Many of the most popular stocks trading today are also some of the most volatile ones in the markets. Artificial intelligence (“AI”), energy, fintech, and even some of the “Magnificent Seven” stocks can take investors on a pretty bumpy ride. That’s why blue-chip stocks can be so valuable in an investor’s long-term portfolio.

Blue-chip stocks may not offer the highest of highs like some of the aforementioned stocks. But they typically won’t drag investors to the lowest of lows either. Blue chips are important core stocks to hold, especially during times of market uncertainty.

Top Blue-Chip Stocks to Invest In

The stable performance and strong balance sheets that come with many blue-chip stocks provide a calming change of pace in 2026 amid an environment full of AI-driven headlines and wild uncertainty within the oil markets.

Most blue chips pay regular dividends, offering a measure of stability and consistency over the long term. That’s particularly appealing for income-focused investors.

The identifiable traits of a blue-chip stock include:

- Large market capitalizations, often exceeding $10 billion

- Global brand recognition

- Long history of profitability

- Steady earnings growth

- Generally reliable dividend payments

Perhaps the most important characteristic of a blue-chip stock, however, is its consistency. These stocks are typically far less volatile than small-cap stocks, growth-oriented companies, and the broader market. In other words, blue chips are portfolio anchors that investors can rely on.

Here’s a list of the best blue-chip stocks for investors to consider for their portfolios. Note the solid dividend yields and forward price-to-earnings (P/E) ratios of each large-cap company.

| Ticker | Company | Sector | Market Cap | Dividend Yield (Est.) at Market Close on April 9, 2026 | Forward P/E at Market Close on April 9, 2026 |

| MSFT | Microsoft | Technology | Mega-Cap | ~0.97% | ~19.64 |

| AAPL | Apple | Technology | Mega-Cap | ~0.41% | ~30.66 |

| JPM | JPMorgan Chase | Financials | Mega-Cap | ~2.02% | ~14.29 |

| PG | Procter & Gamble | Consumer Staples | Mega-Cap | ~2.99% | ~20.08 |

| V | Visa | Financial Technology | Mega-Cap | ~0.89% | ~23.97 |

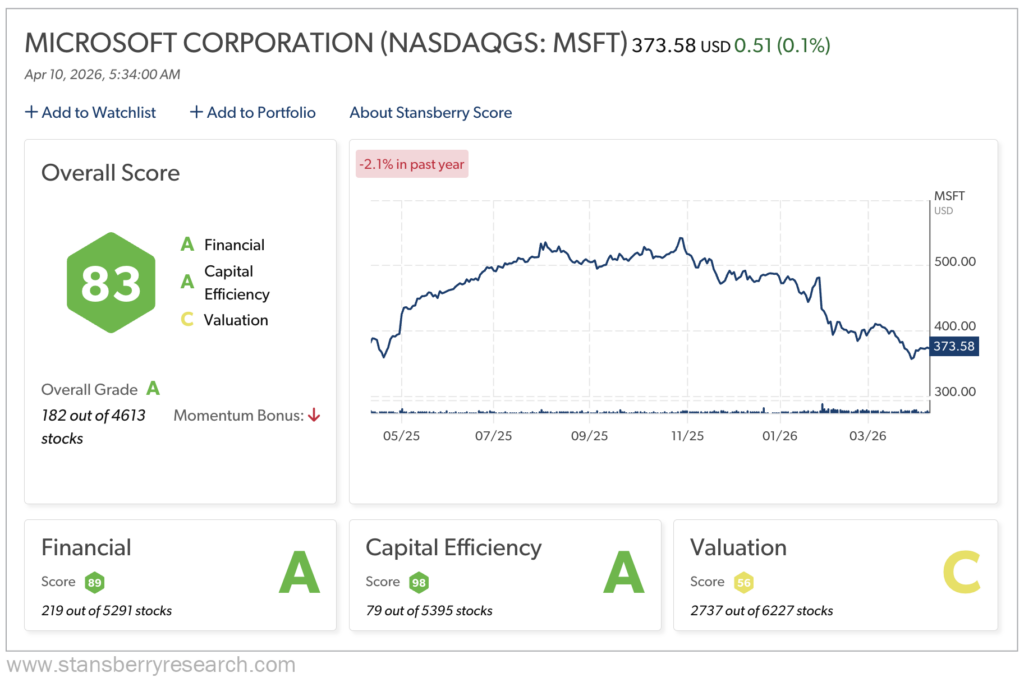

Microsoft (MSFT)

Microsoft has been a blue-chip business for around three decades. And the company continues to raise the bar as a tech leader. While it’s no longer alone atop the tech mountain, Microsoft is a consistent moneymaker and is firmly entrenched among the Magnificent Seven tech stocks.

