Key Points

- Merger speculation with United Airlines was quickly dismissed by American Airlines as regulators and political figures signaled strong skepticism toward a possible tie-up, citing antitrust concerns and potential harm to consumers.

- American Airlines continues to lag rivals financially and operationally, with weaker profits, thinner margins, higher debt, and labor unrest in 2025.

- The airline is attempting a strategic turnaround by shifting back toward premium travel offerings and operational improvements, but key risks remain for investors.

American Airlines (AAL), the world’s largest airline by seat capacity, wasted no time dismissing the rumors of a possible merger with “Big Four” competitor United Airlines (UAL) once they began spreading on April 17.

The merger speculation began as details of a private February meeting between United CEO Scott Kirby and President Donald Trump emerged.

During the White House meeting, Kirby allegedly floated the idea of a merger with American, even though the combined company would own roughly 40% of the domestic share. That massive market share would most certainly raise the eyebrows of regulators.

American issued a terse statement in response to the merger rumor, saying:

American Airlines is not engaged with or interested in any discussions regarding a merger with United Airlines. While changes in the broader airline marketplace may be necessary, a combination with United would be negative for competition and for consumers, and therefore inconsistent with our understanding of the [Trump] Administration’s philosophy toward the industry and principles of antitrust law. Our focus will remain on executing on our strategic objectives and positioning American to win for the long term.

U.S. Transportation Secretary Sean Duffy, however, hasn’t exactly thrown cold water on the idea. As Duffy stated earlier in April, “President Trump, he loves to see big deals happen.” And he added that there’s “room for mergers in the aviation industry.”

But the likelihood of this type of merger legally coming to fruition is slim to none. Even Duffy acknowledged the difficulty with this type of merger.

“If there was a merger between some of the larger airlines, they’re going to have to peel off some of their assets,” Duffy said. “We don’t want to have this massive infrastructure with one airline in America. Again, that will affect pricing in the long run, because it would be a lack of competition.”

Trump himself said on April 21 that he doesn’t “mind mergers,” but when it comes to a potential deal between American and United, he said, “I don’t like it.”

Why American Airlines Stock Slid After Dismissing Merger Talk

American Airlines stock dipped more than 4% between Friday, April 17 and Monday, April 20, upon news that the carrier had no plans to merge with United.

It was an interesting market reaction, as investors appeared optimistic about a possible mega-deal forming – far and away – the world’s largest airline.

Upon hearing the initial rumors, investors priced in the premium they expected this merger would create. That’s why American’s stock price shot up roughly 4% on April 17, when the rumors surfaced.

After American rejected the possibility of a merger, it simply brought the price back down to its previous level.

A Look at American Airlines Major Struggles in 2025

Investors and analysts have concerns over American’s shortcomings – including sagging profits, labor unrest, high cancellation rates, and significant debt.

Although American posted a company-record $54.6 billion in revenue in 2025, a deeper look into its 2025 financials reveals cracks in the foundation.

- American earned $111 million in net income in 2025. Rivals Delta Air Lines (DAL) and United earned $5 billion and more than $3.3 billion, respectively. Even Southwest Airlines (LUV), at $441 million, surpassed American by a wide margin.

- Net profit margins were even worse. American finished at 0.2%, while Delta ended 2025 with a 7.9% net profit margin, United with 5.7%, and Southwest with 1.6%.

- American ended 2025 with $36.5 billion in total debt, which was actually a $2.1 billion improvement over 2024.

- American’s free cash flow (“FCF”) totaled negative $83 million in 2025. For comparison, Delta’s FCF was $4.6 billion, and United’s was $2.7 billion.

American’s problems go well beyond finances, however.

Based on 2025 U.S. Bureau of Transportation Statistics data, American Airlines – despite operating the second-most flights (behind only Delta) – lagged behind most U.S. carriers in several categories:

- American had the third-worst flight on-time percentage (71.03%) among the 10 carriers, ahead of only JetBlue (JBLU) and Frontier (ULCC).

- Not surprisingly, the airline had the second-most delayed flights, behind only Southwest.

- American’s 11,519 cancelled flights were more than 3,500 ahead of the next-closest carrier.

And then there’s the labor issue.

American Airlines CEO Robert Isom has been the target of ire from the pilot and flight-attendant unions.

