How long will it take to reopen the Strait of Hormuz?

That’s now the most important question for financial markets right now.

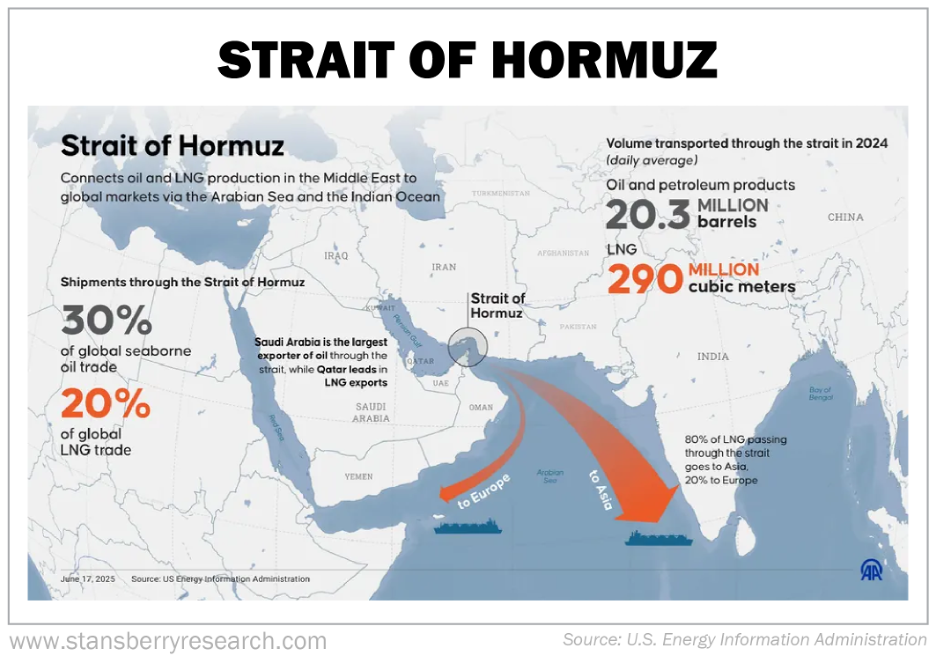

The Strait of Hormuz is a narrow 21-mile-wide waterway between Iran and Oman connecting the Persian Gulf and the Arabian Sea. Roughly 20 million barrels of oil and 290 million cubic meters of liquefied natural gas (“LNG”) pass through the strait each day.

That’s nearly all the crude from OPEC giants like Saudi Arabia, the United Arab Emirates (“UAE”), Kuwait, and Iraq. Plus, a significant amount of liquefied natural gas “LNG” from Qatar.

Let me say from the start that I (Bill McGilton) have no idea how long the Strait of Hormuz will stay closed.

What I can offer in this article are some thoughts on how the closure could affect financial markets and some observations on how to best prepare your portfolio.

For starters, the Strait of Hormuz can stay closed for far longer than most people expect.

On Drones, AI, and Asymmetric Warfare

Military technology has changed significantly since the start of the Russia-Ukraine war. As former U.S. Navy SEAL officer and Blackwater founder Erik Prince put it during a Hillsdale College seminar on “Artificial Intelligence” on February 2, 2025, the Russia-Ukraine war “has massively accelerated warfare in a way that I think it’s the greatest advancement, or it’s the greatest swing in the pendulum, really since Genghis Khan put stirrups on horses” back in the 1200s.

What Prince is referring to is the combination of drones and electronic warfare, used in conjunction with real-time surveillance and artificial intelligence.

Drones have changed the nature of conflict – allowing for cheap precision technology to stand up against far more powerful and expensive legacy technologies – like tanks and ships.

Ukraine has used these technologies effectively for the past four years to limit Russia’s advances and to bottle up the Russian Black Sea Fleet in Novorossiysk – while under consistent heavy bombardment from missiles and Shahed-type drones from Russia.

These same technological advances create the potential for a long conflict in Iran… especially given Iran’s huge territory, at about one-sixth the size of the U.S., its rugged terrain, and a population of 93 million people.

So maybe the U.S. and Israel bomb Iran into submission, or the country fragments under the pressure… Maybe the parties figure out a way to negotiate and find an off-ramp… Or maybe the conflict continues and the Strait of Hormuz stays closed or partially closed for an extended period. I have no way to know.

