Investors may be watching the wrong Elon Musk project…

We’ve written about how all eyes are focused on the SpaceX IPO, likely to be the biggest in history… The artificial intelligence (“AI”) supercomputer that xAI built faster than anyone thought possible… And even Tesla (TSLA), which is worth more than the next 10 automakers combined and could soon merge with SpaceX.

Luke Lango says none of those are the most important story to focus on right now, with the biggest profit potential for investors.

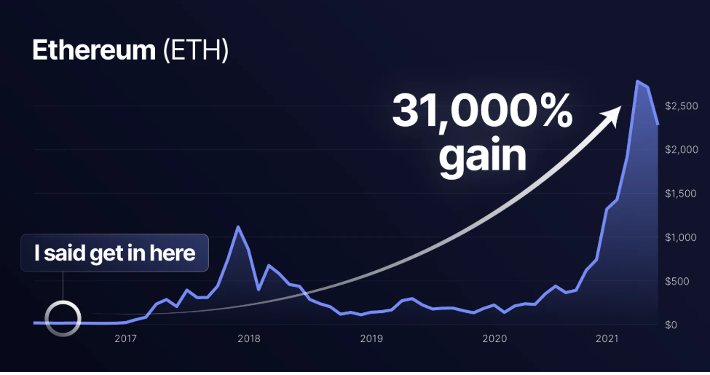

Luke is the lead technology analyst at InvestorPlace, a top independent financial publisher. He’s been ranked the No. 1 stock picker in the world, out of more than 15,000 financial experts. And the last time he spotted this type of story, he showed investors how to make up to 31,000% gains over the next decade.

Already, the Bank of Elon has secured money-transmitter licenses in almost every U.S. state… inked a partnership with Visa (V), the world’s largest payment network… and is benefitting from executive orders pushing the federal government toward digital payments.

As Musk puts it, he intends the Bank of Elon to be “the place where all the money is – the central source of all monetary transactions.”

That’s a potential $480 trillion market… and could result in the biggest change to banking in America in more than 50 years.

And it’s why Luke believes the payoff could ultimately dwarf the profits investors have made on Tesla or even the upcoming SpaceX IPO.

Or read on as we dive into why Luke is so interested in this big story…

Table of Contents

Elon’s 27-Year Mission to Reinvent How Money Moves

Luke Lango’s specialty is finding the next disruptive technology story before Wall Street wakes up to it.

And today, while Wall Street is focused on the SpaceX IPO, Luke thinks there’s even more upside in Musk’s next move… fulfilling an idea that the richest man in the world has been talking about since 1999.

Back then, a 28-year-old Elon Musk had just sold his first company, an Internet directory called Zip2. He walked away with roughly $22 million… And poured nearly all of it into a single idea, that he called X.com.

Biographer Walter Isaacson, who shadowed Musk for two years, described it like this in his book, Elon Musk:

His concept for X.com was grand. It would be a one-stop everything-store for all financial needs: banking, digital purchases, checking, credit cards, investments, and loans. Transactions would be handled instantly, with no waiting for payments to clear. His insight was that money is simply an entry into a database, and he wanted to devise a way that all transactions were securely recorded in real time. “If you fix all the reasons why a consumer would take money out of the system,” he says, “then it will be the place where all the money is, and that would make it a multitrillion-dollar company.”

Within a few months, the company had several hundred thousand users. But it was locked in a costly battle for market share with a separate startup called Confinity, founded by Peter Thiel and Max Levchin, that was building its own peer-to-peer payment product.

In March 2000, the two companies merged under the X.com name, with Musk becoming chief executive.

Then came what Isaacson and others have described as one of the nastiest coups in Silicon Valley history. While Musk was on his honeymoon in Australia, he was forced out as CEO… with Thiel and his allies taking control of the board and renaming the company PayPal (PYPL).

“I was pretty angry at first,” Musk told Isaacson. “I had thoughts of assassination running through my head. But eventually I realized that it was good I got cooped. Otherwise I’d still be slaving away at PayPal… Of course, if I had stayed, PayPal would be a trillion-dollar company.”

