2026 is not off to a great start for the Magnificent Seven…

The Roundhill Magnificent Seven Fund (MAGS) – which tracks Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Meta Platforms (META), Microsoft (MSFT), Nvidia (NVDA), and Tesla (TSLA) – is down about 6% this year.

When you zoom out further, MAGS last made a high on October 29 and is down more than 10% since. Over the same period, the S&P 500 Index is up slightly.

And the Invesco S&P 500 Equal Weight Fund (RSP) – which doesn’t give higher weights to larger companies like the S&P 500 – has outperformed. It’s up more than 8% since the Mag Seven last made a high.

A decline like this isn’t common for these market winners. And you might be wondering whether it’s a serious sign of weakness… or a rare window when these giants go on sale.

With that in mind, how do these tech giants stack up today? Before we answer that, we need to dive into…

Why the Mag Seven Lead Markets

These seven companies make up a combined 33% of the S&P 500. And when you look at the tech-heavy Nasdaq 100 Index, that weighting gets even larger. They make up a combined 41% of the Nasdaq 100.

Last month, my colleague James Royal wrote about why the Mag Seven have such a big pull on broader markets. In short, size matters. From James…

These large weightings are also a huge factor in the returns of the major indexes themselves. Looking at just the S&P 500, the Magnificent Seven contributed 55% of the total return of the index from 2023 through 2025, according to S&P Global.

But that weighting can work against them in downturns. Since they make up such a large part of those indexes, they can drag the rest of the market lower, too. That’s what we saw in 2025…

MAGS peaked in December 2024 before turning lower – eventually falling more than 26% by “Liberation Day” in April. Meanwhile, the broader market traded flat throughout the end of December 2024… before following MAGS and declining about 17%.

If you look at RSP, which doesn’t give the Mag Seven higher weight, it fared much better – “only” falling 13% by Liberation Day.

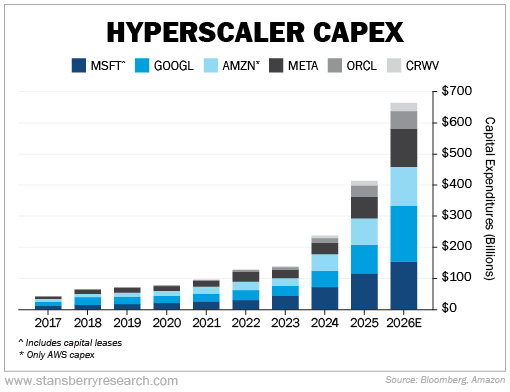

‘Hyperscalers’ Are Spending Big in 2026

Over the past few weeks, we got earnings updates from the hyperscalers. Many of these companies are included in the Mag Seven…

As Stansberry Research publisher Matt Weinschenk explained in This Week on Wall Street in October, hyperscalers are the companies that are building data centers to run their AI models.

Meta, Microsoft, Alphabet, and Amazon have all reported their fourth-quarter and full-year results for 2025. But investors weren’t too worried about their operations.

Instead, all the focus was on how much these companies are investing in AI in 2026. For example…

- Alphabet expects total capital expenditures (“capex”) of $175 billion to $185 billion this year… up to double the $90 billion the company spent on capex in 2025.

- Amazon forecasts $200 billion in capex this year, up 53% from 2025 and well above Wall Street’s estimate of $145 billion.

When you add in Meta Platforms and Microsoft, the four “hyperscalers” have pledged more than $650 billion in combined capex for this year – up 71% from 2025. Just take a look at this chart from the Stansberry’s Investment Advisory team (and shared in the February 9 Stansberry Digest)…

Hyperscalers Used to Be Capital Efficient, But No Longer

For years, Big Tech companies produced loads of free cash flow (“FCF”). FCF is simply a company’s operating cash flow minus any capex. It’s a measure of how much money is left over for things like dividends, buybacks, or reinvestment in the business.

In the past, the hyperscalers’ Internet-based business models meant they could grow without big increases in spending.

Microsoft is a great example… It doesn’t cost the company extra to sell a new Office subscription, so every incremental subscription was pure profit.

Meta is another great Internet company. It doesn’t take any more incremental cost to set up a new Facebook or Instagram account, so Meta can easily collect that new data and target ads – basically for free.

But that low-cost business model has changed as these companies invest heavily in AI.