With a market cap of nearly $2.8 trillion, Microsoft is one of the most valuable companies in the world. The company has been profitable just about every year since it went public in 1986, a testament to its steady and consistent leadership.

And Microsoft has shown no signs of slowing down.

During the second quarter of its 2026 fiscal year, Microsoft reported:

- $81.3 billion revenue, up 17% year over year

- $38.3 billion operating income, up 21% year over year

- $38.5 billion net income on a generally accepted accounting principles (“GAAP”) basis, up 60% year over year, and $30.9 billion net income on a non-GAAP basis, up 23% year over year

- $5.16 diluted earnings per share (“EPS”) on a GAAP basis, up 60% year over year, and $4.14 diluted EPS on a non-GAAP basis, up 24% year over year

The company’s vast ecosystem helps ensure its success year after year. The Windows platform is still dominant in Microsoft’s More Personal Computing, a segment that earned $14.3 billion in the second quarter of fiscal year 2026 (which was actually a slight 3% year-over-year dip).

And its Productivity and Business Processes segment is particularly dominant. It earned $34.1 billion in the second quarter of 2026, a 16% year-over-year increase, driven by its successful Microsoft 365 Commercial package.

Consider some of these 2025 statistics:

- Microsoft 365 had roughly 345 million paid subscribers and about 321 million active users worldwide.

- Microsoft 365 (consumer version) grew its subscriber base by 8%. Cloud revenue also grew 11%.

- Among office-productivity suites, Microsoft 365 held roughly 30% global market share.

- There were more than 400 million active Microsoft Outlook users globally.

While these segments are always steady revenue drivers, it’s the cloud and AI parts of the business where Microsoft is really picking up momentum.

For starters, the company owns a 27% stake in OpenAI, which offers exclusive access to the company’s models, intellectual property, and APIs for products and services until 2032.

Microsoft’s Intelligent Cloud segment, fueled by increasing demand for its Azure cloud platform, earned $32.9 billion in the second quarter of 2026. That’s an impressive 29% year-over-year gain.

And Microsoft Cloud revenue for the quarter was $51.5 billion, the first time it crossed the $50 billion mark, up 26% year over year.

Microsoft 365 Copilot, the company’s AI assistant, experienced record growth by reaching 15 million paid seats – a massive 160% year-over-year increase. And GitHub Copilot subscription rates grew by 75% year over year.

The company’s outlook remains positive. Microsoft is projecting third-quarter 2026 revenue to increase between 15% and 17% to between $80.65 billion and $81.75 billion.

A look at Microsoft’s Stansberry Score, which measures the long-term investment quality of a stock, provides evidence of the company’s strength. MSFT earns an overall “A” grade, ranking well within the top 200 stocks out of roughly 4,600.

MSFT’s strong score comes primarily from its Financials and Capital Efficiency categories, both of which earn “A” grades as well. Its Capital Efficiency score, as of April 9, ranks within the top 80 stocks out of the nearly 5,400 ranked in that category, thanks in part to the company’s 20 consecutive years of increased dividends paid.

Microsoft has proved its worth as a blue-chip tech stock for decades. And its projected future growth signals that the company will remain a blue chip for decades to come, even during challenging periods.

