Back in eighth-grade geography, I remember staring at a map of the Persian Gulf and thinking,

“Is that it?”

The Strait of Hormuz looked like a minor crease in the paper. The waterway separating Iran from the Arabian Peninsula is barely 21 miles wide at its narrowest point. Easy to miss. Easy to forget on a pop quiz.

That’s the thing about chokepoints. They look small until they aren’t.

Markets are now learning that same lesson. Twenty percent of global oil output once flowed through that strait, and war in Iran has turned this small bottleneck into a global flashpoint.

Most investors are playing it the obvious way. They’re piling into crude futures and large-cap energy names, watching the WTI price ticker like it’s a scoreboard.

But oil prices are unpredictable, as Monday’s reversal proved – a near-30% crash from intraday highs as diplomatic signals suddenly shifted. You might as well make money from coin flipping.

That’s why professional investors usually look for better odds. These are bets that should do well, no matter where oil goes. Now, no one wants to see global conflict, but to help protect your portfolios admist the war, I found three stocks that could help ride out the volatility

The first is a shale play that’s benefiting from high oil prices. They’re suddenly able to ship natural gas from the American heartland to places abroad that need it. The second is Europe. And the third is a fertilizer crisis that has barely registered on Wall Street’s radar, even as the signals are already flashing.

Let’s take a look now.

Oil Stock to Buy No. 1: Devon Energy Corp. (DVN)

Devon Energy (DVN) is at the forefront of America’s shale revolution. Senior InvestorPlace Analyst Eric Fry added shares to Fry’s Investment Report (subscription required) in 2024 when prices were still in the $30s — they’re at $45 now — and the recent jump in global oil prices now gives Devon another leg of growth.

Here’s the fundamental case.

Devon is one of America’s largest shale producers. The firm merged with rival Coterra Energy in early 2026 and now produces 1.6 million barrels of oil equivalent per day – enough to fill up 4.5 million cars with gasoline.

Devon is also a relatively efficient producer, especially compared to global averages. The company’s breakeven oil price sits at just $44 per barrel and could reach the low-$40 range on post-merger cost savings. Even with oil prices pulling back, Devon is still printing money and can still lock in $70-plus prices in the futures market.

It’s a guaranteed profit either way.

Most importantly, Devon isn’t just an oil story. It’s a gas story, too.

For years, the Delaware Basin in West Texas has had a stranded gas problem. Production from oil wells generates enormous volumes of natural gas, and pipeline capacity wasn’t enough to move it out. That meant gas was flared. Trucked. Sold at Waha Hub prices so deeply discounted they were negative at times (i.e., producers paid people to take the gas away). Devon was sitting on a resource it could barely monetize.

The Delaware Basin’s gas was like a brilliant athlete stuck in class. The skills were there. The path to the NFL was there. But he was simply in the wrong place.

That’s now changing.

In 2025, the Matterhorn Express Pipeline came online. The 580-mile system now moves 2.5 billion cubic feet per day of natural gas from the Waha Hub toward the coast. A second route, the Blackcomb Pipeline, is set to open within the next several months. Together, these systems are transforming the Delaware Basin. Both pipelines give Devon’s stranded gas access to liquefied natural gas (LNG) compression plants on the Gulf Coast. These supplies are hitting the market right as the world needs them most. Roughly 20% of global liquified natural gas (LNG) is now blocked in the Strait of Hormuz.

That makes DVN a strong buy at its current mid-$40 price. While the world is watching the stuck assets in the Strait of Hormuz, investors really should be focused on the ones that are flowing out of America instead.

Oil Stock to Buy No. 2: Equinor ASA (EQNR)

The gas opportunity extends to Europe as well.

In 1972, the Norwegian parliament founded Statoil to manage the country’s oil and gas assets. Massive oil reserves had been discovered in the North Sea, and the government wanted to make sure it was properly managed.

We now know Statoil as Equinor (EQNR) – a publicly traded company that’s become Europe’s primary oil and gas producer. The company produces 2.1 million barrels of oil equivalent daily and is by far Europe’s largest supplier of piped gas.

Shares surged in the months following Russia’s invasion of Ukraine in 2022. Piped gas from Russia dried up, and Equinor soon became the dominant game in town. EQNR shares rose past $40 by that summer (up from $20 the year before), and management boosted its dividend for four years.

It was a windfall for early investors. And a similar story is now playing out again.

Last week, Qatar was forced to shut liquefied natural gas production after missile attacks from Iran began targeting energy infrastructure. The country makes up 20% of global LNG exports, and prices in the Far East and Europe have already spiked. What’s worse, sources say it would take at least a month to return to normal production volumes… which might not happen for a while. After all, LNG tankers are essentially floating bombs.

