Pity the average California commuter. One of the state’s towns – Brentwood, in the Bay Area – is home to the longest average car commute time in the nation, and residents have long paid high gas taxes for that questionable privilege.

Now, residents face another problem:

California gas prices could hit $7.50 this summer.

In fact, some areas will see gas prices as high as $10, especially in remote pockets like Mono County and other isolated regions where fuel delivery is expensive, and drivers have few choices. A typical SUV could cost over $200 to fill up.

Many retail investors have already jumped on the obvious trades – buying up oil funds and filling up their tanks. Bettors on prediction markets like Kalshi are giving a one-third chance that WTI Crude prices will hit $150 later this year.

However, I believe there’s a more useful question for investors. Rather than focus on spot oil (which changes by the day), people should ask: where does the longer-term shortage show up first, and which stocks does the market still misunderstand?

That second-order thinking changes the math. Here, I’d like to outline one company perfectly positioned to benefit… one that’s on the sidelines… and one company to sell immediately that’s about to get squeezed…

Let’s take a look.

Why Are California Gas Prices Spiking?

To get started, let’s consider the three key reasons California gas prices are rising so quickly.

First, crude oil prices have surged on the Iran conflict and tanker disruption fears. Crude futures currently sit above $100 per barrel, making gasoline more expensive. If the U.S.-Iran conflict extends through the summer driving season, Americans in general could see fuel prices rise into the $5 range.

Second, California has a structural supply problem. The state depends on a smaller set of refineries and its laws mandate a special gasoline blend that is specifically made for that market. Supplies have tightened after Valero Energy Corp. (VLO) shut down its Benicia refinery in April, cutting the number of gasoline-producing refineries to seven. This follows a separate 2025 shutdown of a Phillips 66 (PSX) refinery in Los Angeles.

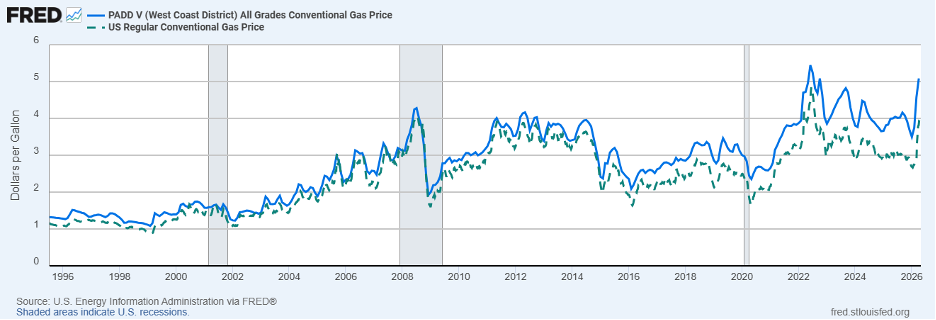

Most importantly, California sits in an “energy island” called PADD 5 (Petroleum Administration for Defense Districts No. 5). There are no major crude pipelines between this West Coast region and the rest of America, so the state has historically relied on imports. Around 70% of its oil came from abroad last year, with the Persian Gulf making up a quarter of that figure. California also imports a significant amount of finished gasoline and blending components from South Korea, Canada and India.

These imports are now drying up. The final regular deliveries from the Far East should arrive in the next two weeks, and replacement shipments from American Gulf ports will not make up the full difference. Trucks and rail will provide even less relief, since the PADD 5 region has too few terminals to handle that type of cargo.

That means we should expect prices to rise past $7.50 by July, assuming a roughly 18% decrease in gasoline supply and a 6% decline in short-run demand. Until more Californians can give up driving, the PADD 5 premium is about to widen further.

Source: St. Louis Federal Reserve

Buy: Why PBF Energy Stock Will Profit

PBF Energy (PBF) is the cleanest way to own California gasoline scarcity.

The company operates two major California refineries: Torrance in Southern California and Martinez in Northern California. Its Torrance refinery can process about 166,000 barrels of crude oil per day, and its Martinez location handled 157,000 per day before halting production in 2025 after a fire. Management announced last week repairs are now almost entirely complete, and that Martinez is now back at full planned production.

Together, PBF will generate roughly 3 billion gallons of gasoline this year for California – or almost a quarter of the state’s demand.

That timing is unusually favorable. Valero’s shutdown of its Benicia refinery has tightened the market right as imports are drying up. PBF will go from producing under 10% of California’s gasoline (due to the Martinez shutdown), to almost 25%.

Investors have not yet priced in the full opportunity. Shares of PBF have risen less than 30% since the start of the U.S.-Iran conflict, compared to 35%-plus increases in Texan companies like HF Sinclair Corp (DINO) and APA Corp (APA). The Martinez refinery shutdown “hid” a vast production facility from trading algorithms focused on 2025 data, and the Benicia shutdown has not yet shown up in current financial data.

That suggests markets are unprepared for the massive surge in West Coast crack spreads – the gap between crude oil and gasoline prices. There are far fewer players in California gasoline today compared to three months ago. And given that shares of PBF trade for roughly 9X forward earnings, there’s plenty of upside as California faces a “new normal” of refinery demand.

