Abbott Laboratories (ABT) is making one of its biggest moves in years.

In November, the health care giant agreed to buy Exact Sciences for $105 per share in cash, a deal worth about $21 billion in equity value and roughly $23 billion including debt. The transaction closed on Monday, March 23.

With the deal, Abbott is buying one of the best-known names in cancer testing.

Exact Sciences built its business around tests that help find cancer earlier and guide treatment decisions. Its best-known product is Cologuard, an at-home colon-cancer screening test.

The logic behind the deal is easy to follow. Abbott wants a bigger role in a large and growing area of health care. Unfortunately, about 20 million people around the world receive a cancer diagnosis every year. Abbott has identified the U.S. market for cancer screening and precision oncology diagnostics to be worth about $60 billion.

Bolting on Exact Sciences allows Abbott to gain a stronger position in one of the most important trends in medicine.

What Abbott Does and Why Investors Trust It

Before we go deeper into Exact Sciences, it helps to step back and look at Abbott itself.

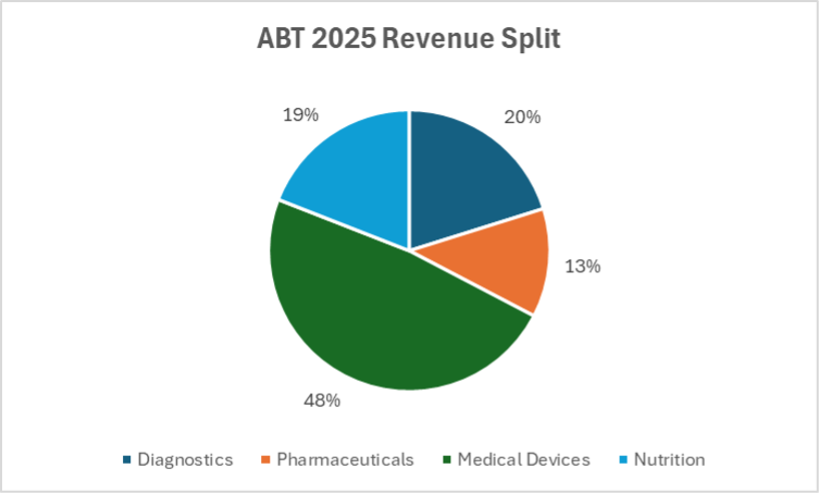

Abbott is a broad operator in the health care industry. Its business spans four main segments: medical devices, diagnostics, nutrition, and established pharmaceuticals.

Medical devices are the company’s largest business by far, accounting for nearly half of all revenue. In 2025, that segment generated $21.4 billion in sales. Diagnostics, the runner-up, brought in about $8.9 billion.

While diagnostics may steal the show, Abbott is not a one-trick pony. It’s a large operating company with multiple growth drivers and a global footprint. Abbott’s products range from FreeStyle Libre glucose monitors for people with diabetes to heart devices used in rhythm management, heart failure, and structural heart procedures.

The company also has a long track record of returning cash to shareholders. Last year marked its 408th consecutive quarterly dividend payment, and Abbott has now raised its dividend for 54 straight years. That makes it a “dividend king,” a lofty title often sought out by dividend investors.

Abbott provides consistency for investors who want exposure to health care without taking on the full risk of a small, speculative biotech name.

It also helps explain why Abbott could make a deal like this from a position of strength.

Abbott’s Core Business Still Looks Strong

The market still carries some old baggage when it looks at Abbott.

For a while, investors saw it as a COVID-19 testing winner that would have a hard time replacing that revenue once demand cooled off.

That concern was fair. Abbott’s diagnostics business, like many others, got a huge boost during the pandemic. Then those sales faded.

For instance, the company’s fourth-quarter 2023 earnings report showed that COVID-19 testing sales were $288 million for that quarter… down from $1.069 billion a year prior.

But the company did not stall out once the COVID boom ended.

Last year, Abbott posted $44.3 billion in sales. Its core base business experienced organic growth of almost 7%. Medical devices finished the year strong, growing by more than 10% in the fourth quarter. That marked the 12th straight quarter of double-digit organic growth in the segment.

The numbers tell the same story on an annual basis as well. Medical-device sales rose 12% in 2025 thanks to higher revenue across the entire business. The segment’s operating margin also improved to 33.7%, up from 32.4% a year earlier.