That’s had an immediate impact on European gas prices, which must compete with Asian buyers for supply. Dutch TTF Natural Gas Futures have spiked from $30 before the conflict to $45… and could rise further as remaining winter stocks are depleted.

Meanwhile, EQNR shares sit at a valuation that doesn’t reflect its situation. Prices continue to trade almost 20% below their 2022 peaks.

That gives Equinor a solid double-digit upside from here.

I must also note that the company is astonishingly well run. Production grew 3.4% to record levels in 2025, and management expects another 3% increase in 2026 with breakeven levels of $40/barrel equivalent. This represents a 25% return of $65/barrel of oil.

Though its upside is far lower than Devon’s, Equinor is still a solid buy at current prices. The company is facing another windfall and has shown itself highly capable of managing them in the past.

Fertilizer Stock to Buy No. 3: The Mosaic Company (MOS)

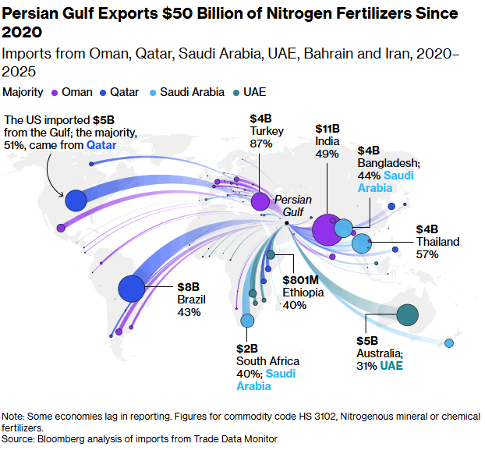

The Middle East isn’t just an oil and gas hub. It’s also a critical supplier of nitrogen-based fertilizers. Exports have essentially shut down with the closure of the Hormuz Strait.

The most direct beneficiaries have already seen the news reflected in share prices. CF Industries Holdings, Inc (CF) has surged over 40% since the start of the year, while Nutrien Ltd (NTR) is up 20%. These companies are major nitrogen-based fertilizer makers and compete most directly with Middle Eastern imports.

However, one company has yet to rise:

Mosaic (MOS).

The Florida-based firm is North America’s largest producer of potash and phosphate. These two fertilizers are slightly different from the nitrogen-based type that the Gulf exports, and so, the stock has barely risen since January.

In theory, the three types of fertilizer have little in common. You need nitrogen, potash and phosphate to make things grow, and these are not interchangeable. (Gardeners will know these by the “NPK” acronym seen on fertilizer bottles.) So, at first glance it makes sense that CF and NTR are up, while MOS is not.

However, different crops need different amounts of these three fertilizers. Corn requires more nitrogen, while soybeans rely on far less. So, high prices in one type of nutrient can often cause shifts in what farmers plant.

That’s why shares of Mosaic should eventually rally. Rising nitrogen fertilizer costs are already beginning to cause chatter about more soybean planting, and one researcher at the University of Arkansas System Division of Agriculture is already predicting 3.5 million acres of soybeans this year – a level not seen since 2017.

MOS shares are also relatively cheap. The stock trades at just half of long-term, mid-cycle valuations, and so even a return to normalcy gives shares a 2X upside. A windfall from higher fertilizer prices will only add to that.

In other words, when CF hits a 52-week high and Mosaic hasn’t yet moved, that’s not a coincidence to ignore. That’s a signal to buy.

The Bottom Line

The Strait of Hormuz crisis is real. The oil trade is obvious. And obvious trades are usually already priced in the market. Monday’s oil reversal proved that point. Devon and Equinor, with breakeven costs under $45, remain profitable even as crude pulls back. That’s the whole thesis.

That means investors usually need to look one or two steps ahead to get in at the right price.

That’s particularly important in today’s market. Futures prices are now in “backwardation,” so obvious oil-based trades like the United States Oil Fund LP (USO) can fall in price, even if oil stays above $90. These funds are forced to buy high-priced spot oil and lose money every time contracts roll forward to a lower price. (It’s a bit technical, but that’s why USO has lost 65% since 2014 despite oil prices finishing roughly flat.)

Meanwhile, oil and gas producers like Devon and Equinor can lock in profits at current prices because their breakeven costs are so low. Mosaic benefits as farmers switch to crops that are less reliant on nitrogen.

And so, be sure to think outside the box when it comes to oil stocks. All of Wall Street’s attention is now on that 21-mile-wide strip between Iran and Oman, and every word the White House is saying about it. Take that opportunity to hedge with companies beyond their focus.

Editor’s Note: Elon Musk reinvented the auto industry, sparked a new era of space exploration, and built the world’s largest satellite network. But his new initiative — “Project Apex” — could become the crown jewel of his career. And, like Tesla, it could make early investors incredibly wealthy. See below for the details…