Key Points

- Booking Holdings produces substantial free cash flow, giving it financial flexibility and long-term stability.

- The stock trades at a lower earnings multiple than both its historical average and the broader market, despite strong fundamentals.

- With global travel demand remaining resilient, Booking is well positioned to continue driving revenue and earnings growth.

Sometimes the best ideas come from the archives…

The online travel stock Booking Holdings (BKNG) is a stock my team at Stansberry’s Investment Advisory has been watching for years…. We first wrote about it in February 2019.

At the time, we identified Booking as a highly scalable business. Booking is the market leader in online travel booking. It owns multiple independently operated brands, including Booking.com, Priceline, Agoda, Kayak, and OpenTable.

The more hotels and unique places it offers on its websites, the more reason for travelers to use them and for new hotels to join its network. And long term, we were right about the business model’s success…

As you can see from this 10-year stock chart, the stock has more than doubled from our entry price of $72.13. But as you can also see, the stock has struggled since this past summer:

After peaking last July at $231.27, Booking fell 33% to a 52-week low around $150 in February amid fears that a war in Iran would hurt consumer spending and global travel.

It has rallied a bit since then, closing yesterday at $181.12. But that’s still 21.7% below last summer’s peak.

I like nothing better than buying a great company after it has sold off. So let’s take a look to see if Booking fits the bill today…

Cash Is the Key to the Booking Juggernaut

The February 2019 Investment Advisory issue described exactly what makes Booking’s such a great business:

You can book air travel and rental cars, as well as make restaurant reservations, on its websites. But the accommodation business not only provides most of the company’s revenues, it is also its growth engine. And the company expects that trend to continue. The growth is fueled by several powerful trends:

- Offline-to-online booking,

- Adoption of mobile devices, and

- Growth of travel in Asia Pacific.

These trends ensure the company has many more years of double-digit growth ahead of it.

These words are just as true today as they were in 2019.

Booking was also attractive because it was one of the most capital-efficient businesses we’d ever seen. As the issue explained:

Capital-efficient companies don’t need to keep extending their hand asking for more capital. That’s because their businesses generate loads of cash. They’re able to use this cash to reward shareholders by paying dividends… or buying back their own stock, reducing the number of shares outstanding. They may also choose to pay down debt or simply keep the cash and use it to fund future growth. No matter what they choose, shareholders win.

That’s why we love to invest in capital-efficient companies. They’re able to grow their businesses with their own capital. That’s a luxury most companies don’t have. It gives them a huge advantage… And this advantage compounds over time. When you invest in growing, capital-efficient companies and hold them for the long term, it doesn’t really matter when you invest in them. Their excellent businesses and cash-generating power propel them through good times and bad.

Booking: An Attractive Stock at an Attractive Price

Let’s take a look at Booking’s historical financials to see if it remains the capital-efficiency juggernaut we identified more than seven years ago…

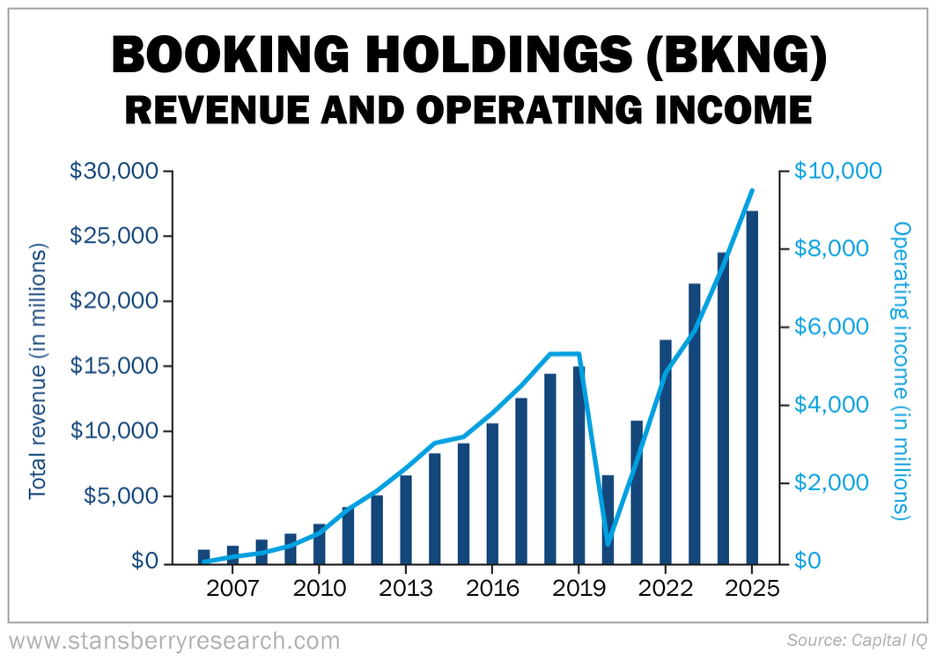

Revenue and operating income grew strongly for 14 years, then crashed during the pandemic (though note that the company was still profitable in 2020). Both figures have recovered and grown since then:

In the past 20 years, revenues are up 24 times, or 17.2% compounded annually. And operating income is up 153 times, or 28.6% annually. These are incredible numbers.

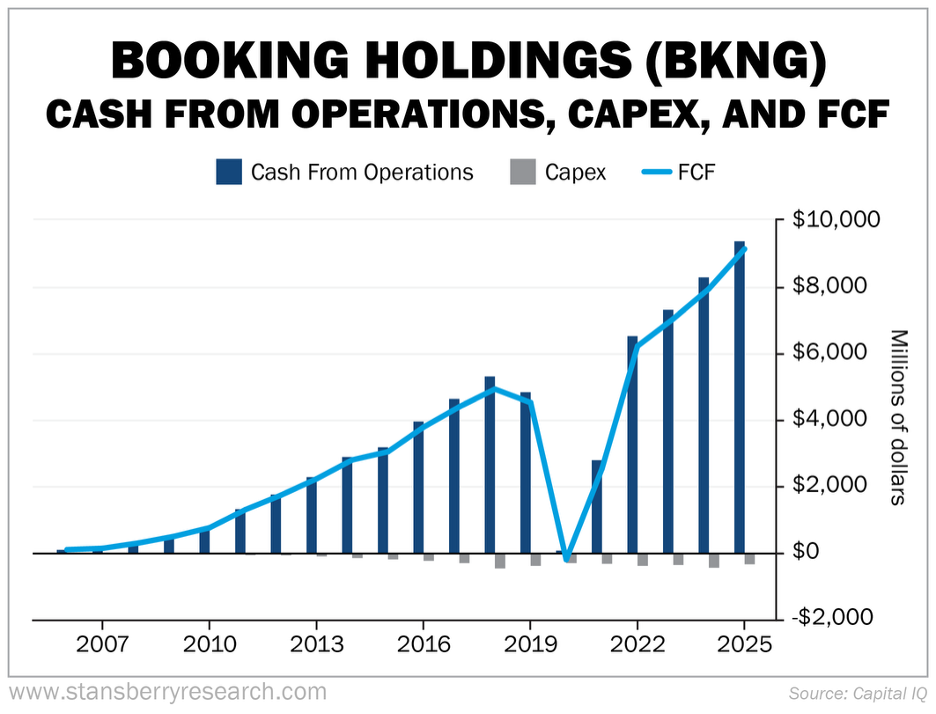

The cash-flow statement is equally remarkable. Booking has almost no capital expenditures (“capex”). And it has huge, growing free cash flow (“FCF”) – up 92 times in the past 20 years, or 25.3% annually:

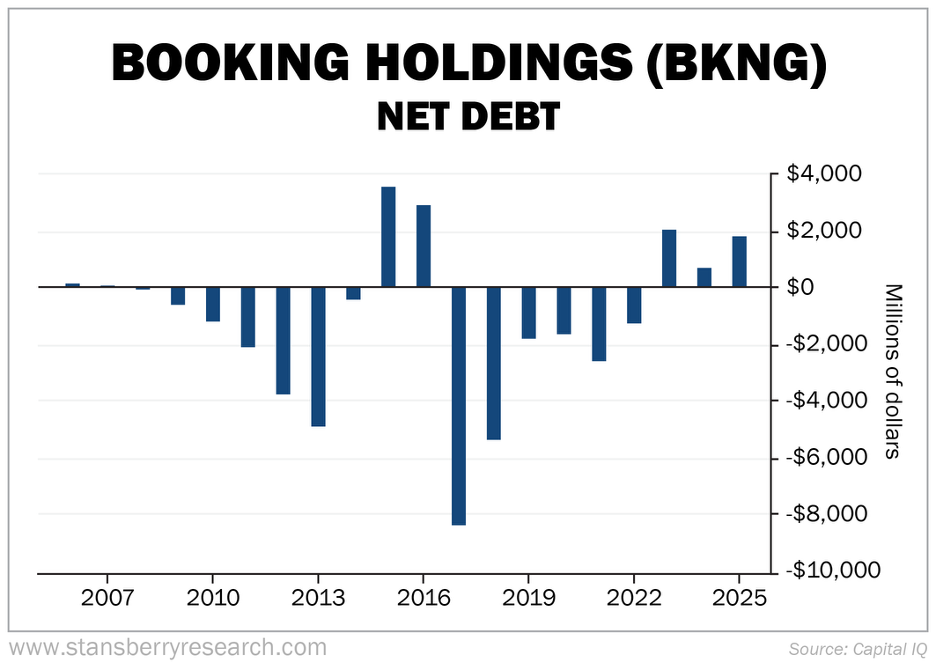

The company has always maintained a healthy balance sheet, with a net cash position in 13 out of the past 20 years:

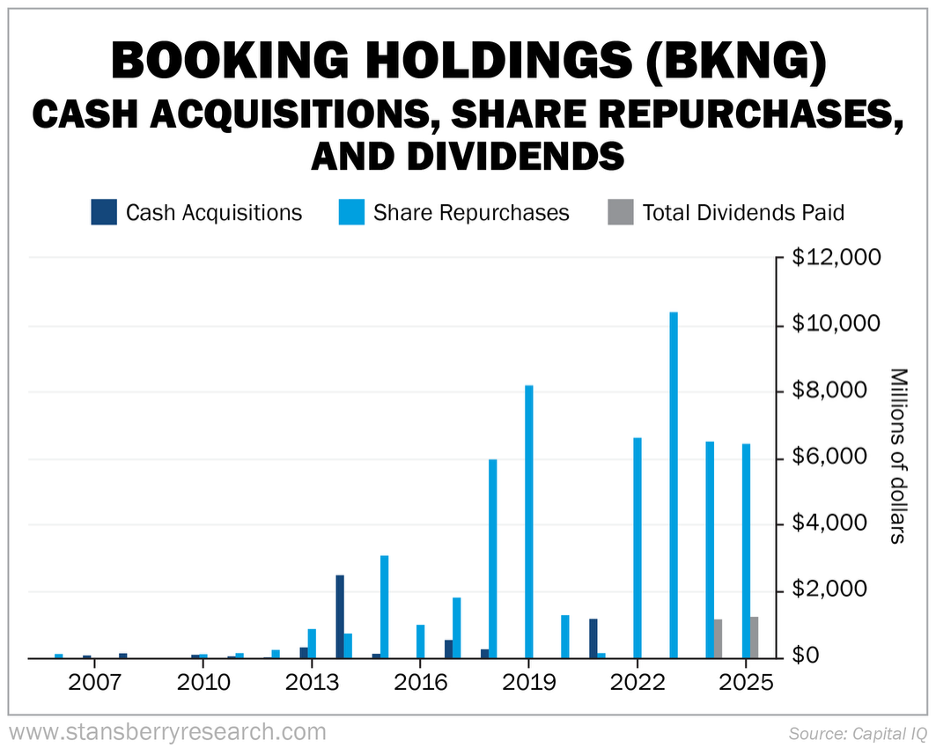

Whenever Booking has decided to take on a bit of debt, it has mostly been driven by large share repurchases. These really ramped up in 2018 and have remained at $6 billion or more since then, with the exception of the pandemic years in 2020 and 2021:

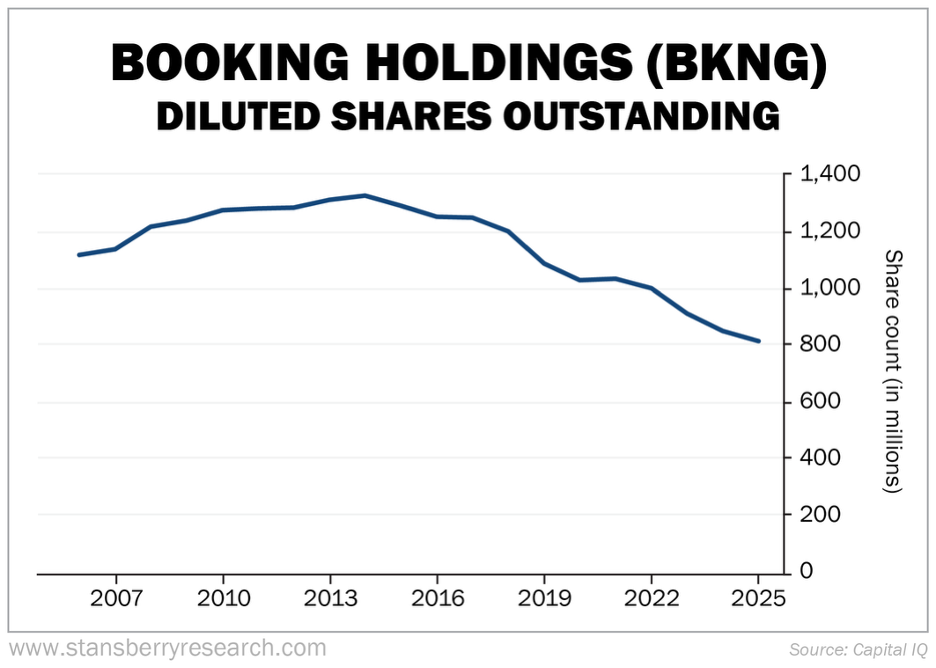

As a result, its diluted share count has declined by 38.4% in the 11 years since it peaked in 2014. This means Booking has been reducing its share count by 4.3% annually on average, providing a tailwind to earnings per share (“EPS”):

In summary, Booking’s financials are spectacular in every way and show no signs of weakening.

What about valuation? At yesterday’s close of $181.12 per share, the company has a market capitalization of $143.4 billion. Adding $1.8 billion of net debt, its enterprise value is $145.2 billion.

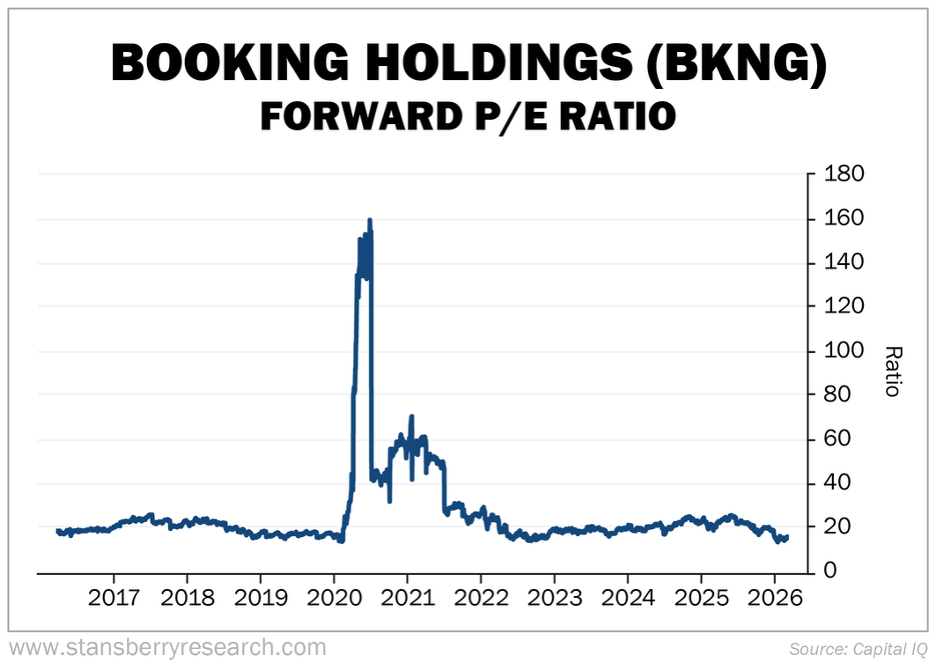

Analysts expect EPS of $10.71 this year and $12.51 next year. So the stock is trading at 16.9 times this year’s estimates and 14.5 times next year’s.

Over the past decade, Booking’s stock has, on average, traded at 27.2 times forward price to earnings (P/E). And as you can see in this chart, it has never been lower than 14.5 times:

That’s a very attractive price, both in relation to the stock’s history and the market. The S&P 500 Index trades at an average of just above 20 times.

Booking is a far above-average company trading at a below-average multiple.

Editor’s Note: This article was adapted from today’s edition of Whitney Tilson’s Daily. Every day, Whitney emails his readers with his comments on the most important topics of the day, including stocks he’s investigating… great articles he has read… his media and podcast appearances. You can sign up here to receive all of Whitney’s daily thoughts and insights.