That strength gives Abbott room to think beyond the next quarter. While the diagnostics segment continues to chug along, the rest of the business is improving and cutting the reliance on one segment.

Abbott doesn’t need Exact Sciences to rescue the company. It wants Exact because the core business is healthy enough to support a move into a new growth lane.

And that new lane could help fix a weak spot.

Abbott’s diagnostics business is still its bread and butter, but it has not matched the momentum of medical devices. Diagnostics sales decreased by 4.5% over the past year, thanks to lower COVID-test demand and lower volumes in China.

That backdrop makes the Exact deal easier to understand. Abbott is using strength in one part of the company to rebuild growth in another.

Why Abbott Wants Exact Sciences

Abbott doesn’t need to learn a new business to make this deal work… It already knows diagnostics.

Hospitals and labs around the world use Abbott machines and tests every day. Exact adds a stronger position in one of the most promising parts of that market: cancer screening and treatment guidance.

Exact brought in more than $3 billion last year and is expected to contribute roughly the same amount this year. Through this transitional year, Abbott has penciled a small bump to 2026 sales growth and margins.

But more importantly, Exact gives Abbott a stronger foothold in a market with long-term demand behind it.

Its best-known products are easy to understand. Cologuard helps patients screen for colon cancer at home, and Oncotype DX helps doctors decide how aggressively to treat certain breast cancers. Exact also has newer blood-based tests and follow-up tools that can help detect cancer and monitor whether it may return.

Together, those products give Abbott more exposure across the course of care, from early screening to treatment decisions and follow-up monitoring.

Abbott also brings something Exact does not have on its own: global scale. Exact built a strong cancer-testing franchise in the U.S. Abbott already has deep relationships with hospitals, labs, and health systems around the world. Management sees that reach as a way to expand Exact’s products into more markets over time.

Of course, there’s never zero risk.

Abbott is spending about $21 billion to bring on Exact. That’s a major commitment.

Cancer testing is a large market, but it is also competitive, and integration always carries risk. Abbott will need to keep Exact growing while folding it into a much larger company.

Still, the logic is clear. Abbott is using its strength in its broader business to add a faster-growing diagnostics platform in an area of health care that should keep expanding for years.

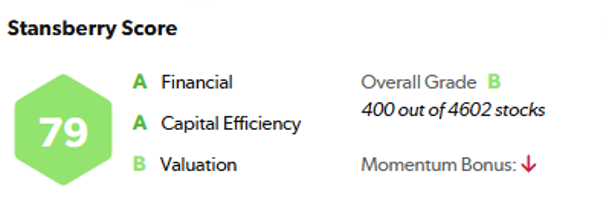

Abbott’s Stansberry Score Still Supports the Story

Abbott ranks in the top 10% of the 4,600-plus companies monitored by our proprietary Stansberry Score. That’s good enough to earn an overall grade of B. It scores an A for Financial strength, sporting a cash reserve of nearly $9 billion with only $5 billion of net debt.

With a 5-year average return on invested capital (“ROIC”) of 14% and a long history of rewarding shareholders, Abbott earns a grade of A for Capital Efficiency.

Abbott earns a solid grade of B for Valuation, meaning it’s fairly valued relative to its peers. The company has an enterprise value (“EV”) to earnings before interest, taxes, depreciation, and amortization (“EBITDA”) ratio of 19.6. To put that into perspective, its competitor Stryker (SYK) has a ratio of about 21.

Abbott’s score looks like what you would hope to see from a company of this size. It has financial strength, it uses capital well, and the stock is not priced so richly that investors must count on perfection. That gives Abbott a solid foundation, while the Exact Sciences deal gives it another path to growth.

It also arrives at a useful time for the sector. While investors spent the past two years crowding into AI winners, many health care stocks fell out of favor. In fact, Health Care is the worst-performing S&P sector over the past year, returning negative 1.09%.

But that doesn’t worry us. In fact, it has started to create a more interesting setup for companies like Abbott.

Why Health Care May Finally Be Getting Another Look

Health care has trailed the market for years.

A lot of money chased AI, software, and other fast-moving tech stories. Meanwhile, many health care and biotech stocks got cheaper and drifted out of favor. That has left the group in an unusual spot. The fundamentals in many cases still look sound, but the market has not rewarded them the way it has rewarded the hottest corners of tech.