Only one of the four hyperscalers – Microsoft – is expected to be able to cover its capex with the cash it generates from its operations this year. That means the rest are going to have to come up with the money another way – like with new debt or share offerings.

And that changes the investment case for them. As Stansberry’s Investment Advisory editor Whitney Tilson wrote in his free daily e-letter on February 6…

In the short run, it makes these companies, which previously had asset-light, high-free-cash-flow businesses, look a lot worse. If this is a permanent state of affairs, then these stocks deserve a much lower multiple and should be sold.

That’s exactly what we’re seeing in the market’s response…

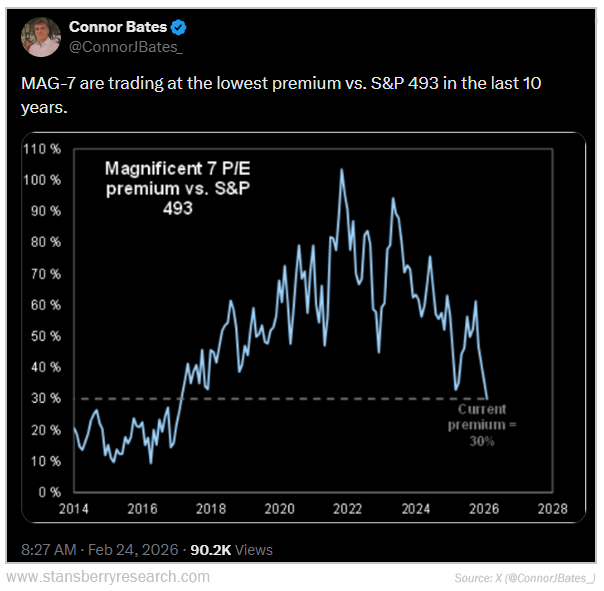

Looking at the Mag Seven’s price-to-earnings (P/E) ratio, the group now trades at a 30% premium to the “rest” of the S&P 500. As Revere Asset Management’s Connor Bates shared on social media platform X, that’s the lowest premium to the market for this group of stocks since 2017. Take a look…

With the companies pledging so much spending, they won’t deliver as much FCF as they have for the past 10 years. And some may even go FCF negative as they invest in AI. As a result, folks are dumping these stocks.

Are Alphabet, Amazon, Meta Platforms, or Microsoft Good Stocks Today?

These companies don’t have to worry about their heavy investments pushing them into bankruptcy. Alphabet, Amazon, Microsoft, and Meta all still produce loads of cash flow from their core operations and have been sitting on piles of cash.

Until AI, they just didn’t see an opportunity worth deploying so much of it. That won’t change the fact that these companies have hugely profitable businesses.

To see whether these companies are good investments today, we’re going to turn to our proprietary Stansberry Score. Our tool gives stocks a simple grade based on four main factors… capital efficiency (the hallmark of Stansberry Research), financial, valuation, and momentum.

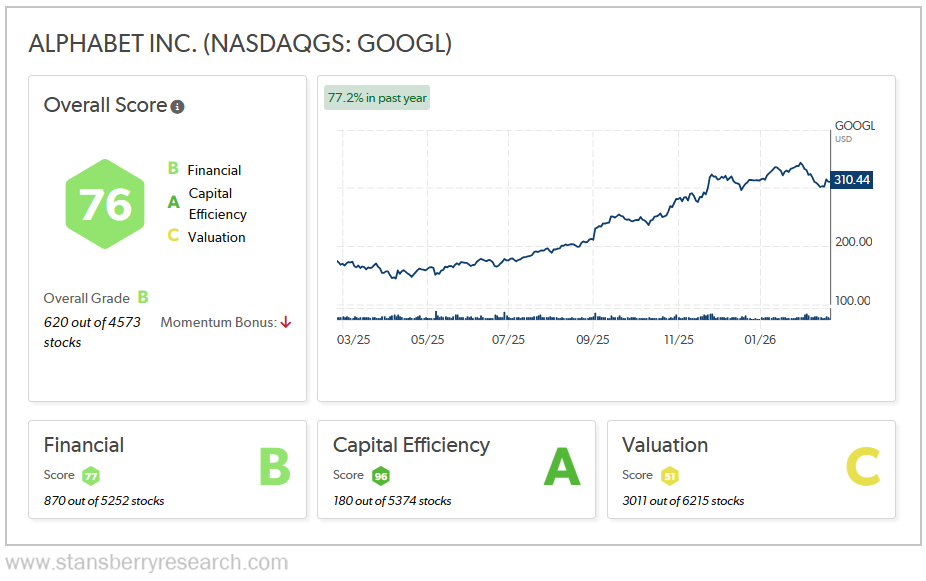

Let’s start with Alphabet…

Alphabet gets a score of 76 out of 100. That earns the Internet giant an overall grade of B.