Hold: Devon Energy Stock Can Ride This Out

In March, I recommended that readers buy Devon Energy (DVN), a high-quality Permian shale play benefiting from the opening of new Texas-to-Louisiana pipelines. The Matterhorn Express Pipeline came online the year before, and the Blackcomb Pipeline was set to open within the next several months. As I explained:

Both pipelines give Devon’s stranded gas access to liquefied natural gas (LNG) compression plants on the Gulf Coast. These supplies are hitting the market right as the world needs them most. Roughly 20% of global liquefied natural gas (LNG) is now blocked in the Strait of Hormuz.

Devon’s stock has risen 17% since then, an excellent two-month return. And I’m continuing to hold on for three reasons:

- Operations. Devon remains an extremely profitable firm and has a breakeven price below $45 per barrel.

- Costs. Its recent merger with Coterra Energy transforms it from a regional behemoth into a firm with a cost basis that rivals Diamondback Energy (FANG).

- Exports. Its new links to the U.S. Gulf Coast turn this domestic firm into an export powerhouse.

I expect another double-digit return by the time the U.S.-Iran conflict gets resolved.

Now, the Texas-based company has less exposure to the Californian energy market compared to pure plays like PBF Energy. Devon has no major pipelines into the PADD 5 region, nor refineries that can turn crude oil into the gasoline that the Golden State mandates. That’s why it’s a “hold” rather than a “buy” due to California gas prices.

Nevertheless, there’s still some upside.

On April 24, President Trump extended the waiver of the Jones Act for another 90 days, which allows foreign ships to transport cargo between American ports.

This is crucial for companies like Devon, which need these foreign ships to move products from the Gulf Coast to the West Coast. Most Jones Act-eligible tankers are already tied up with regular business of running oil between Alaska, Hawaii, Louisiana and Florida. So, there’s little spare capacity for a new route from Louisiana to California – probably five to ten ships at the most.

The waiver now allows Devon to move oil from the PADD 3 region (where it is not needed) to PADD 5 (where it is).

Devon’s original investment thesis also remains compelling. America is turning into a major energy exporter, and for 9X forward earnings, DVN is an attractive play on that trend. It remains a “hold” in my books.

Sell: Alaska Air Stock Is Flying Into Trouble

Alaska Air (ALK) is a well-run airline that’s heading into a nightmarish situation. The company bought Hawaiian Airlines in 2024, and the combined firm is now unusually exposed to high jet fuel prices on the West Coast.

Alaska’s primary hub is at the Seattle-Tacoma International Airport and 78% of its traffic is on the West Coast. That means fuel is generally bought at West Coast prices – an unattractive proposition today. The Hawaiian merger added exposure to Singapore jet fuel prices as well, which have risen faster than any other major market outside of the Middle East.

Worst of all, the company abandoned its hedging program in 2025, meaning that it has not locked in jet fuel prices for 2026. This fact is buried in its 100-page annual report (bolding for emphasis):

Alaska and Hawaiian previously used crude oil call options to hedge fuel expense. Alaska’s fuel hedge program was suspended in 2023 and all remaining positions were settled in 2025. Hawaiian’s fuel hedge program was suspended in the beginning of 2025, with all remaining positions settled later in the year. No hedge positions remain open as of December 31, 2025.

That means fuel costs – which already made up 21% of operating expenses in 2025 – are about to turn into a near-catastrophe. Analysts are expecting a 38% increase in fuel expenses this year, flipping ALK’s earnings per share negative to -$0.80, down from $2.44 the prior year. I expect the figure to be even worse, considering that jet fuel prices are already 105% higher than they were at the start of the year.

Meanwhile, competitors like Delta Air Lines Inc. (DAL) hedge themselves against these threats. In fact, Delta even bought its own refinery in 2012 to protect itself from rising jet fuel prices and widening crack spreads. Its Monroe refinery now covers 80% of the airline’s domestic jet fuel needs, putting the national carrier in a position to undercut Alaska Air and gain market share.

In addition, Alaska could face lower consumer demand. When California drivers are paying $6 to $8 at the pump, discretionary travel becomes easier to postpone. That is not my primary bear case, but it adds pressure at the wrong time.

The Bottom Line: How to Play the California Gas Price Crisis

California is unlikely to run out of gasoline everywhere. Its seven remaining refineries continue to produce gasoline, and high prices are already trimming demand. There’s no reason to get hysterical quite yet.

That is why my call is far more specific than betting on oil:

- Buy PBF Energy because it owns the California refining assets that can profit from scarcity.

- Hold Devon Energy because the March 10 thesis worked, and the company can still ride elevated energy prices.

- Sell Alaska Air because West Coast jet-fuel exposure, limited hedges and a high earnings multiple leave too little margin for error.

These investments are far better positioned to address California’s longer-term fuel issues than the crowded oil trades retail investors are pursuing.

What would make me wrong? A fast normalization in Pacific imports, broad California fuel-specification relief, smooth refinery operations across the state and a rapid decline in crude and jet-fuel prices. If all those happen, PBF loses some of its scarcity premium, DVN becomes more range-bound and Alaska gets breathing room.

Until then, the playbook is straightforward: own the barrel that California needs, keep the energy producer that already worked, and stay far away from the airline that has to buy the expensive fuel.

Editor’s Note: Elon Musk reinvented the auto industry, sparked a new era of space exploration, and built the world’s largest satellite network. But his new initiative — “Project Apex” — could become the crown jewel of his career. And, like Tesla, it could make early investors incredibly wealthy. Click here for the details…