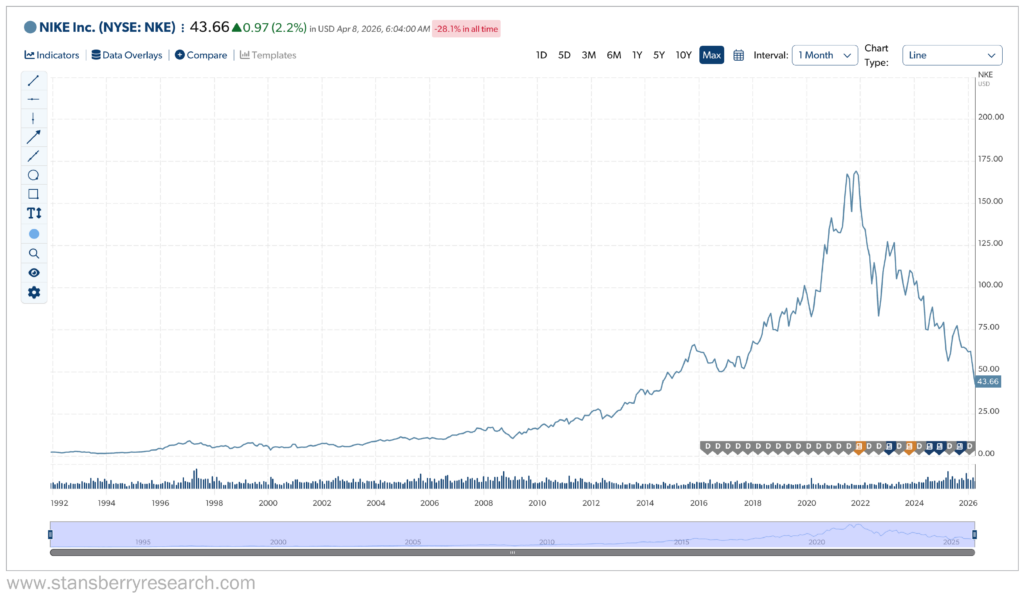

After releasing its disappointing fiscal third-quarter 2026 earnings on April 1, you can bet Nike (NKE) is pining for the “salad days” of 2021.

In early November of that year, Nike shares soared to an all-time intraday trading high of $179.10, driven by a COVID-19 demand boom, solid performance in China, and strong direct-to-consumer sales.

Barely half a year later, all those positives had become negatives.

By June 1, 2022, shares of Nike had plummeted to around $119. Just three months after that, on September 1, Nike closed at $106.49. So, in the span of 10 months, Nike’s stock had lost more than 40% of its value.

Nike’s share price briefly bounced back at the start of 2023, but the stock has seen a steady decline since.

On April 1, 2026, Nike shares closed at $44.63 after a rather dismal earnings announcement. Unfortunately for the iconic brand, this was no April Fool’s joke.

Since that November 2021 high, Nike shares have plunged by 75%.

What gives, and can investors expect Nike to bounce back?

Behind Nike’s Fall from Grace

Since Michael Jordan laced up his first pair of Air Jordans as a rookie for the Chicago Bulls in 1984, Nike and its famous “swoosh” logo have dominated not only the sneaker and athletic apparel industry, but also global pop culture.

Athletes of all ages likely recognize Nike’s world-famous “Just Do It” slogan. Or the late 1980s commercials featuring Jordan and Spike Lee (as Mars Blackmon), with the catchphrase, “It’s gotta be the shoes.”

Nike was on top of the world. And it remained there for nearly four decades.

But the company chose to pivot to direct-to-consumer (“DTC”) sales around 2017. Nike doubled down on the DTC strategy in 2020 by prioritizing its digital sales, its Nike and SNKRS apps, and its retail stores.

Nike hasn’t been quite the same since.

The strategy made some sense at the time. By pushing customers to buy directly from Nike rather than through a middleman or third-party retailers like Foot Locker, Dick’s Sporting Goods (DKS), and Zappos, the company aimed to maximize its margins. And it did result in higher profits. Nike Direct (the company’s digital and owned stores) accounted for roughly 44% of sales by 2023.

But it also opened the door for competitors (and there are a lot of them) to take Nike’s place on store shelves and eat into the company’s market share.

And those competitors capitalized on Nike’s pivot.

Performance running sneaker brands like Hoka, Brooks Sports, and On Running gained significant market share among serious runners. And New Balance, with its “dad shoes” becoming a popular fashion choice among young consumers, took a big bite out of Nike’s lifestyle sneaker business on its way to $9.2 billion in revenue – a 19% year-over-year jump – in 2025.

Experts believe that Nike’s former Chief Executive Officer (“CEO”) John Donahoe severely misread both the sneaker market and his customer base.

According to Tom Nikic, senior research analyst at Needham & Co., “It’s become clear the prior regime completely misjudged the sneaker market, period. The importance of product development. The importance of good wholesale relationships. The way that customers shop. What customers look for. All of that was misjudged.”

That all culminated in Nike’s most recent earnings announcement.