But what I do know is if the conflict continues, we’re looking at serious repercussions across financial markets.

What a Closed Strait Means for Energy Markets

Not all 20 million barrels of oil crossing the strait are set to be lost to markets. There are some alternative pipeline routes. And the Paris-based International Energy Agency (“IEA”) announced on March 11 that it is prepared to release 400 million barrels of oil into the market as an emergency measure – including 172 million barrels from the U.S. Strategic Petroleum Reserve (“SPR”).

That may sound like a lot, but it’s a proverbial drop in the bucket. By the IEA’s own estimate, global oil consumption was approximately 104 million barrels per day in 2025. Put another way, that historic release wouldn’t even sustain a week’s worth of global demand.

Coupled with demand destruction from higher prices and limited crossings, the IEA expects oil supply to drop by a net 8 million barrels per day (around 8% of world oil demand).

That’s an enormous figure. It means, for instance, that Australia will completely run out of fuel by June 1 – as it’s heavily dependent on refined fuel from Singapore, South Korea, and Japan – which in turn get their crude oil from the Middle East via the Strait of Hormuz.

About three weeks into the war, we’re now looking at Brent crude (the international standard) trading at $111 per barrel. Brent was trading at around $72.50 on February 27 – the day before the conflict started. The longer the war continues… the higher oil prices will soar.

Keep in mind, the current oil price is after the IEA already said it would release 400 million barrels of oil – which represents one-third of the 1.2 million total governmental reserves of all IEA countries. It’s the largest release in history, yet it has only been a speedbump for higher oil prices.

Investment bank Goldman Sachs warned that Brent crude could exceed the 2008 peak of $148 a barrel if the strait stays mostly closed through March.

Already, we’re looking at higher oil prices pushing inflation higher and pressuring growth. That’s because oil is the lifeblood of the global economy. Higher oil prices act like a tax on consumers and ripple through the entire economy.

And I’m not just talking about higher fuel prices raising transportation costs – which is a huge factor. Crude oil is a raw ingredient in things like plastics, fertilizers, and even some medicines. And it’s often used for electricity generation.

Higher fuel prices raise the cost of everything – causing everything from food to airplane tickets to get more expensive. Consumers end up with less disposable income – hurting the economy.

With all that said, what should investors be thinking about right now?

A Few Assets to Keep on Your Radar

Now’s the time to hold onto your energy investments. You’ll have time to take profits once the war is over – when there’s more clarity. You surely won’t sell at the top with this strategy. But it’s likely to be more profitable overall to wait and let things play out.

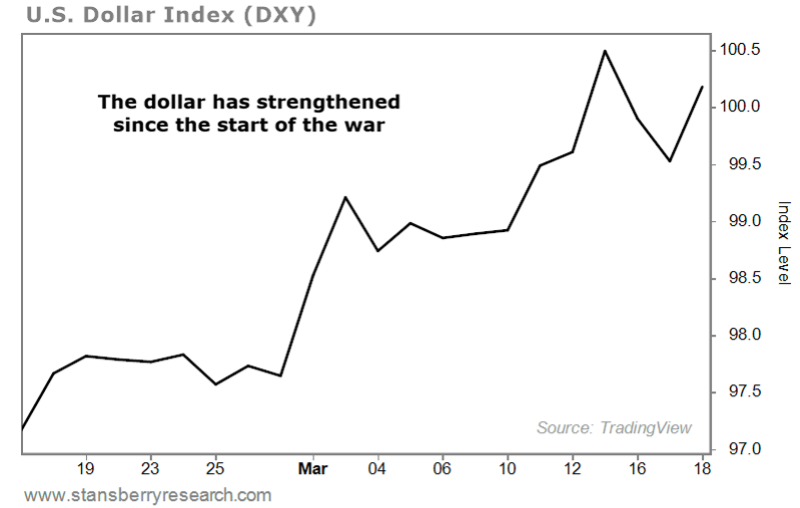

For now, investors are rushing into the U.S. dollar. The U.S. Dollar Index (“DXY”), which tracks the dollar against a basket of currencies like the euro and yen, is up 2% since the start of the war. Two percent might not sound like much. But for currencies – which are typically measured in “bips” – it’s a massive move in such a short period of time.

The U.S. dollar has also outperformed gold and silver – which are down 13% and 26% respectively since the start of the war.

