Media and entertainment company Paramount Skydance (PSKY) has “won” a bidding war against Netflix (NFLX) to acquire Warner Bros. Discovery (WBD).

I put “won” in quotes because Paramount is massively overpaying. It will be saddled with at least $79 billion in debt once the deal closes (likely in the third quarter). Some analysts think it could be as much as $100 billion.

There’s no way the company can support such a high debt load… So I expect it to be financially crippled the day the deal closes and eventually file for bankruptcy, wiping out shareholders.

Analyzing Paramount Skydance’s Financial Decline

To understand why, let’s take a look at both Paramount’s and Warner’s financials over the past two decades, starting with Paramount…

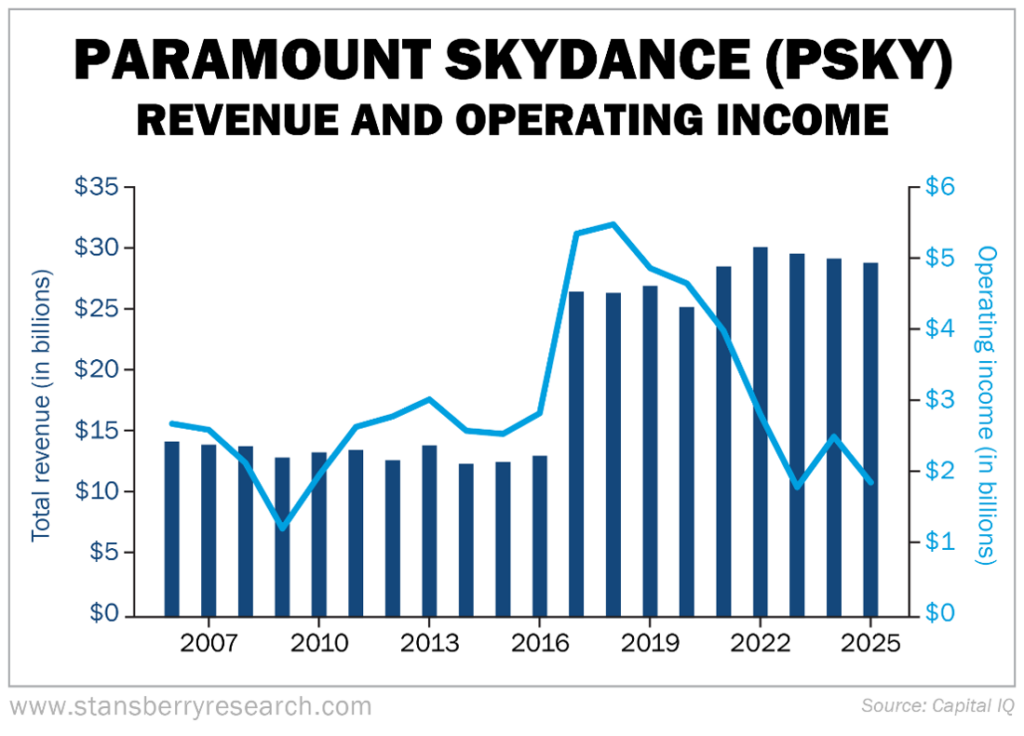

Revenue and operating income have been declining for years:

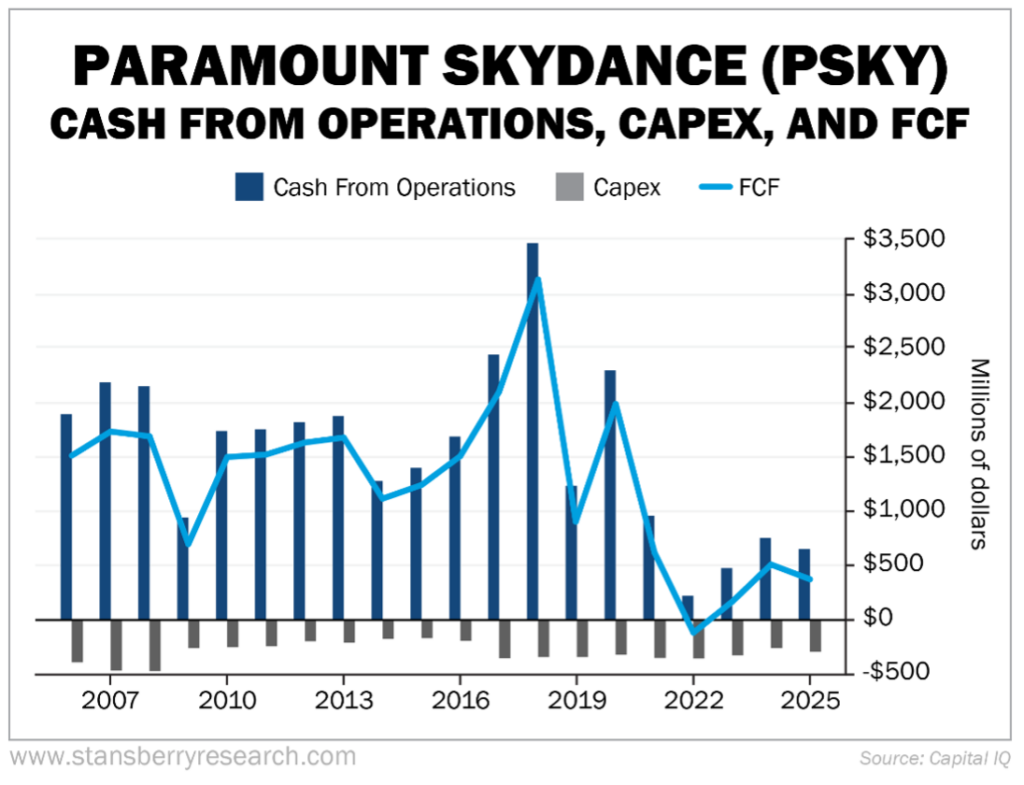

Free cash flow (“FCF”) has been tepid:

Paramount Is Taking on Unsustainable Debt

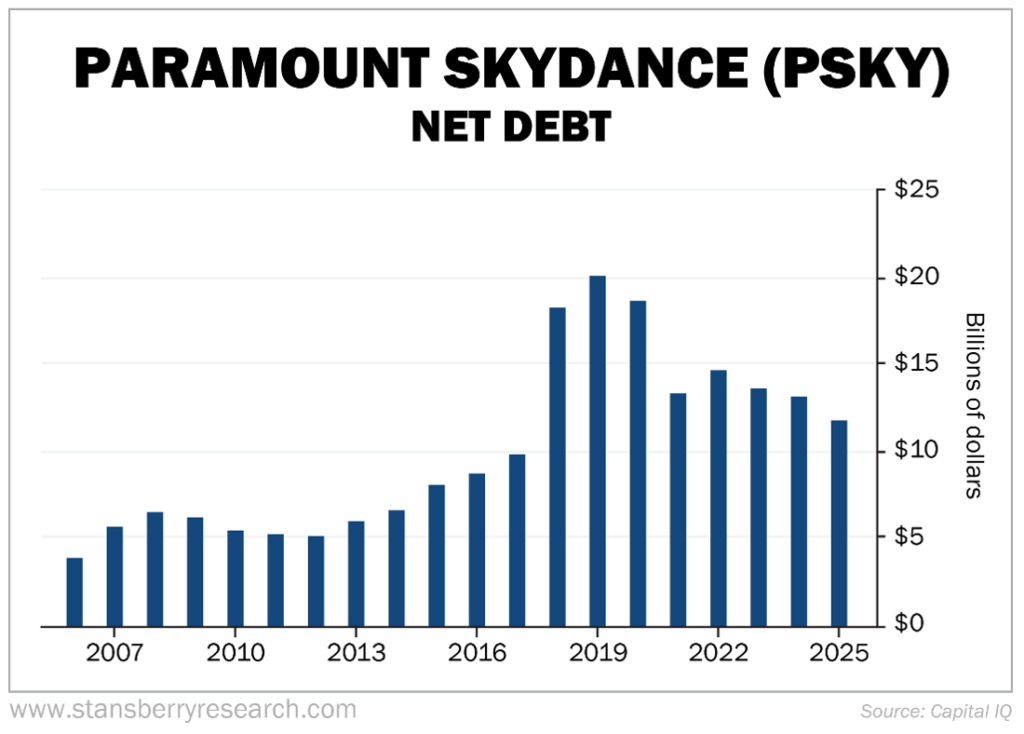

And while Paramount has paid down some debt, it remains high:

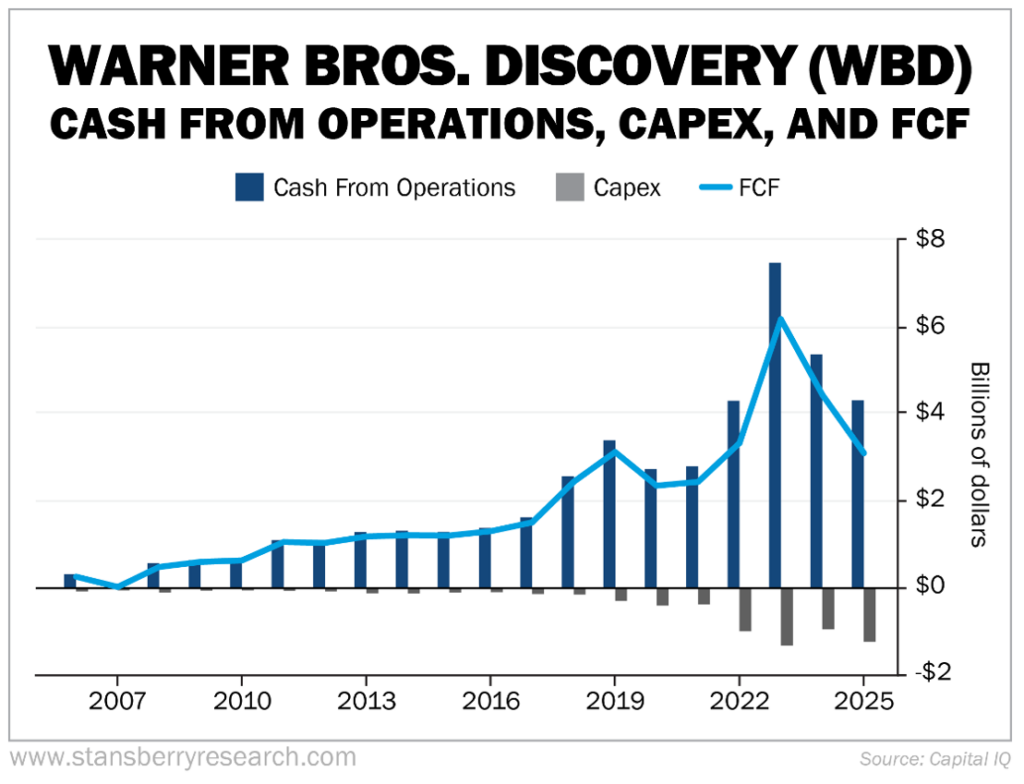

Warner Bros. Discovery: Declining Assets and Plunging Free Cash Flow

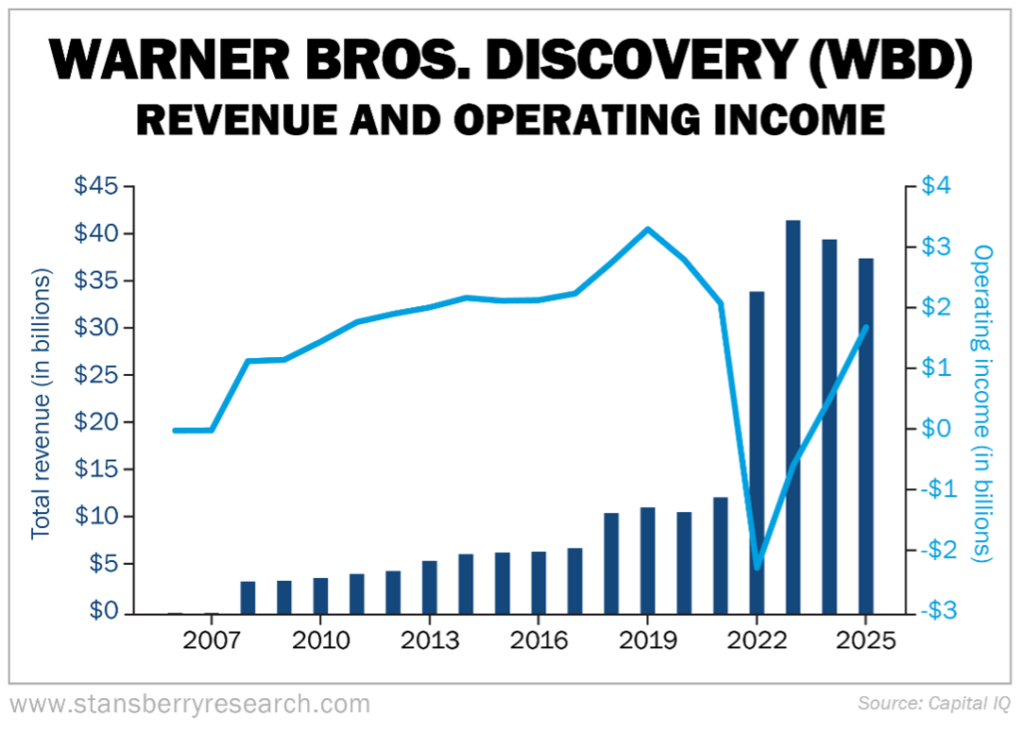

Turning to Warner, the company had a surge in revenue – but a crash in profits – when it merged with Discovery in 2022. Since then, profits have recovered somewhat, while revenue has declined in the past two years:

FCF has also plunged over the past two years:

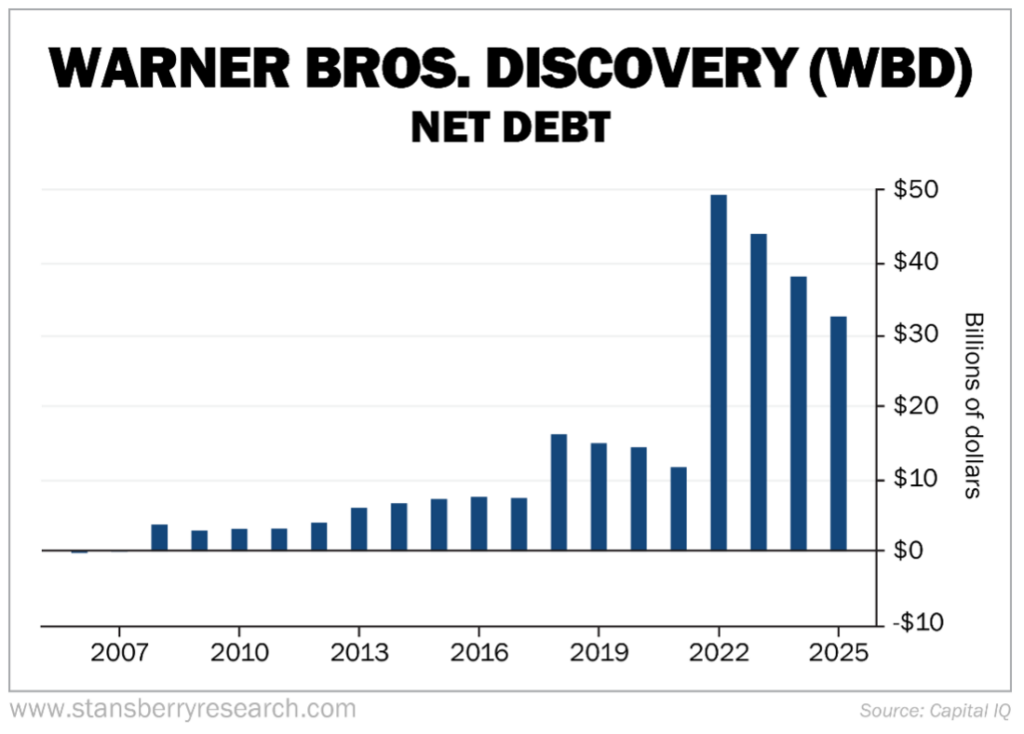

The company has been paying down the huge debt load it assumed in the 2022 merger, but it remains high:

A $111 Billion Gamble: Why This Deal Could Bankrupt Paramount

If Paramount and Warner were simply merging, their combined net debt load of $44 billion would be high but not bankruptcy-inducing in light of their combined FCF of $3.4 billion last year.

But that’s not what’s happening: Paramount is buying Warner for a wildly inflated price of roughly $111 billion (including the assumption of $32.2 billion of 2025 net debt). That’s for a declining asset that generated a mere $1.7 billion of operating income and $3.1 billion of FCF last year.

This deal reminds me of the saying, “Two stones tied together still sink.”

New York University marketing professor Scott Galloway shares my view. In an essay on his Prof G Media website, Galloway called it “the worst acquisition in history.” He concludes:

There are only two ways to make money in the media business: bundling and unbundling. We’re in a bundling phase. The question isn’t what the Ellisons will do with Paramount and WBD, but who will acquire those assets at fire-sale prices when their AI synergy narrative can no longer provide cloud cover for their pair of overleveraged legacy media companies.

Avoid Paramount’s stock at all costs.

Note: This article was adapted from today’s edition of Whitney Tilson’s Daily. Every day, Whitney emails his readers with his comments on the most important topics of the day, including stocks he’s investigating… great articles he has read… his media and podcast appearances. You can sign up here to receive all of Whitney’s daily thoughts and insights.