Nike’s Q3 2026 Earnings: China Sales and Analyst Downgrades Send Stock Reeling

Some year-over-year highlights (if you can call them that) from Nike’s third-quarter 2026 earnings call:

- $11.3 billion revenue, flat on a reported basis, down 3% on a currency-neutral basis

- $4.5 billion Nike Direct (its DTC segment) revenue, down 4% on a reported basis, down 7% on a currency-neutral basis

- Gross margin down 130 basis points to 40.2%

- $0.35 diluted earnings per share (“EPS”), down 35%

- $6.5 billion wholesale revenue, up 5% on a reported basis, up 1% on a currency-neutral basis

- $635 million operating income, down 19.4%

- $520 million net income, down 34.5%

The reality is that tariffs are killing Nike’s gross margins, and the company’s restructuring under current CEO Elliott Hill is still a work in progress.

Another big challenge Nike needs to overcome is shrinking sales in China. Considered Nike’s largest international growth driver, Greater China is key to the company’s success. But sales fell 7% year-over-year during the third quarter. Nike is also projecting another 20% decrease in sales for China during 2026 Q4.

Unfortunately for Nike, that wasn’t the only forecasted decline. The company’s management projects an anticipated revenue decline of 2% to 4% in the fourth quarter as well. That prompted a big-time sell-off of Nike shares as well as analyst downgrades from JPMorgan Chase (which cut its Nike price target from $86 to $52), Goldman Sachs, and Bank of America.

This all led to a one-day 15.5% drop in Nike’s share price, from $52.82 to $44.63. Year to date, the stock is down about 30%.

It has obviously been a tough run for Nike over the past few years. The question is, can Nike make a comeback sooner rather than later?

Can Nike Turn Things Around Quickly?

Legendary Wall Street investor and Stansberry Research colleague Whitney Tilson believes in Nike. But he cautions that it might take some time.

In his April 1 Whitney Tilson’s Daily newsletter, Tilson stated:

The key question is: Can Nike return to its former glory? Or has it been permanently impaired, either due to its own missteps or rising competition?

My instinct says it’s the former. Nike’s brand and global reach are among the strongest of any company in the world. But I need to do a deeper revisit of the stock.

For what it’s worth, I’m inclined to agree with Whitney.

Nike itself acknowledges that its turnaround from the Donahoe days is progressing more slowly than investors and analysts would like.

During Nike’s earnings call, Chief Financial Officer (“CFO”) Matthew Friend said, “We remain confident in our ability to position the company for profitable growth long term,” while also admitting that “our comeback is taking longer than we would like.”

The first step to fixing a problem is admitting there is a problem, right? Nike has done that. Now it’s up to CEO Hill, CFO Friend, and the rest of Nike’s leadership to execute their turnaround plan.

Nike does have some positives to build upon.

As of 2024, Nike was still the global market share leader in athletic apparel and footwear at 16.4% (Adidas, at 9%, was second). And Nike’s global distribution is second to none.

Plus, in Q3 2026, Nike’s North American quarterly sales improved 3%, its wholesale business grew by 5%, and its Nike Running line surged more than 20%.

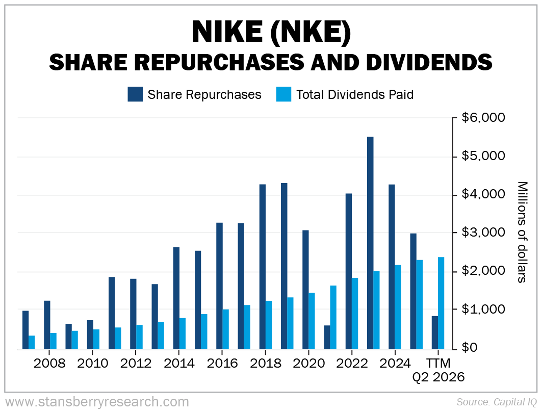

More importantly for investors, Nike is just one year away from establishing itself as a Dividend Aristocrat – a company that has increased their dividends for 25 straight years. Nike just paid its shareholders a quarterly dividend of $0.41 per share, so there is some internal confidence that the company will continue to generate cash in the long term.

Nike will also be a major player during the 2026 FIFA World Cup. And it’s counting on the world-famous football (soccer) competition to help turn around sales.

The company will be supplying kits for the teams representing the U.S., Canada, South Korea, Australia, Brazil, Uruguay, England, France, Croatia, Norway, Netherlands, and Turkey. It’s also collaborating with high-profile artists and fashion brands to create World Cup-themed streetwear.

Will the World Cup give Nike the momentum it needs to reverse its fortunes? We’re likely to find out later in the summer once the event ends.

Is Nike Stock a Buy Right Now?

That all depends on your confidence in Nike. If you think this is just a bump in the road for Nike, then yes, now could be a great time to buy.