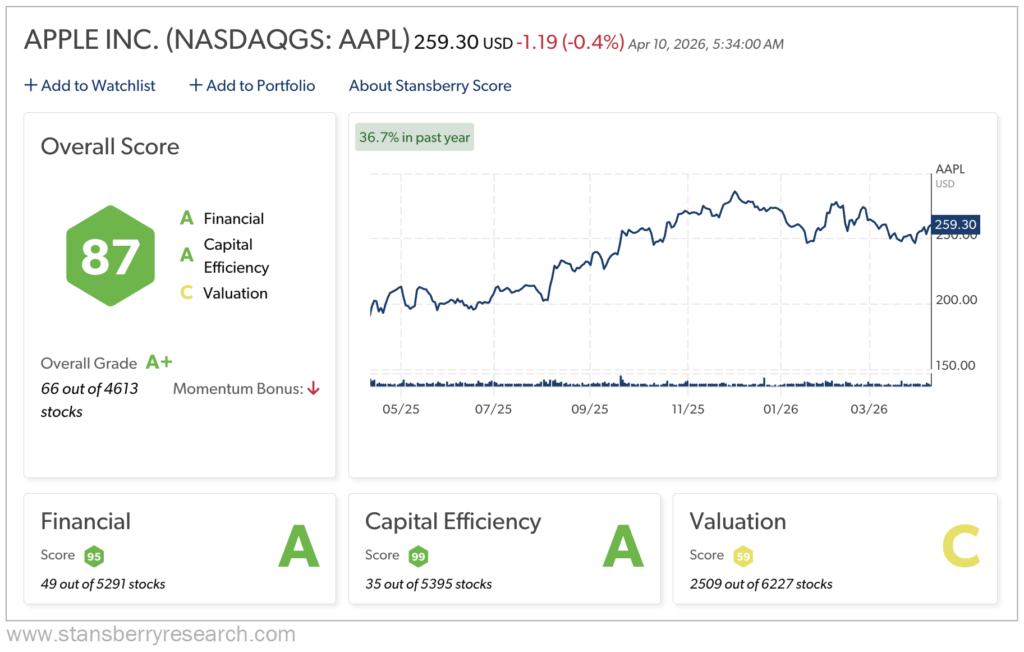

Apple (AAPL)

When it comes to tech, the first name that probably comes to most people’s minds is Apple. And rightfully so.

Also one of the Magnificent Seven tech stocks, Apple is one of the most dominant brand names in the world. Of course, the company earned its stellar reputation as a tech innovator – look no further than the iPhone, iPad, Apple Watch, and MacBook. These products basically set the standard for smartphones, tablets, wearables, and laptops, respectively.

Even going back several years, Apple’s iMac, Macintosh, and Apple II products were ahead of their time and served as a blueprint for personal home and office computing.

But Apple’s brand goes beyond physical products. The company created a proprietary ecosystem – some may even call it a “lifestyle” – for all Apple users through the iCloud platform.

By automatically syncing photos, videos, documents, and device backups, iCloud is the backbone of the Apple ecosystem. Within that environment, users can sync content through the App Store and purchases through Apple Pay.

And its iOS system, with services like iMessage and AirDrop, contributes to the “stickiness” of the Apple world… and that’s often enough to ensure Apple users remain Apple users for life.

Beyond technology, Apple has positioned itself as an entertainment giant. Apple TV has made its imprint among streaming services, enough to take around 9% market share thanks to high-quality original series and movies, such as Ted Lasso, Severance, The Studio, and F1 The Movie. Apple Music, with roughly 95 million users in 2024, is the second-largest music streaming service in the world behind only Spotify.

And Apple Studios, the company’s in-house film and television production company, is a major player in Hollywood. In 2026 alone, Apple Studios earned 15 BAFTA nominations, six Academy Award nominations, and 14 Golden Globe nominations.

Apple is everywhere. Even if you don’t own an Apple device, it’s still an essential piece of 2000s pop culture. And not many brands can claim that.

To the surprise of hardly anyone, 2026 is off to a great start for Apple. Its fiscal year 2026 first-quarter revenue jumped to roughly $143.8 billion from $124.3 billion a year prior. And its gross margin increased to roughly $69.2 billion from $58.3 billion the prior year.

Apple’s first-quarter 2026 net income also improved, landing at roughly $42.1 billion versus around $36.3 billion the year before. Its diluted EPS grew from $2.40 to $2.84 year over year as well.

Looking at Apple’s net sales by category, the iPhone saw a huge jump of roughly $16 billion year over year in first-quarter 2026 to more than $85 billion thanks in large part to the launch of the new iPhone 17.

Though Macs and wearables/home/accessories dipped slightly, iPad and services sales both increased. Overall, net sales rose by nearly $20 billion year over year.

Apple’s Stansberry Score is quite reflective of the company’s performance. AAPL stock earns a rare overall “A+” grade on the back of its stellar Financials (“A,” ranked just within the top 50 out of nearly 5,300 stocks in that category) and Capital Efficiency (“A,” ranked within the top 40 of nearly 5,400 stocks in that category) scores.

Considering its start to 2026, its $3.8 trillion market cap, and the fact that Apple has increased its dividends for 14 straight years, those scores should come as no surprise.

Looking forward, it’s also no shock that Apple has big plans in the pipeline.

Along with exciting new products expected to debut in the next couple years – including the iPhone 18, foldable iPhones, new smart home hubs, updated iPads, the Apple Watch Series 12, AI glasses, upgraded MacBooks, and new AirPods – Apple is aiming to expand the capabilities of Apple Intelligence and Siri, as well as move more of its manufacturing to America.