A significant source of the unrest stems from low profit sharing for the company’s employees. Consider this alarming statistic from American’s pilot union: Near the end of 2025, American Airlines pilots were projected to receive just 0.6% in profit sharing for the year, whereas Delta pilots would receive 10% and United pilots 7.6.

That low profit sharing is a direct result of American’s underperformance, and its workers want answers.

Employees also remain frustrated that American’s crews were stranded at airports during severe winter storms in late January, literally leaving them with nowhere to sleep aside from the airport.

All this unrest culminated in early February, when the flight-attendants’ union released a statement saying that “this level of failure begins at the very top” as it issued a vote of no confidence against Isom.

Would a Mega-Merger With United Even Help American Airlines?

An airline merger the magnitude of the rumored American-United deal has never occurred. But if American and United did join forces, two of the three largest domestic airlines would combine to create a never-before-seen mega-airline that could control roughly 40% of the U.S. market.

With that massive level of domestic share, this proposed mega-carrier would instantly have the pricing power to raise fares. And that would, theoretically, vastly improve American’s (and United’s) bottom line.

But antitrust laws exist to prevent exactly this type of price hike. An American-United merger would remove one of the “Big Four” airlines from the skies, leaving passengers with fewer choices.

From an operational standpoint, merging two large airlines would likely create more problems than it solves. Think about what’s involved in operating an airline every day. Airlines may be the most complex and challenging businesses to operate on the planet.

From servicing the aircraft to sourcing food vendors, there’s a seemingly endless slate of operational tasks involved in simply keeping an airline running. Each airline has its own processes, technologies, and nuances.

Now imagine combining two very large operators. It’s an enormous undertaking that could raise countless logistical and operational issues, at least in the short term. Ultimately, that could result in reputational and financial harm.

A mega-merger, even without the inevitable legal impossibilities, wouldn’t fix the company. American Airlines must do that itself.

MORE: Best Blue-Chip Stocks for 2026: 5 Reliable Market Leaders

How American Airlines Shifted Back to Premium

American Airlines found itself at a crossroads in 2025. Should it continue to operate as usual and hope that, with a few tweaks, success follows? Or was a pivot in strategy necessary?

American wisely chose the latter.

For starters, American needed to treat Delta and United as its primary rivals and chief competition once again.

That hadn’t been the case since about 10 years ago, when American turned its focus to lower-cost carriers like Frontier and Spirit in an ill-advised attempt to compete with them on price.

The problem with that strategy? American Airlines isn’t a lower-cost carrier. It never was. By opting not to invest in an improved premium travel experience to compete with Delta and United, American essentially neglected the flight experience altogether in favor of price.

As a result, American’s aircraft cabins weren’t updated, its service suffered, and its airport experience (lounges, for example) grew stale.

American did manage to earn more revenue than its top two rivals from 2016 through 2022. But, as travelers began prioritizing a premium flying experience over cheap airfare, the carrier saw both Delta and United pass them by. For the past three years (2023 through 2025), American earned less revenue than both of its main competitors.

So, American decided to do something about it.

Last year, the airline announced it was getting back into the premium business. American introduced its new Flagship Suite – which features lie-flat seats, privacy doors, and extra storage – for its long-haul flights. The airline is also refreshing cabins on regional flights and offering amenities such as faster (and free) AT&T Wi-Fi (for members of AAdvantage, American’s loyalty program), Bollinger Champagne service, and Lavazza coffee products.

The pivot is beginning to pay off.

American, during its first-quarter 2026 earnings call on April 23, said:

The company continued to win share in corporate channels during the first quarter, with managed corporate revenue increasing 13% year over year. Additionally, American is focused on increasing premium leisure revenue and improving upsell to higher-margin products. Premium unit revenue continued to outperform the Main Cabin in the first quarter.

The carrier also hopes to see a continued uptick in revenue from loyalty-mile sales through co-branded credit cards. By the time you read this, all Barclays (BCS) American Airlines co-branded cards will have fully transitioned to Citi, which is now the exclusive issuer of American Airlines AAdvantage cards.

American is also investing in improved technology, particularly its mobile app, which will, according to the airline, “give customers real-time solutions all in one place to self-serve their itineraries for a smoother, more autonomous travel experience during irregular operations.”

Operationally, American plans to rebank – or restructure flight schedules at – its largest hub, Dallas Fort Worth International Airport, to increase on-time departures, decrease late arrivals, and reduce overall delays. It’s also rebanking operations at Philadelphia International Airport to increase and improve trans-Atlantic connectivity.