PayPal got acquired by eBay (EBAY) in 2002 for $1.5 billion. Musk’s stake netted him around $250 million… which he would later use to become the largest shareholder of electric-car maker Tesla and fund SpaceX.

But Musk never let go of his original X.com vision.

Over the next couple of decades, he tucked the idea away while he built the rest of his empire… from Tesla to SolarCity, the Boring Company to Neuralink, and SpaceX to xAI.

Musk saw his opening when he bought social network Twitter in 2022.

Most headlines focused on the chaos around the acquisition… from the $44 billion paid to Musk’s disdain for “politically correct” content moderation. But they largely missed Musk’s vision. As Isaacson wrote:

By the time he started buying its shares, Musk saw Twitter, whose name he likewise felt was too niche and precious, as a way to fulfill his original concept. “Twitter could become what X.com should have been,” he told me that April, “and we can help save free speech in the process.”

Luke, too, has written about Musk’s real vision for Twitter at Yahoo Finance…

Musk didn’t buy Twitter because he wanted to own a social media company. He bought Twitter as a distribution layer, with a user base of hundreds of millions of people already using the platform daily…

Musk didn’t just build a product. He built the regulatory infrastructure to go with it. In fact, as he’s said: “If done right, X would be half of the global financial system.”

And sure enough, within months, Musk had renamed Twitter to X. He hinted publicly at his plan to integrate banking and payments. Then he started building the legal and regulatory infrastructure that would make it possible…

Last year, X announced a partnership with Visa, with Fortune magazine noting that it was a step toward turning X into an “everything app”…

X Money represented the tightest pairing of social media and money seen in the U.S. market. It’s a common pairing in other global markets – Tencent’s WeChat represents something of a model for the service.

Visa sees the development as a step forward in making the digital economy more accessible.

X has also been quietly acquiring money-transmitter licenses, state by state. There is no federal money-transmitter license in the United States, so any company that wants to move money has to get authorized separately in every state. The company has secured licenses in 46 U.S. states and D.C., with four states still to go.

And of course, the federal government has given Musk’s project a massive tailwind with two separate executive orders…

Shortly after his election, President Donald Trump inked Executive Order 14178, which set the framework for the federal regulation of digital assets and prohibited a central bank digital currency.

A few months later, he signed Executive Order 14247, which required the Treasury Department to stop issuing paper checks by September 30, 2025. From that point onward, every federal disbursement – from tax refunds, Social Security payments, vendor checks, and even intragovernmental transfers – had to move to electronic methods like direct deposit, debit cards, and digital wallets.

Both orders push the entire federal payment system in a direction that benefits private digital wallets, like what Musk is building at X Money. And Musk, of course, ran the Department of Government Efficiency for much of this period.

That brings us to today… While most of the financial world watches the SpaceX IPO, Luke is focused on the live, public rollout of X Money. As Luke put it in his exclusive interview (read the transcript here):

Tesla has arguably made more regular folks rich than any other company in recent history. It created a whole army of “Teslanaires” — people who turned small stakes into vast fortunes entirely by backing Elon’s company…

And yet… even Elon says his next venture could be many, many times bigger.

What X Money Actually Is

Musk wants a platform that can be your wallet, your bank, your brokerage, and your identification – all in one place…

1. Payments. The payment layer is the most basic part of X Money, and it’s what most reporters have focused on so far.

Similar to Venmo or Zelle, X Money has launched peer-to-peer transfers powered by Visa Direct. Users can send money to anyone instantly, and deposits and withdrawals are connected to a traditional bank account.

If Musk can get 10% to 20% of the nearly 600 million active X users to start using X Money for payments, it would immediately make the app a major player in line with its competitors… For example, Zelle boasts about 100 million active users, Venmo has roughly 90 million active users, and Cash App comes in with around 60 million users.