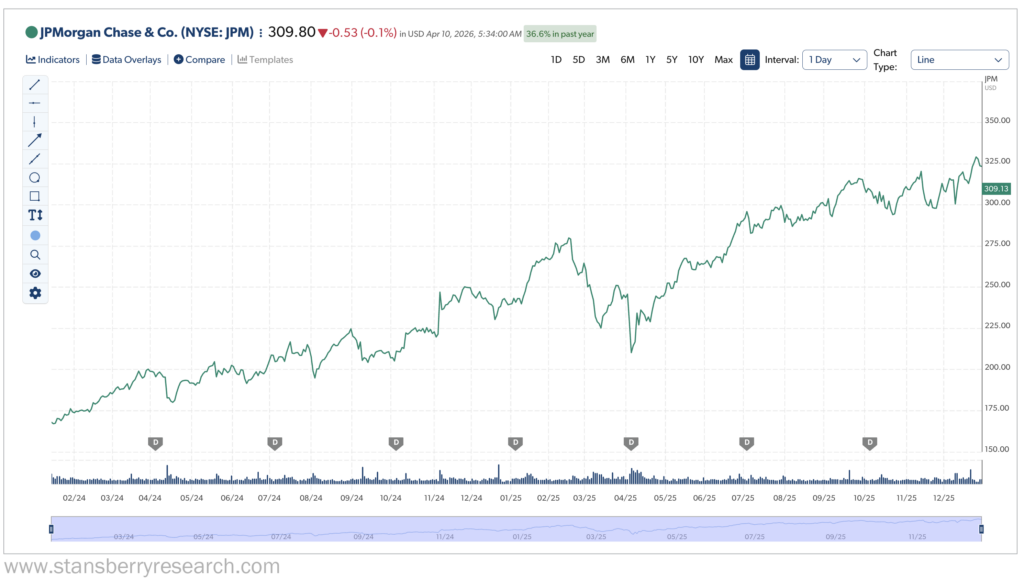

JPMorgan Chase (JPM)

Switching gears to the world of finance, JPMorgan Chase is the largest bank in the world with a roughly $826 billion market cap… more than double that of Bank of America (BAC), the second-largest bank worldwide.

That alone makes JPM a blue-chip company. But so does the fact that JPMorgan Chase holds more than $4.4 trillion in assets, the most of any bank in the world outside of China.

The bank also has history on its side. Established in 1799 as the Manhattan Company, JPMorgan Chase has literally stood the test of time through the absolute worst and best financial climates.

Perhaps most important to JPM’s blue-chip status, however, is its well-known fortress balance sheet. This strategy prioritizes high liquidity, massive capital reserves, and lower risk exposure to ensure the bank can withstand even the worst financial crisis.

The fortress balance sheet ensures the company can continue operating and serving its clients during financial crises. And that inspires much confidence from the bank’s clients, knowing that their assets are safe.

Plus, the liquidity component of this strategy allows JPMorgan Chase to make important acquisitions in any financial environment. For example, when First Republic Bank failed in 2023 (as the Federal Reserve was significantly raising interest rates in 2023 in an attempt to slow inflation), JPMorgan Chase was able to purchase most of the bank’s assets through the Federal Deposit Insurance Corporation (“FDIC”).

A major key to JPMorgan Chase’s continued success is its constant investment in technology. The company says it spends around $18 billion every year (and is expanding its budget to nearly $20 billion in 2026) to continuously innovate on its services and products.

Not surprisingly, roughly 10% of that money goes toward advancing AI, which the company uses extensively for tasks such as underwriting, fraud detection, and even marketing. The bank is also focusing its tech investment on updating its systems, including moving operations to a cloud-based platform.

Financially, JPMorgan Chase had a strong 2025, bringing in roughly $182.4 billion in net revenue and $57 billion in net income.

This was driven by multisegment growth, including an 18% year-over-year increase in assets under management to $4.8 trillion, and 1.7 million new checking accounts and 10.4 million new credit-card accounts in 2025. JPM shares responded accordingly. They started 2025 at roughly $240 and finished the year at just over $322, an increase of more than 34%.

Moving forward, JPMorgan Chase has some exciting plans in store. And they all revolve around its Security and Resiliency Initiative, a 10-year, $1.5 trillion plan aimed at investing in critical (and primarily) American infrastructure such as AI, quantum computing, energy, and supply chains.

Beyond that massive investment, JPMorgan Chase is putting billions toward modernizing its customers’ banking experience. This involves plans to build more than 500 new branches by 2027 in high-growth markets such as Philadelphia, Boston, Charlotte, Minneapolis, and the Washington, D.C. area. Additionally, roughly 1,700 existing locations will undergo renovations.

These modernization efforts all tie back to JPMorgan Chase’s ultimate goal, which JPMorgan Chief Analytics Officer Derek Waldron revealed to CNBC in an exclusive interview: “The broad vision that we’re working towards is one where the JPMorgan Chase of the future is going to be a fully AI-connected enterprise.”