We have been talking about that setup in Stansberry Innovations Report, where health care and biotech remain an important part of the portfolio. In our year-end comments, we noted that after such a strong run in AI-linked stocks, some investors may start taking gains and looking for opportunities in cheaper areas of the market, including health care.

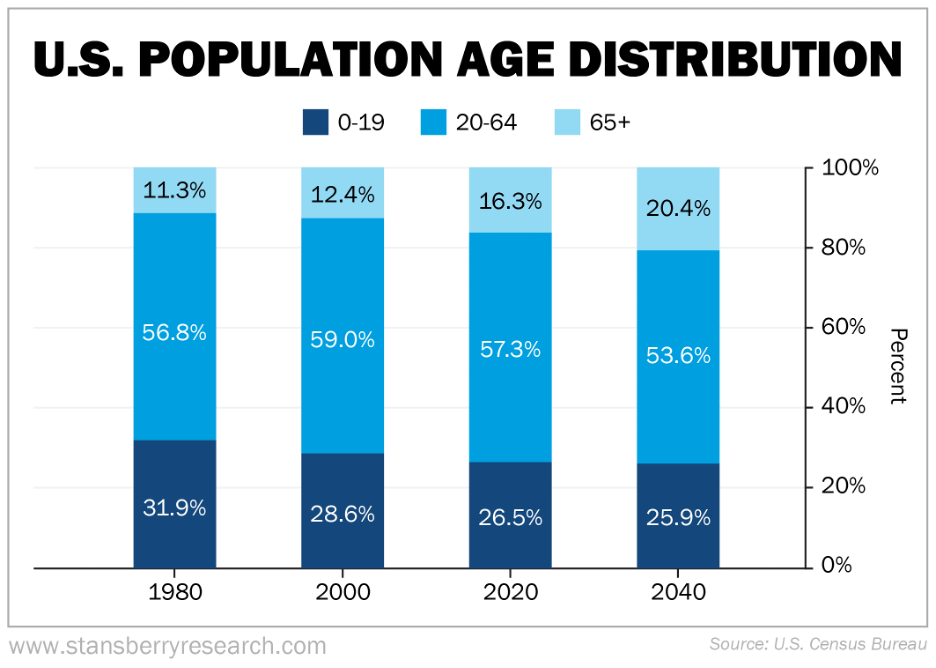

Another reason health care looks interesting today is simple demographics. America is getting older, and older populations need more care.

As older adults live longer, chronic conditions such as cancer, diabetes, and heart disease become more common. This means more testing, more monitoring, and more procedures over time. By 2040, adults 65 and older, the age at which medical needs significantly increase, will make up more than 20% of the population, according to a study by the Urban Institute.

For companies like Abbott, that creates a long runway of demand across diagnostics, devices, and other core parts of the business.

Abbott brings a different profile than many of the smaller and more speculative names investors often associate with health care innovation. The business is larger, more established, and easier to understand. With Exact Sciences, it also has a fresh growth lever tied to cancer screening.

A rebound in the sector is not guaranteed. But if money does start rotating back toward health care, Abbott looks like one of the steadier ways to play it.

Bottom Line

Abbott already looked like a solid health care business before this deal.

It had scale, a diverse product lineup, and strong momentum in medical devices. The Exact Sciences acquisition adds a larger role in cancer screening and treatment guidance.

That does not remove the risks, though. Abbott is spending a lot of money, and it will need to integrate the business well. But the logic behind the deal makes sense. Abbott is using a position of strength to improve one of its slower-growing segments and push deeper into a market with room to grow.

And if investors do start moving money out of crowded AI winners and back into health care, Abbott looks like one of the steadier names to watch.

For investors who want a large, established health care company with a new potential growth factor, Abbott deserves a closer look.

Good Investing,

Tyler Jarman

Editor’s Note: What should you invest in right now?

A renowned former hedge fund founder and his research team have found what they believe is the next big tech trend that could make investors rich.

It’s a breakthrough they’re calling “Helios” – and if you haven’t yet heard of it, you soon will.

Over the next few years, it could impact the food you eat… the water you drink… the places you live and work… and even the prices you pay for airfare, gas, electricity, and household goods.

“Helios” is going to cause a lot of people to lose money, too. Dozens of well-known businesses could go bankrupt.

But if you own a stake in this new tech, the positive effects will far outweigh the negatives. Get the facts for yourself. Make sure you’re not on the wrong side of this trend. Click here to see this new analysis…