2. Banking. The banking layer goes further… X Money is offering an FDIC-insured checking account through Cross River Bank, a fintech-friendly chartered bank that already powers embedded finance for companies like Stripe and Affirm (AFRM).

Users can set up direct deposit to fund the account and receive a metal Visa debit card with up to 3% cashback and zero foreign transaction fees.

In addition, the yield on balances is where things start to look unusual. Beta participants have reported earning up to 6% APY on their X Money balances.

For comparison, the national average savings rate at U.S. banks sits below 0.6%. So a customer with $50,000 sitting in their X Money account would earn around $3,000 a year, versus roughly $300 at a typical bank.

That kind of yield is likely to attract some attention, especially since right now there doesn’t appear to be a maximum amount that X Money will pay that 6% yield, though, of course, funds are federally protected only up to the standard $250,000 FDIC limit per depositor…

3. Investing. The investing layer hasn’t launched yet, but Musk has been explicit about where it’s headed.

This will ultimately enable users to buy stocks directly from inside the X app. Musk has previously added “Smart Cashtags” to X feeds that allow a user to click a ticker symbol to load up a stock chart and see the latest discussion about the stock.

The closet analog here is probably Robinhood Markets (HOOD) and Coinbase (COIN), but neither has the user base or the social context that X already has.

4. Identity. Finally, the idea of an app for your financial identity is something that doesn’t get much attention… but will likely be increasingly important in the new world of AI and deepfakes.

We’ll have to see what develops here, but the potential will be interesting to watch. As venture capital investor Chamath Palihapitiya noted:

Your identity on X becomes a crucial financial asset. The distribution of your identity becomes a huge asset that others will underwrite. Investing will then include building a following and posting good, interesting, engaging and useful content.

Why does this one-stop financial app matter for investors?

Because the comparable example anywhere in the world is China’s WeChat. As Luke put it when examining why X Money could be far bigger than PayPal ever was:

And lest you think this is science fiction, just look to China. WeChat – which is also called “The Everything App” – launched its banking features in 2013. Within a few years, nearly 1 billion people were using that app to pay for groceries, invest in the market, split restaurant bills, and send money to family. Mobile payments now account for over 80% of all transactions in China. Tencent, WeChat’s parent company, rewarded investors with a 20x return when mobile banking took off.

X Money is the American version of that story. Except Elon Musk has significantly more users, significantly more political tailwind, and significantly more audacity.

So as X Money rolls out across the U.S., the question is: How can an investor profit from this opportunity?

When Disruptive Technology Meets Money

History is full of examples of what happens when a new, disruptive technology collides with the financial system.

Every time it happens, a new class of financial winners emerges.

Let’s go back to the 1800s, as Samuel Morse’s telegraph network started threading its way across the American landscape. Soon, telegraph lines connected major cities, allowing information to travel at the speed of light for the first time in human history.

It didn’t take long for someone to figure out that the same wires could carry money.

Beginning in February 1871, Western Union (WU) launched its first wire-transfer service… allowing customers to send money between New York, Chicago, and Boston. Soon after, it was named one of the original handful of stocks included on the Dow Jones Transportation Index.

Western Union would dominate the wire-transfer business for nearly a century… and became a giant of the financial world.

The same thing happened with the rise of “plastic” in the 1950s…

Ralph E. Schneider was a lawyer with a client who complained about dining at a restaurant, then finding he didn’t have enough cash in his wallet. So Ralph called up a few restaurants with the idea of a “credit card” that would allow diners to eat now and pay later.

Ralph turned the “Diners’ Club” into the world’s first independent credit-card company. And soon, his net worth surpassed $10 million, placing him firmly into the ranks of newly minted millionaires.

American Express (AXP) followed soon after. Visa and Mastercard (MA), originally bank-owned card networks, came in the 1950s and 1960s.

Within a few decades, plastic money was everywhere. American Express stock has climbed roughly 10,000% over the decades. Visa has delivered closer to 2,000% gains since its IPO, while Mastercard, which went public in 2006, has risen about 14,000%.

