The conspiracy theory about the silver market goes something like this…

The price of silver you see quoted is a farce. It’s the price of an empty promise based on “paper” silver traded via futures contracts, whose volumes and claims dwarf the physical metal sitting in vaults.

Trading desks at big banks, including JPMorgan (JPM), allegedly coordinate to suppress the price of precious metals. They do this by aggressively selling silver futures into strength, capping rallies and shaking out leveraged longs before quietly covering their shorts at lower prices.

Sometimes, silver starts to overwhelm the shorts.

In that event, as the conspiracy goes, the COMEX, the gold and silver futures exchange, comes to the banking cartel’s rescue. The COMEX hikes margin requirements, killing the precious metals bull market before things really get out of hand.

Of course, the Federal Reserve and U.S. Treasury are complicit in this scheme because they want to mask the true rate of inflation and prevent a massive loss of confidence in the U.S. dollar, a fiat currency backed by nothing but the full faith and credit of the U.S government. And there’s nothing like a massive rally in precious metals to shake investor confidence in the dollar.

That’s the narrative, and it contains just enough truth to be plausible.

For example, over the past decade, several prominent banks have settled charges related to manipulation and trade “spoofing” in the precious metals markets. JPMorgan even paid a fine totaling more than $900 million.

There has clearly been short-term manipulation at the order book level. But evidence is scant of a decades-long, policy-level scheme to suppress silver and gold.

Nonetheless, with the price of precious metals going parabolic recently, social media is abuzz with variations of “the paper shorts are out of ammo” or “the COMEX vaults will be empty” or even “the fiat system is entering its endgame.”

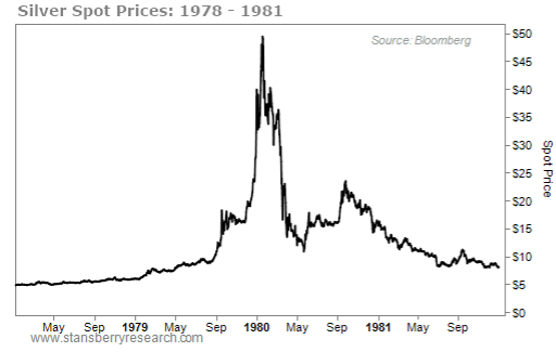

The spot price of silver reached a record of more than $121 per ounce on January 29 following a spectacular rise of 200% in just six months.

Silver’s surge is reminiscent of the great silver mania in 1979 and early 1980. It looks awfully like a blow-off top, although there’s no telling when it will end, exactly.

Regardless, there will be lots of volatility. It’s already starting. Silver suffered a 12% decline yesterday within 90 minutes of hitting an all-time high.

Editor’s Note: By the time this article was published on January 30, the price of silver was already under pressure. Silver ended up crashing that day by more than 35% before recovering slightly. Indeed, the forecast for volatility has already proven prescient.

Trading volumes are exploding. Fortunes are being made. Many will be lost. But rest assured, the COMEX will “win.” And to help put this crazy silver market in perspective, it’s worth taking a look back at when the market was “cornered.”

The Original Silver Squeeze

In 1973, Nelson Bunker Hunt’s inherited oil riches took a hit when the Libyan government nationalized his oilfields in the country.

That’s when Hunt, who was still a billionaire, became obsessed with silver. Stored in remote vaults, silver would be harder for a government to seize. The metal was also a hedge against soaring inflation in the 1970s.

Hunt and his brother William began buying silver at roughly $3 per ounce.

They bought futures contracts – agreements to buy silver at a set price on a future date.

Most traders close or roll their futures positions before the contracts expire. The Hunt Brothers, on the other hand, took advantage of the physical delivery option. They gradually amassed a huge silver position, depleting silver inventory at the COMEX (officially called the Commodity Exchange) and the Chicago Board of Trade.

Fearing U.S. government confiscation, the Hunt Brothers shipped some of their silver to vaults in Switzerland and London.

In 1979, the Hunt Brothers joined forces with two Saudi Arabian Sheikhs to form an international company that would buy even more silver.

According to an SEC report, the Hunt Brothers and their Saudi partners amassed control of roughly 200 million ounces of silver. Around half of that was physical silver and half was exposure via futures contracts.

To put their silver hoard in perspective… A COMEX-approved silver refinery estimated that total U.S. silver inventory (bullion), including government and private holdings, totaled 340 million ounces. The Hunt Brothers had nearly cornered the U.S. bullion market. But the overall silver market was much larger.

Global bullion inventory was estimated to be around 1.3 billion ounces. On top of that, there were billions more ounces of silver in silverware, jewelry, and coins.

Nonetheless, the Hunt Brothers and their co-conspirators had grossly distorted silver prices.

Heading into 1979, silver’s spot price was around $6. By the end of that year, it was $32 and rising rapidly.

If only the Hunt Brothers had stuck to acquiring physical silver and skipped the leveraged futures speculation, they would have been fine. But they had borrowed money using their silver stockpiles as collateral to buy more futures. It was pure greed and recklessness.

The COMEX took increasingly aggressive actions to keep the futures market functioning properly. The exchange raised initial margin requirements (the upfront deposit) and then imposed position limits.