Alphabet gets a B grade for its financial, thanks to its surging revenue and thick margins. (You can read more about those in Whitney’s February 5 daily here).

And since its core business is completely Internet-based, it produces loads of FCF. That earns it an A grade for capital efficiency.

At a P/E ratio of 28X, Alphabet is trading at right around the same valuation as the broader market. So it gets a C grade for valuation.

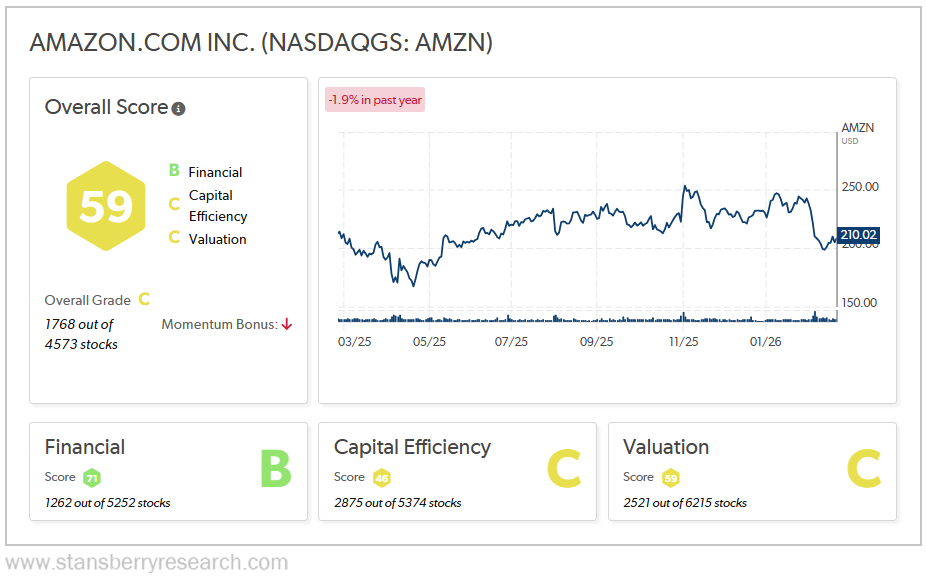

Moving on to Amazon, the online retailer and cloud-computing giant earns a score of 59 – good for an overall rating of C…

Amazon’s cloud-computing segment produces thick margins, but its retail arm has much thinner margins. Still, it gets a B grade for the financial component.

As for capital efficiency, Amazon invests heavily in its warehouses and distribution centers, and is now plowing money into AI. So it gets a C for capital efficiency.

Like Alphabet, Amazon is just about as expensive as the market. So it earns a C for valuation, too.