In this AI-centric vision, Waldron and JPMorgan Chase expect that “every employee will have their own personalized AI assistant; every process is powered by AI agents, and every client experience has an AI concierge.”

Of course, this won’t all happen in 2026 – or even 2027. But it’s something to watch down the road as JPMorgan Chase continues to lead the fintech charge.

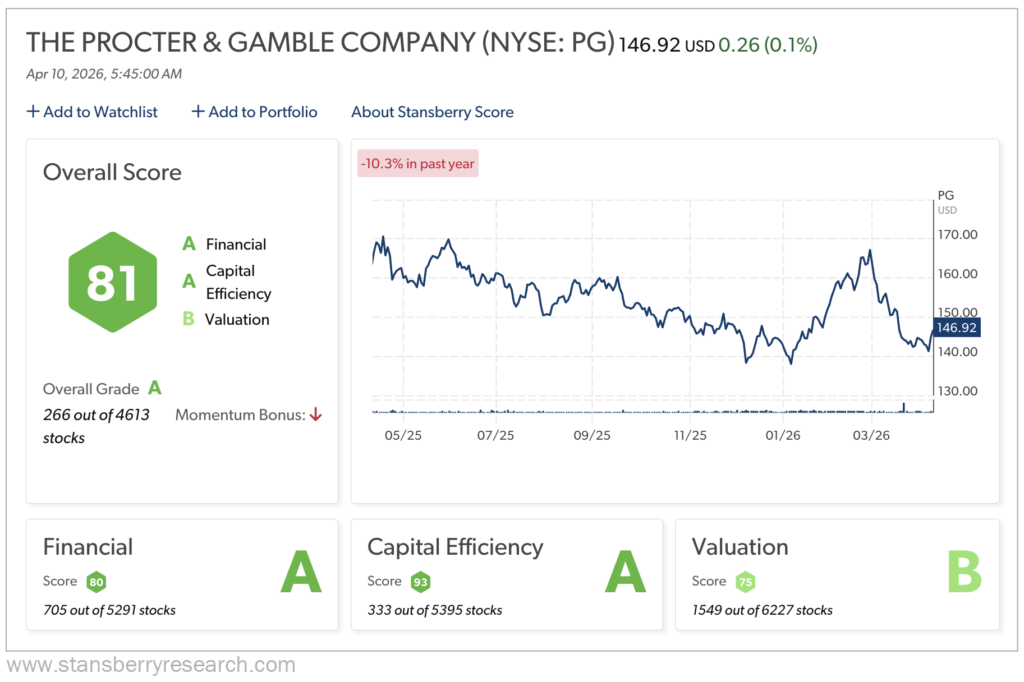

Procter & Gamble (PG)

In February, I wrote an article highlighting the top consumer-staples stocks to watch in 2026. Right at the top of the “blue chip” list was Procter & Gamble, or P&G.

Why? Because you know Procter & Gamble, even if you don’t realize it.

What I mean is, you could look around your home right now and track down at least a half-dozen products from brands owned by P&G: household staples such as Tide detergent, Pampers diapers, and Bounce dryer sheets. There’s also Puffs tissues, Cascade dishwashing detergent, and Crest toothpaste.

This is just a tiny sampling of P&G’s brand portfolio, which is practically peerless.

And you can see why Procter & Gamble has long been considered a blue-chip stock. Its brands make products that we literally can’t live without. The company is nearly recession-proof, since even during the worst financial times, we spend what little we might have on food and personal hygiene items.

Between P&G’s vast brand offerings, its resilience to any economic conditions, and its stature as the No. 1 manufacturer in the world for 10 straight years (as ranked by the 2024 Advantage Report Global Scorecard), it’s easy to see why P&G is a strong blue-chip stock.

But there’s even more to P&G.

It’s forward-thinking, recognized by Fortune as one of America’s Most Innovative Companies. It has plenty of sway, named by Timeas one of its 100 Most Influential Companies of 2025. And it’s universally respected, earning a spot on the Fortune list of the World’s Most Admired Companies for 2026.

And, cementing its status as a top blue-chip stock, P&G has long been known as a Dividend King, increasing its dividend payout for 69 straight years. P&G increased its dividend by 5% and returned more than $16 billion in cash to shareowners in 2025 (nearly $10 billion in dividends).

Maybe even more impressive is that 2025 marked the 135th consecutive year that P&G paid a dividend.

The decades of increasing dividend payouts – and the century-plus of dividend payments – show how strong P&G has been through every type of financial climate. And its Stansberry Score reflects a highly respected and resilient company.