Each of these companies became one of the most powerful financial institutions in the world… handing early investors significant profits. And Luke believes X Money is going to play out for similar massive gains.

More recently, PayPal made sending money as easy as sending a message. Its product caught fire on eBay, where users were looking for a way to pay strangers for purchases.

The company first went public in 2002 at $13 a share… was bought out by eBay… then returned to public markets a decade ago and soared as high as $310.

And of course, PayPal’s success spawned an entire generation of digital-payment fintech companies like Block (XYZ), Venmo, Stripe, Klarna (KLAR), Wise (WISE)… each built on the basic insight that the Internet could move money faster and cheaper than the old banking system.

Each time, the companies that combined the new technology with the financial system created wealth for their early investors.

That’s happening again today with X Money as it benefits from a convergence of social media, smartphones, AI, and financial services. X Money is the first attempt in the U.S. to combine all these technologies into a single, unified app.

Luke isn’t the only one making this case…

The Bank for International Settlements (“BIS”), the central bank of central banks, published a 2021 research note arguing that social media platforms with deep user data are particularly well positioned to disrupt traditional banking.

Big techs have the potential to compete at scale and become dominant players. They already enjoy economies of scale and scope and network effects in their core markets. By adding financial services to their ecosystems, on their own or using [Banking-as-a-Service], they can leverage these economies to compete with traditional providers and fintechs. They also have the clout and deep pockets to navigate complex regulations and build parallel infrastructures and closed-loop systems, which could solidify their role as gatekeepers to the consumer (and their relevant data) in the financial sector.

The BIS went on to add that the bundling of services together is likely to set off a feedback loop “where big tech ecosystems become more valuable to users. This begets new users, higher user engagement, and more user data.”

JPMorgan Chase (JPM) CEO Jamie Dimon was even more blunt, warning his executives that the bank should be “scared shitless” of the competitive threat from fintech firms.

That’s why Luke recently wrote a new special report, titled “How to Make 1,000% From the Bank of Elon,” where he identified the 19 public companies that are most critical to X Money’s rollout, organized into three distinct tiers based on how they plug into the system.

Most important, Luke details which of these companies are immediate buys today… and which are better treated as watch list candidates. A few select quotes from the report:

- “As X evolves into a full financial platform – not just payments, but investing, transfers, and potentially crypto – it will need a trusted partner to handle those functions behind the scenes. [Financial Partner No. 2] is one of the few companies positioned to do that.”

- “Every time the Bank of Elon uses AI – to scan for fraud, process transactions, or analyze data – it runs through systems like this. And those systems require a lot of computing power, which means more [AI Integrator No. 1] chips.”

- “As the Bank of Elon takes on the responsibilities of a regulated financial institution, its cybersecurity spending is likely to increase significantly. [Software Backbone No. 2] is one of the primary companies positioned to capture that demand.”

Luke says the recommended companies in this report have the hallmarks of the biggest winners he’s ever recommended… And looking at Luke’s long-term track record… the average return of every portfolio recommendation he’s ever issued since inception is an incredible 102%.

Luke has a special $49 introductory offer for new subscribers… along with a 90-day money-back guarantee. If his work doesn’t fit your investing style, no problem – you can cancel online or via phone and receive a full refund.

What Is InvestorPlace?

InvestorPlace is one of America’s longest-standing independent financial research firms.

Founded in 1973, the company started by offering investment advice to self-directed investors at a time when Wall Street firms gatekept most useful research.

Today, InvestorPlace produces detailed research and recommendations for retail investors, financial advisors, and money managers around the world. Its analyst team includes some of the better known stock analysts in the independent-research industry.

InvestorPlace’s business model is straightforward. It publishes original research and sells it directly to subscribers… That means it doesn’t accept fees from the companies it covers. It doesn’t run investment-banking deals. And it doesn’t take commissions on trades.

Its only customers are its subscribers.