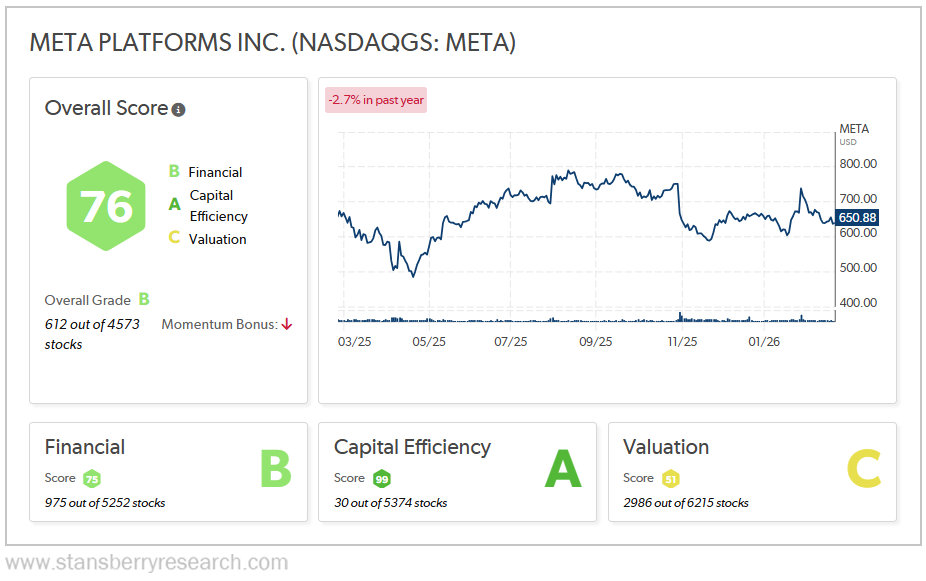

Meta Platforms gets a score of 76 and an overall grade of B. Take a look…

Like Alphabet, its core business relies entirely on the Internet, so it can produce loads of FCF. So it gets an A for capital efficiency. And it’s still growing revenue at a rate above 20%, which is great for a company of that size – earning it a B rating for financial.

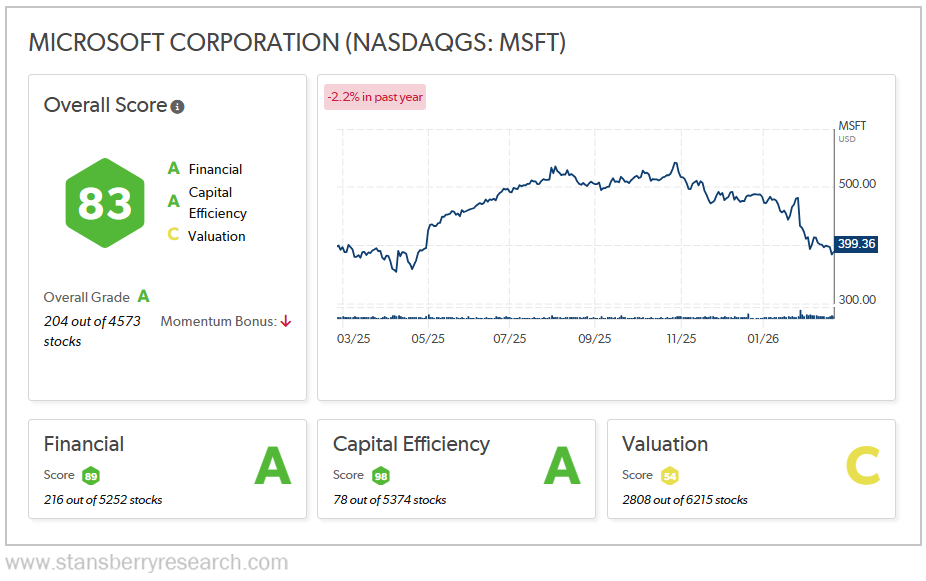

Meta is slightly less expensive than the market at 27X earnings, but that’s not enough of a discount to consider shares “cheap.” So it gets a C for valuation. Finally, software giant Microsoft gets an A grade and a total score of 83…

The company gets “A’s” for both its financial and capital efficiency (for the same reasons we explained above). And while its P/E ratio of 23X is cheaper than the S&P 500’s 28X ratio, it’s still not in “screaming buy” range. So Microsoft also gets a C for valuation.

All of these companies have stellar underlying businesses. In the long run, they’ll be just fine. But in the short term, investors are getting impatient looking for when and how much return the companies will get from their AI investments.

Based on our system’s ratings, Amazon is the laggard of the group. But all four of these companies still look like good long-term investments today. Their “C” grades for valuation shouldn’t surprise investors – since these companies have such strong core operations, they rarely (if ever) trade at steep discounts.

Just expect any AI headlines – and certainly future updates on spending – to bring a little “noise” in the near term.

Good investing,

Nick Koziol

Editor’s Note: If you’re 50 or older… or thinking ahead to retirement… legendary investor Whitney Tilson says this could be your smartest financial move of the entire AI boom.

It’s time to look past Nvidia and the “Magnificent 7.”

Whitney, a retired hedge fund manager once dubbed “The Prophet” by CNBC, is sharing a new AI story.

His brand-new stock system just gave one company a near-perfect grade… and it’s not a name you’ve heard on the news.

The company just signed a huge new AI deal with a key tech partner, and you’ll soon see a massive nationwide rollout.

Whitney’s giving away the name, ticker, and full breakdown for free.