Stansberry grades Procter & Gamble as an overall “A,” ranking the company within its top 300 stocks, with an “A” in Financials and Capital Efficiency and a “B” in Valuation.

For 2026, P&G is looking to increase its premium offerings by offering upgraded products within the Pampers, Swiffer, Tide, Olay, Bevel, and Dawn brands.

But the current market may test P&G’s resiliency, as it faces headwinds stemming from roughly $400 million in tariff costs as well as broader economic uncertainty and the threat of inflation from the ongoing war in Iran.

P&G has already lowered its 2026 forecast and is likely to raise prices on some of its products as a result.

Analysts at TD Cowen have already cut the price target for P&G by $14 to $142. Their logic? Companies – including those in the personal-care and household industries – will not be able to absorb the increased oil-related costs from the war without raising prices. And those elevated prices will not drop anytime soon, even if the war ends tomorrow.

Will consumers, already feeling the pinch from high gasoline prices and energy costs, want to shell out even more for P&G products?

For the basics, possibly, though they’ll likely face more competition from in-store brands. For its premium products? That’s a difficult ask.

But P&G has faced headwinds before and typically emerges in solid shape. That’s why it’s on this list.

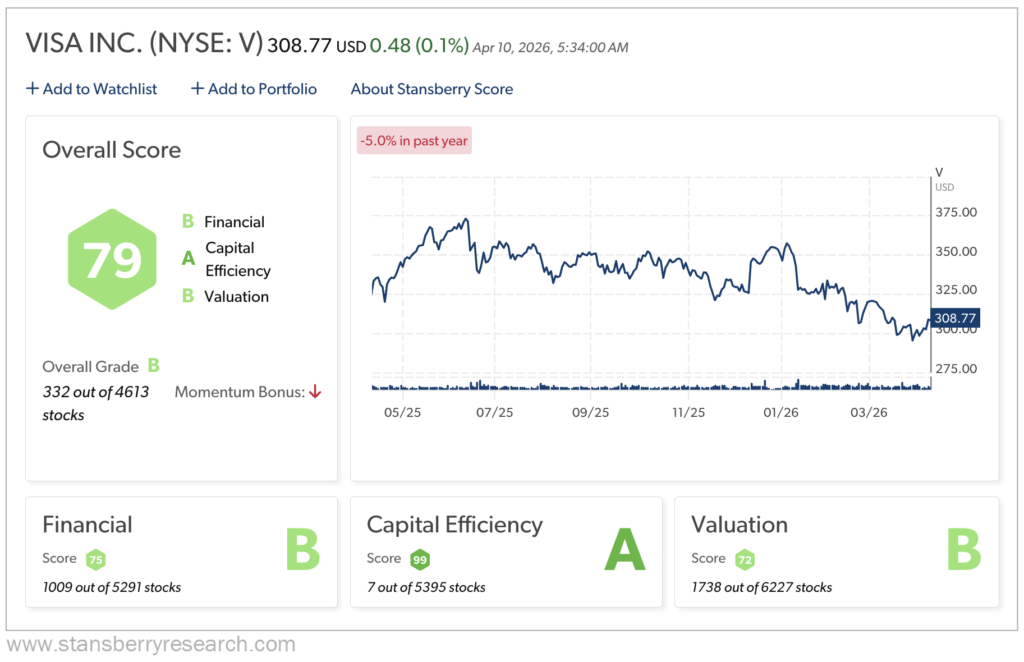

Visa (V)

The world’s second-largest card-payment company (behind only China UnionPay), Visa facilitates electronic funds transfers through digital payments such as credit, debit, and prepaid cards across more than 200 countries and territories.

There’s a strong chance that you have some type of Visa card in your wallet right now. That’s because Visa dominates the American card market. In 2025, Visa handled 31% of debit transactions and 30% of credit transactions on U.S.-issued cards, according to the Nilson Report.

Globally, Visa processed more than 260 billion transactions in 2025, making it the largest payment network in the world.

Visa also offers security services, fraud management, and consulting services. But the company is obviously recognized worldwide for its card payment processing.

It’s also well known for its impressive profit margins, which typically exceed 50%. In fact, over the past three years, Visa’s operating margin has been roughly 67%, and its operating cash flow margin has averaged just under 59% in that same time frame.

How does Visa maintain such high margins on an annual basis?

For one, it operates on a huge-scale economy. Why? Because Visa processes all its transactions – trillions of dollars’ worth – through VisaNet, its proprietary electronic payment network, which has been in place since 1973.