This is all very promising news for American Airlines. The only issue? It’s going to require quite a bit of capital expenditure (“capex”) – the efforts are projected to cost more than $4.5 billion through 2027 – for a company that’s already around $35 billion in debt.

Should Investors Be Bullish on American Airlines?

American is making inroads and investing in the right areas. And the strategy pivot is starting to bear some fruit. So, there’s some evidence that could support a turnaround for the stock, with some caveats.

To start, there’s the company’s record fourth-quarter revenue of $14 billion in 2025… and, as noted earlier, its record $54.6 billion full-year revenue last year.

Yes, American’s debt is significant, but the company did manage to slice $2.1 billion off the books in 2025. And it started 2026 by cutting debt to its lowest level in more than a decade. It may not be much, but it’s a start.

American’s first-quarter 2026 results revealed more reasons to be cautiously optimistic that the company is beginning to turn things around.

- American posted record first-quarter revenue of $13.9 billion, up 10.8% over first-quarter 2025.

- The company had a GAAP (generally accepted accounting principles) net loss of $382 million, a substantial improvement over its first-quarter 2025 net loss of $473 million.

- That led to a loss of $0.58 per diluted share.

- American reported more than $3.4 billion in free cash flow.

- The company finished the first quarter with $34.7 billion in total debt. That’s American’s lowest total debt level since 2015.

- Available seat miles rose 3% year over year.

Moving forward, for the second quarter, American forecasts a year-over-year revenue increase in the $13.5 billion to $16.5 billion range. But the carrier also expects the midpoint of its full-year guidance to stay roughly flat to 2025.

Why? Because American is facing a roughly $4 billion increase in jet fuel costs due to the war in Iran.

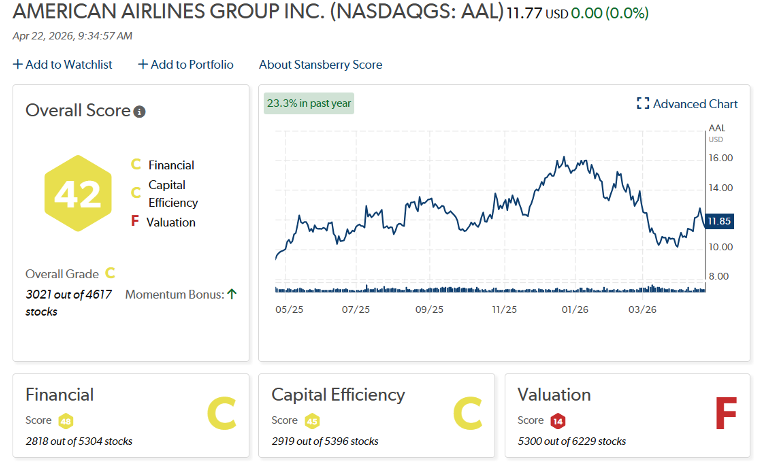

American Airlines’ Stansberry Score, a tool that helps determine the quality and long-term value of thousands of stocks, accurately reflects the company’s current position, with an overall “C” grade. Its financials and capital efficiency are average (“C”), and its valuation is poor.

American’s high (though improving) level of debt, growing fuel expenses, increasing labor costs, lack of profitability compared to its competitors, and operational struggles help explain the “F” grade in valuation.

Hurdles such as rising fuel prices and the potential for further labor strife still linger. And American has a lot of ground to make up if it’s going to catch rivals Delta and United, both of which are still well ahead of American in the premium travel space.

Financially, the carrier’s profits are far behind its competitors’, its stock is down roughly 26% year to date, and it has significant debt to pay off.

These are not problems to be solved overnight. American seems to understand its shortcomings and is actively addressing them. We’ll see, throughout the rest of the year, whether those solutions move the needle.

The airline certainly has its challenges, but it seems to be heading in the right direction. I don’t know that “bullish” is the best descriptor for American right now, but there are definite signs of a turnaround being possible as 2026 continues.

Regards,

David Engle

Editor’s note: One group of Americans is quietly building extraordinary wealth right now, while another is falling further behind with every passing month. Whitney Tilson – the hedge fund legend CNBC called “The Prophet” – says we’ve hit the “Ripping Point,” and the split is accelerating fast. He’s sharing what he believes everyone needs to do immediately (and providing two free stock picks) in this urgent, free presentation.