more than three years after approval shows that unblinded study personnel manipulated the results of the pivotal clinical study so the drug looked effective when the original analysis did not support that conclusion.”

In other words, the FDA is essentially accusing Amgen of fudging data to get the drug approved and on the market. That’s not a good look.

Now, the FDA is attempting to have Tavneos approval withdrawn and taken off the market due to concerns that the drug may cause severe liver damage. The side effect was a known risk and was mentioned on the drug’s label. However, the FDA found that eight deaths occurred with patients taking Tavneos, which elevated the agency’s concern.

Increasing Competition

Amgen is facing increasingly stiff competition, not only in certain key markets but also for its flagship products. For example, sales of its reliably profitable Prolia and Xgeva drugs, which help curb bone breakdown, plummeted by 32% year over year during the first quarter of 2026.

Why?

Competition from biosimilar drugs like Jubbonti and Wyost, both made by Sandoz.

And Enbrel, a longtime best-selling autoimmune drug for Amgen, is suffering as well. Enbrel’s full-year revenue plunged 33% in 2025, while year-over-year sales during the first quarter of 2026 fell 37%.

The government’s Medicare Part D redesign was a major factor, but so was market-share competition from frequently advertised drugs like Humira, Skyrizi (both made by Big Pharma rival AbbVie [ABBV]), and Tremfya, made by Janssen Biotech, whose parent company is Johnson & Johnson (JNJ).

Amgen certainly didn’t help itself by showing up late to the GLP-1 obesity drug competition, as rivals like Eli Lilly (LLY) with its Foundayo, Mounjaro, and Zepbound drugs, and Novo Nordisk (NVO) with its Ozempic and Wegovy products have dominated the market.

Amgen is hoping its experimental, long-acting Maritide GLP-1 is a differentiator, as it requires less frequent dosing than typical GLP-1 drugs, which should be very appealing to GLP-1 users.

The drugmaker has plenty of products in its pipeline, such as Maritide, Repatha, Imdelltra, and Tezspire… but so do its competitors.

So, the pressure is on Amgen to offset its late entry into the obesity and diabetes drug markets, as well as the downturn in revenue from its historically profitable drugs.

Amgen is hoping Maritide and its other pipeline drugs are the cure. But it’s a tall order.

Amgen’s Stock Outlook

Yes, Amgen’s stock has been tumbling for the past couple of months. But let’s keep in mind that Amgen is up nearly 20% over the past year and set a new all-time high just weeks ago.

While there are some concerns about the company’s future performance, as I outlined earlier, there’s a lot to like about Amgen’s stock.

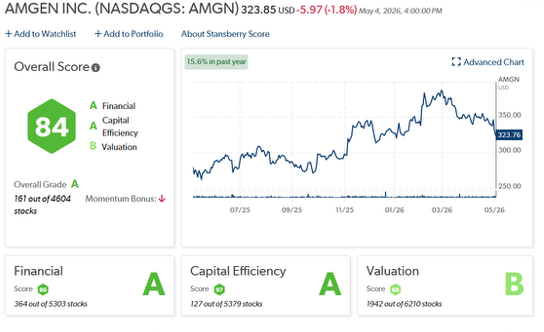

Amgen’s Stansberry Score, a tool that helps determine the quality and long-term value of thousands of stocks, ranks well within the top 200 stocks out of more than 4,600 overall.

Its strong “A” grade is driven by the company’s outstanding financials, as Amgen continues to increase its revenue and operating income. Amgen also receives an “A” for capital efficiency, as the company consistently increases its operating margins, pays capital returns to its shareholders, and owns a stellar 28.6% free cash flow margin over the past five years.

So, what’s the verdict on Amgen?

It’s important to acknowledge the factors behind the company’s recent stock slide. But it’s also worth noting that Amgen has been a highly successful – and profitable – company for more than 45 years.

Amgen continues to develop important drugs, is entering the GLP-1 market, and is expanding its manufacturing footprint.

Most importantly, Amgen keeps making money and generates consistently significant free cash flow that opens opportunities for expansion and acquisitions. And that’s what matters for investors.

Regards,

David Engle

Editor’s note: Since the start of 2025, more than 700 stocks have doubled. That’s incredible. And yet, True Wealth senior analyst Brett Eversole says we’re not done. His latest research shows a new pattern forming that could send today’s record-high market soaring even higher.

He calls this pattern the “Melt Up Tsunami.” And he has identified at least six stocks that could benefit, including one stock he says could not just double, but triple. He names that stock in his new presentation, found here.

Recent Articles

KKR, Blackstone, and Brookfield Bet $16 Billion on Kuwait’s Oil Pipeline Deal

Bloom Energy’s Recent Mega Sell-Off Could Be a Buying Opportunity After a Blowout Earnings Report