Since VisaNet has been firmly entrenched for decades, every transaction that passes through it grows Visa’s profit with minimal cost to the company. Considering Visa’s massive transaction volume, it’s bringing a whole lot in without putting a whole lot out.

Plus, Visa is not a bank. The company doesn’t actually issue credit or debit cards, nor does it set interest rates. So, Visa does not feel the burden of credit risk that comes with cardholder debt because it only handles payment processing.

And that greatly helps Visa’s margins.

So, it’s not surprising that Visa is in outstanding financial shape. It earned $40 billion in net revenue in 2025, a year-over-year increase of 11%.

Its EPS continues to impress as well, with a GAAP EPS of $10.20 and a non-GAAP EPS of $11.47, up 14% from 2024. Visa’s EPS has grown at a compound annual growth rate of nearly 18% over the past five years. And it’s projected to keep growing by roughly 13% per year.

All this growth can be at least partially attributed to its payment volume growing 8% in 2025, as well as Visa’s 329 billion processed transactions.

Visa’s Stansberry Score earns a strong “B” grade overall. Its Capital Efficiency score is especially noteworthy, ranking No. 7 out of nearly 5,400 graded stocks in that category.

We already covered the reasons for that stellar mark. But you can add Visa’s free cash flow – which has averaged more than 113% of its net income over the past five years – to the mix as well. The company is basically a cash cow.

And while it still has some years to go before it reaches Dividend Aristocrat status, Visa has increased its dividend for 17 straight years.

The bottom line? Visa is a very reliable income-growth stock.

Visa’s future plans? If you guessed something related to AI, you’re correct. The company is hedging its bets on agentic commerce through its Trusted Agent Protocol. This technology, in Visa’s words, “[ushers] in a new era where AI can search, compare and pay on behalf of consumers.”

Visa is also looking to transition stablecoins (cryptocurrencies backed by fiat currency) from being speculative investments to trusted payment infrastructure for business-to-business and cross-border payments.

And the company is counting on the continuing transition away from cash and toward digital payments. This year, half the world’s consumer payments will be made with card credentials, which is outstanding news for Visa and its investors.

Why Investors Are Prioritizing Blue Chips in 2026

If you were creating a pros and cons list for investing in blue-chip stocks, you’d likely find yourself with far more check marks in the pro column.

For investors who prefer dividend income, defensive growth, and – perhaps above all – stability in their investments in an economic environment of volatility and inflation, blue chips are becoming a priority.

Let’s dig deeper into the key reasons why blue-chip stocks are so appealing to investors.

Safety and reliability

Successful, established companies with strong business models tend to be investor favorites, especially during uncertain markets. Blue-chip stocks are simply less volatile than many other types of stocks.

Beta value is a metric that measures a stock’s volatility compared with the overall market’s volatility. Most blue-chip stocks have a beta under 1.0. That means they’re less volatile than the overall market.

Looking at the companies in the table at the beginning of the essay, Procter & Gamble has an extremely low beta of 0.59. That’s right in line with the State Street Consumer Staples Select Sector SPDR ETF (XLP), which has a 0.52 beta. And it helps explain why many consumer-staples stocks are considered blue chips.

Moving on to Visa… the payment-processing giant has a low beta of 0.61. That’s slightly lower than the financial sector’s beta of 0.70. JPMorgan Chase, on the other hand, has a more elevated 1.15 beta. This is likely due to JPM’s massive operations, which include exposure to rapid growth areas like digital banking as well as the volatility of capital markets.

For comparison, the State Street Financial Select Sector SPDR ETF (XLF), which holds millions of shares of both Visa and JPMorgan Chase, has a beta of 0.96

Microsoft and Apple, as part of the more volatile technology sector, typically have higher beta values than, say, the consumer-staples industry. But its 1.04 and 0.81 beta values, respectively, are still significantly lower than other tech giants like Nvidia (NVDA) at 1.89, Meta Platforms (META) at 1.69, and Oracle (ORCL) at 1.82.

The Dividend Advantage

It’s important to note that not all blue-chip stocks pay dividends. But many do. And several of those stocks have gone on to become Dividend Aristocrats and Dividend Kings.

A Dividend Aristocrat is a company that is part of the Standard & Poor’s (S&P) 500 Index and has increased dividend payouts for at least 25 consecutive years.

A Dividend King, meanwhile, does not have to be part of the S&P 500, but it does need to have grown its dividend payment for at least 50 straight years.

Of the blue chips we examined, only Procter & Gamble – with 69 consecutive years of increased dividends – has achieved Dividend King status. The others are on their way toward becoming Dividend Aristocrats, however.