In the near term, the dollar is likely to continue to outperform. Gold and silver are signaling that the economy will likely slow – and thus the stock market will likely sell off – if oil through the Strait of Hormuz continues to be choked off.

But don’t expect the sell-off in gold and silver to last…

War is known to have a scissors effect… It typically increases the money supply – while constricting the supply of goods (like oil).

We’re seeing this starting to play out already. Estimates suggest that the Iran war costs on average $1.4 billion per day. The longer the war goes on, the more that cost matters. It suggests a cost of around $40 billion per month or almost $500 billion over the course of a year. The Department of War just asked for an additional $200 billion to fund the war effort.

The large spending packages come while the world economy is slowing due to higher energy prices and U.S. debt is rising rapidly.

The U.S. national debt just crossed $39 trillion – after hitting the $38 trillion threshold in late October. U.S. debt is now sitting at 122% of gross domestic product (“GDP”). An extended war will only accelerate the debt growth – which is already on autopilot higher.

The problem is that if economic growth slows (because of higher oil prices), tax receipts will fall, and the debt-to-GDP ratio will rise – making the fiscal situation even worse.

The last time we saw a similar situation was just after World War II – when debt peaked at 121% of GDP in 1946. Back then, the Federal Reserve helped keep short-term Treasury yields at 0.375% for five years and long-term bond yields at 2.5% for nine years.

This allowed the government to issue bonds at artificially low rates, reducing large interest expenses. It was done on the backs of bondholders who were paid everything they were entitled to on a nominal basis… except when the bonds matured, they were paid back with dollars with less purchasing power.

Today will be no different…

Expect a variation of the same playbook this time around: soft yield-curve control (policies to cap interest rates) – combined with quantitative easing (“QE”) – when the Fed grows its balance sheet and injects liquidity into the economy. Or we’ll see some form of “not QE” under a different name but with the same effect.

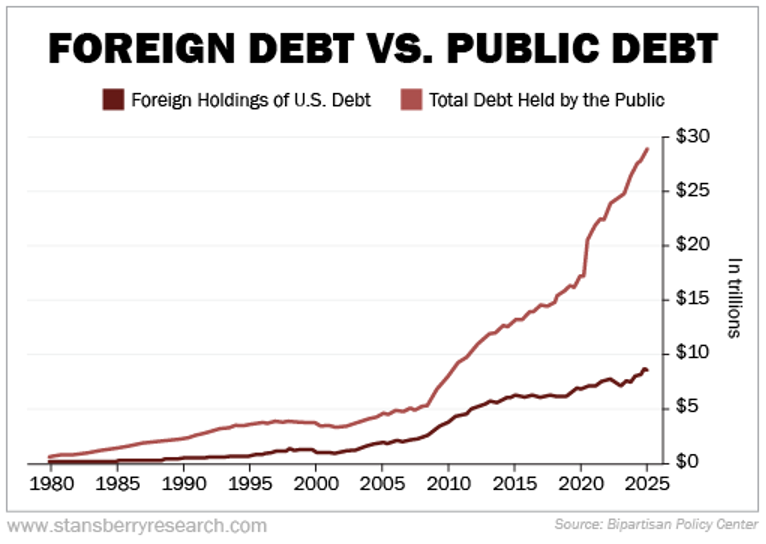

No one in government is interested in austerity. So, the only answer is to inject more liquidity into the financial system. And foreign central banks no longer have the capacity to soak up the massive amounts of debt issuance.

It’s not that foreign central banks have stopped buying U.S. Treasurys… It’s that they can’t keep up with the pace of supply that has flooded the market since QE began in 2008.

Take a look…

And the yield on U.S. Treasurys isn’t high enough to entice central banks to buy them at the same levels as in the past. They know high U.S. debt levels are set to metastasize into higher rates of inflation – which eats into real returns.