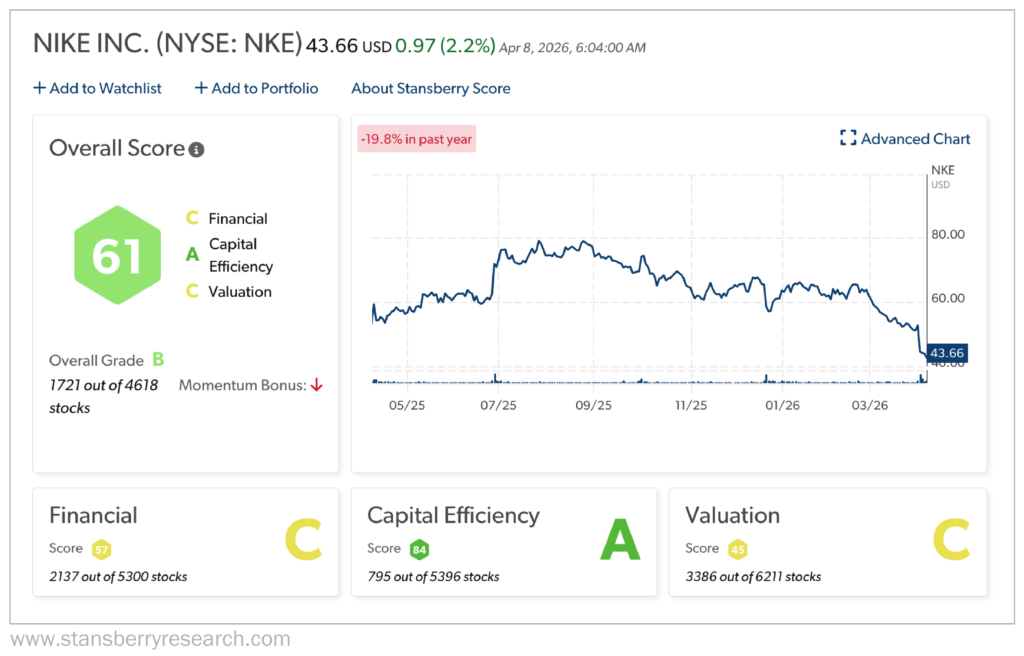

The stock itself is still in solid shape overall, especially when looking at its Stansberry Score (a tool that helps determine the quality and long-term value of thousands of stocks).

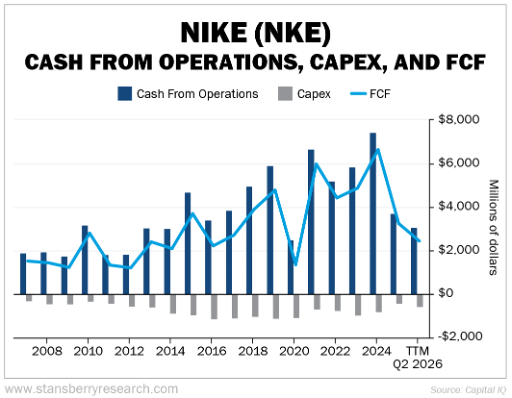

Overall, Nike earns a “B” grade, driven mostly by its excellent capital efficiency, which is boosted by Nike’s DTC model, as it helps improve margins and inventory management. Plus, Nike’s capital expenditure is decreasing – it hit a five-year low of $430 million in fiscal year 2025.

And that adds to the company’s free cash flow, allowing Nike to consistently pay increasing dividends to its shareholders.

Nike’s valuation is a different story, as you can see by its “C” Stansberry Score. On that topic, Tilson commented on April 1:

But what about the valuation? At this morning’s price of around $45.50 per share, the company has a market cap of $67.4 billion. Adding $3.1 billion of net debt, its enterprise value is $70.5 billion.

Nike earned $2.16 per share in its 2025 fiscal year and looks to earn around $1.58 in fiscal 2026, ending two months from now.

Analysts were projecting EPS around $2.31 for fiscal 2027, but given the weak guidance for the rest of this calendar year, I think they’d be lucky if it came in at $2.

All this means the stock is trading at 22.8 times next year’s earnings. That doesn’t appear cheap for a company struggling to turn itself around…

Nike is a tough company to give up on, even after a few years of declining performance. It’s a huge, iconic brand. It has a CEO who seems intent on righting the ship. And there are some promising financial signs to point toward.

But the company has a major problem to solve in China. Restoring sales in Greater China to 2021 levels – or close – will go a long way toward Nike regaining its former glory with investors.

Another risk to monitor: President Donald Trump’s tariffs have choked Nike’s gross margin. If they remain or if Trump imposes new duties in their place, Nike’s margins will likely continue to suffer.

There’s a lot to consider if you’re thinking of investing in Nike. Recent performance would suggest proceeding with caution. But if you’re a believer in the company’s track record of success and its place in brand iconography and pop culture, and you want to buy the dip, well… Just Do It.

Regards,

David Engle

Editor’s Note: Whitney Tilson — the hedge fund manager CNBC called “The Prophet” — says America has reached its “Ripping Point.” The old financial order is being torn apart, and he believes most investors have no idea what’s coming in the next six months. He’s named the stocks he thinks will be destroyed in the chaos — and the ones he believes will soar. Watch his free presentation while it’s still available.