Microsoft has increased dividends for more than 20 straight years, Apple has for 14 years, JPMorgan Chase has for 15 years, and Visa has for 17 years.

The appeal of stocks that pay consistent dividends is obvious. They offer an extra source of reliable income, which is especially helpful for those who have retired or are simply looking for some extra cash.

Even during market downturns, Dividend Aristocrats and Kings generally remain steady because most blue chips are strong companies in critical industries – like health care, consumer staples, finance, etc. That helps these stocks outperform the overall market on a risk-adjusted basis. And that makes blue chips solid defensive options for investor portfolios.

Plus, the dividends paid by blue-chip stocks can be reinvested, delivering compound growth to investors.

Institutional Strength

Another common trait of blue-chip companies is their overall strength. That includes strong cash flows, solid brand reputation, worldwide operations, and steady leadership – both at a company and industry level.

Together, these ingredients create world-renowned institutions within their sectors and instantly identifiable brands that consumers trust.

And that builds resiliency within these companies, which allows them to stand tall even during difficult economies.

Are Blue-Chip Stocks Good for Beginners?

Blue-chip stocks are ideal for beginning investors for several reasons.

- They’re easily recognizable and well known among most consumers. An investor-to-be wouldn’t necessarily need to conduct hours of research to know that, say, Apple is a successful company.

- Blue-chip stocks offer plenty of stability. Most first-time investors would probably feel much more secure putting their money into Walmart (WMT) or Visa than into a highly speculative business like a crypto-mining company. Investors probably won’t experience huge price spikes with a reliable blue-chip stock. But they likely won’t feel the anxiety that comes with plummeting prices either.

- As we covered, many blue-chip stocks deliver consistent dividends. And who doesn’t enjoy some extra income?

- There’s plenty of long-term potential for compound growth. Take Visa, for example. Its current forward dividend yield of 0.8% may not wow you at first glance. But consider that since Visa started paying dividends in 2008, the company’s payouts have increased 2,452%. So, if you invested $1,000 in Visa back in 2008, you’d be receiving nearly $600 in annual dividend income.

- While no business is fully immune to worsening market conditions, blue-chip companies are built to better withstand them. And even when the economy does hit a rough patch, many blue-chip stocks actually thrive because of their defensive, “safe haven” nature.

For example, if the markets go into a tailspin tomorrow, businesses like Procter & Gamble, Walmart, and Colgate-Palmolive (CL) would probably be just fine, if not in better shape. Why? Because consumers need their products to live their lives. Food, hygiene products, and household supplies are all essential items that need to be purchased regardless of the economy. That gives many blue-chip companies a major defensive advantage.

Of course, there’s an element of risk when investing in any stock. But blue-chip stocks can form a very strong foundation for any investor’s portfolio, especially those who are new to investing.

Key Risks to Consider

Blue-chip stocks are typically long-term winners. But there are no guarantees when it comes to investing, and that’s no different for blue chips.

Here are a few risks to keep in mind:

- Valuation risk: If you look through the charts for the stocks we covered, you’ll notice that their Valuation grades are the lowest (though most are still solid). That’s because many blue-chip stocks trade at premium valuations. That’s because investors place a high value on their consistency and stability.

- Growth ceiling: Investors looking for big growth spikes may want to check out AI and tech stocks. They often experience very high highs, but also potentially very low lows. Blue chips, on the other hand, won’t deliver those lofty highs. They also won’t plunge to disturbing depths. Blue chips will, however, deliver steady returns over the long term.

- Regulatory pressure: Depending on the sector, some blue-chip companies face their fair share of regulatory pressure, which can impact their business. For example, big tech businesses like the Mag Seven group often deal with regulatory scrutiny related to antitrust and monopoly concerns.

Building a Strong Portfolio With Blue-Chip Stocks

Blue chips are blue chips for a reason. They’re among the most reliable companies in the world, and among the most reliable stocks on the market.

Again, don’t expect fast or dramatic growth from the blue-chip stocks we covered here… or any blue-chip stocks, for that matter.

But for patient investors who want steady performance, strong business results, and consistent dividend payouts, blue-chip stocks like Microsoft, Apple, JPMorgan Chase, Procter & Gamble, and Visa are smart bets for 2026 and beyond.

Regards,

David Engle

Editor’s Note: Forbes calls $1 billion fund manager Louis Navellier “the king of quants.” Today, he’s stepping forward to reveal why he’s investing $358 million of his own firm’s money in the next stage of Artificial Intelligence… a technological sea-change that could erase millions of jobs, solve humanity’s biggest mysteries, and spark a wave of moneymaking opportunities — both in and outside the stock market. Click here for the details…