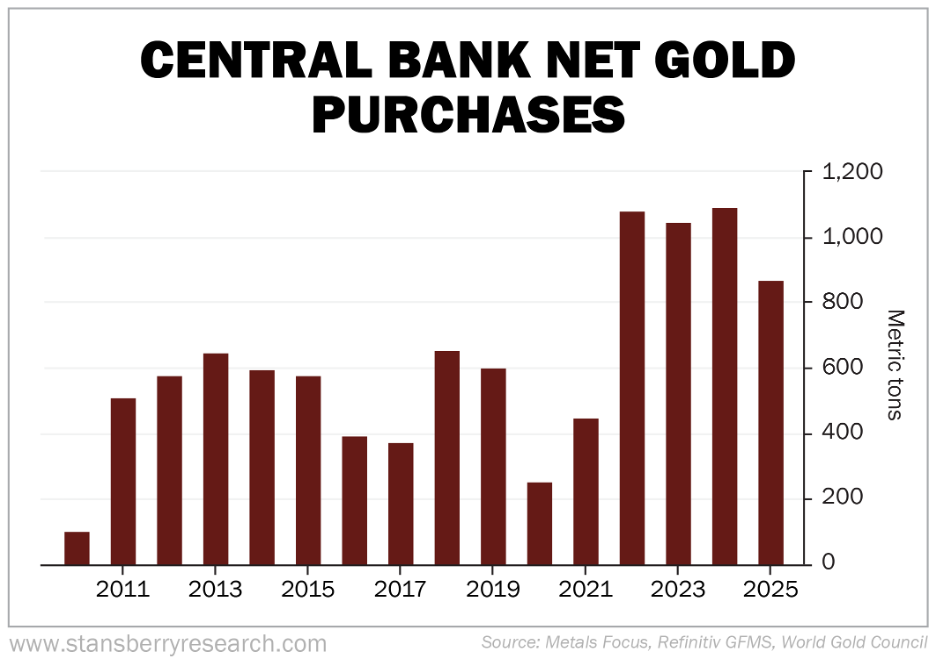

Instead, central banks around the world are responding by buying gold…

They’ve been net buyers of gold for 15 consecutive years, purchasing more than 1,000 metric tons (“MT”) in 2022, 2023, and 2024. According to the World Gold Council (“WGC”), they purchased 863 MT last year. Take a look…

A WGC survey last June found that roughly 95% of global central banks expect to increase gold reserves over the next 12 months. None of the respondents anticipated a decline in their gold reserves.

Altogether, most central banks remain in gold “buy mode.” That will drive prices higher in the coming years.

Of course, it’s not just central banks turning to gold as a store of value. Investors are joining in, too. Investment demand exploded to 2,175 MT last year, 84% higher than in 2024.

Gold prices today are nowhere near high enough to unlock new production or recycling…

Despite higher gold prices in 2025, mine production was up less than 1% to 3,672 MT. And recycling was only up 3% to 1,404 MT.

It’s going to take much higher prices to bring new mines on line. And even if the commodity price does rise high enough to justify new supply, it won’t happen overnight. These are huge commitments that take decades to build. And people aren’t incentivized to recycle enough gold today to keep a lid on prices.

As for silver, the market has been out of balance since 2019, with persistent annual supply shortfalls. According to precious metals consulting firm Metals Focus, demand exceeded supply by 211 million ounces in 2024 and by an estimated 188 million ounces in 2025.

Min production has been stuck at an average of 830 million ounces per year since 2017, with recycling averaging around 190 million ounces per year since 2021.

Silver is mostly used in industry (which means a lot of it disappears off the market because it’s uneconomic to recycle). It’s typically a byproduct of mining other metals like gold and copper, meaning it’s rarely mined on its own. Yet, demand is picking up…

We need more silver for high-tech industries and renewables. That’s why the U.S. Geological Survey (“USGS”) designated silver as a critical mineral in November 2025.

Bottom line – wait for the Strait of Hormuz to reopen before offloading any quality oil positions. Trim back on stocks dependent on discretionary consumer spending. And use this opportunity to buy gold and silver… Both are going a lot higher.

Regards,

William McGilton

Editor’s Note: This year, one of the world’s biggest oil producers poured $1 billion into a startup that could KILL the oil industry.

This obscure startup is the front-runner in a technology that could generate virtually limitless energy.

Bill Gates says that it “could be as transformative as the invention of the steam engine before the Industrial Revolution.” (Details here.)

No wonder Microsoft recently inked a massive deal to generate electricity from this breakthrough power source.

Even the firms that are most vulnerable to its disruptive potential are piling into it… Oil supermajors ExxonMobil, Chevron, Eni, and Shell are staking billions of dollars in a technology that – according to Live Science – could “make oil obsolete.”

And now – thanks to a little-known “backdoor” into this technology – it’s your turn.