Over the decades, InvestorPlace analysts have made a number of well-timed calls…

- In the 1980s, analysts at the company predicted the personal-computer boom and helped subscribers position for it.

- In the 1990s, they spotted Internet stocks early… and they also sounded the alarm when those same stocks became dangerously overvalued ahead of the dot-com collapse.

- And InvestorPlace analysts’ advice to buy stocks aggressively in early 2009 – near the worst of the financial crisis – set up their subscribers for one of the longest bull markets in history.

More recently, InvestorPlace experts have been at the forefront of writing about AI, electric vehicles, the space economy, biotech, and digital assets.

InvestorPlace’s analysts have been featured in major publications including Barron’s, Time, and the Wall Street Journal, and on networks like Bloomberg, CNN, CNBC, and Fox Business.

Their goal is to provide the “Three Es”… to enrich, educate, and entertain their hundreds of thousands of readers.

Who Is Luke Lango?

Luke Lango is the lead technology and cryptocurrency analyst at InvestorPlace.

While studying economics at one of the world’s top technology universities, the California Institute of Technology, he became obsessed with a simple idea: that math could predict things most people wrote off as random.

First, Luke cofounded Scoutables, a fintech startup that used advanced quantitative models to do something the rest of the industry couldn’t – forecast the injury risk of professional athletes before it ever showed up on the field.

From there, he headed to Silicon Valley and kept building. He helped launch and fund a string of startups… including a social-discovery company backed by legendary angel investor Bill Gross, a sports-analytics firm he cofounded with a former Major League Baseball general manager, and an equity research group that connected tech founders directly with the early-stage investors hunting for them.

Each step taught him that the biggest opportunities aren’t obvious at first… much like the X Money opportunity today as Wall Street shifts its focus to the SpaceX IPO.

And his results are exceptional…

In 2020, he was ranked No. 1 out of 15,123 financial experts on independent industry website TipRanks.

And his track record is filled with the decade’s biggest winners… such as Microsoft (+1,000%), Advanced Micro Devices (+8,000%), Netflix (+1,200%), Axon Enterprise (+3,200%), Shopify (+1,400%), Tesla (+3,500%), Nvidia (+5,000%), Strategy (+2,100%), AST SpaceMobile (+1,000%), Rocket Lab (+1,300%), IonQ (+1,400%), and Palantir Technologies (+1,100%).

Today, more than 250,000 readers worldwide follow Luke’s market research, seeking his insight on how technology can reshape industries and build wealth.

How Investors Can Capture These Potential Profits

Elon Musk, arguably the most successful man in the world, has masterminded some of the most extraordinary stock market stories in recent memory.

He’s pulled off the impossible more than once.

And he’s made regular Main Street investors richer than they ever thought possible.

- Like Jason DeBolt, an engineer who put $19,000 into Tesla… and watched it snowball into a nearly $12 million fortune.

- Or Scott Tisdale, who bought 4,000 shares in Tesla… and made $2.8 million.

- And SpaceX’s looming IPO is set to mint more new billionaires than any liquidity event in history.

Now, Elon’s doing it again… with an idea he’s been working toward for 27 years that could radically reshape the entire $480 trillion financial system.

X Money is in beta testing now. The federal regulatory environment has fully turned toward digital payments and digital assets. Nearly all state licenses are secured. And the potential user base is in the hundreds of millions.

Luke says this is the biggest story in the market today… and it’s being almost totally overlooked.

The last time he made this kind of call, in April 2016, his recommendation of Ethereum soared more than 31,000% in the years ahead.

As he said in his interview (transcript here):

That turns every $1,000 staked into more than $300,000.

In other words…

I’ve ridden a trend like this before, for massive gains.

Now I think Elon is spawning a megatrend that’ll deliver even bigger gains.

That’s why you should buy the stocks in the report I’ve prepared for you.

But you’ll need to subscribe to get access to the recommendations that he thinks have far more upside than SpaceX. You can go straight to the order form for Innovation Investor, without watching a long video, by clicking here.