Silver’s surge continued. On January 18, 1980, silver reached nearly $50 per ounce. The spot price was up more than 900% since the beginning of 1978.

Then, after an emergency meeting on January 21, the COMEX board went nuclear… Silver futures trading would be “liquidation only.” Basically, no one could add to, only reduce their positions.

When the market opened, silver dropped by 30% in two days. By the end of March, silver was trading below $15. The Hunt Brothers were unable to meet margin calls, and their futures positions were liquidated.

In 1988, a federal jury found the Hunt Brothers guilty of conspiring to manipulate the silver market. Nelson Bunker Hunt declared personal bankruptcy following the trial.

Despite a few brief spikes, the price of silver languished for more than two decades. And thus, the grand suppression conspiracy theory was born.

Silver’s Latest Margin Hikes

Silver’s next great secular bull market began in 2001 at around $4 per ounce. After falling by more than 50% to around $9 during the global financial crisis in 2008, silver recovered and started going parabolic in early 2011.

Once again, the COMEX, then owned by CME Group (CME), raised futures margin requirements. These included five hikes in nine days between April 26 and May 9.

Silver’s peak of nearly $50 per ounce in late April 2011 coincided with those margin hikes. The price of the metal collapsed by 30% within weeks and entered a nine-year bear market.

Margin increases aren’t nefarious, though. This is not manipulation. The COMEX is just managing its risk.

Futures can be dangerous financial instruments. Their inherent leverage amplifies gains but also losses, as the Hunt Brothers’ saga illustrates.

The COMEX’s clearinghouse, now part of CME Group, serves as an intermediary, stepping into the middle of each matched futures and options trade. That way, traders don’t have to worry if other traders blow themselves up.

The clearinghouse is the central counterparty that assumes the risk of clearing member defaults and acts as a backstop.

To mitigate its own exposure and the risk of widespread defaults, the clearinghouse collects initial and maintenance margin.

Historically, the margin requirements for precious metals have been dollar amounts. When silver prices rise, the clearinghouse faces more risk. That’s why the exchange periodically hikes margins.

Margin adjustments happen routinely and are often gradual. And there are margin decreases, too, when volatility subsides.

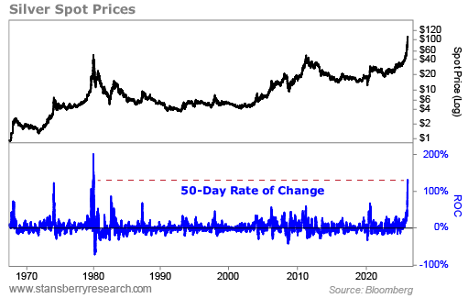

Over the past few months, silver has skyrocketed. It was up as much 130% over 50 trading days. Only the silver spike in late 1979 and early 1980 can compare.

Naturally, the CME Group has raised margin requirements. But it’s trying something different.

On January 13, the exchange shifted from a flat dollar margin to a percentage of the contract’s total value for gold, silver, platinum, and palladium.

Initial margins for 5,000-ounce silver futures contracts went from $32,500 to 9% of the contract value. (High-risk accounts have slightly higher margins.) The exchange raised margins again to 11% effective January 28.

Theoretically, there will now be fewer margin changes, as the margins will now scale with the price of the underlying metal.

Get Ready for More ‘Paper’ Silver

The COMEX became part of the world’s largest derivatives exchange operator when the CME Group acquired the COMEX’s parent company, the New York Mercantile Exchange, in 2008.

Under the wing of CME Group, the COMEX has become the premier global, electronic precious metals derivatives marketplace.

Volumes for COMEX’s benchmark 5,000-ounce silver futures contract have grown steadily. This is the same type of contract that the Hunt Brothers were trading. And there’s still a physical settlement mechanism.

The COMEX now also has “e-mini” and “micro” silver futures, representing 2,500 ounces and 1,000 ounces, respectively. The micro silver futures allow for physical delivery while the e-mini contracts are only cash-settled.

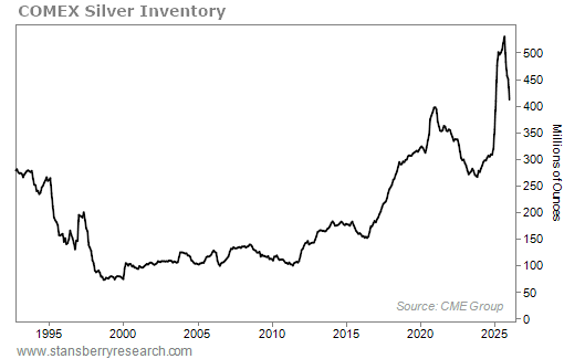

Despite fearmongering about silver vaults emptying, there’s currently more than 400 million ounces in COMEX-approved bank and security firm vaults. All the silver in these vaults meets the COMEX futures delivery standards (whether it’s categorized as eligible or registered).

There’s less silver in these vaults now than there was last September. But there’s still far more inventory than there’s been in the past.

Granted, silver futures open interest is about 160,000 contracts, which represents about 800 million ounces. That’s about double the amount of physical silver in COMEX vaults.

Yet, this isn’t a problem because the COMEX is primarily a market that facilitates the transfer of risk, not physical metal. Silver buyers can hedge their exposure. Silver miners can lock in future prices to sell their production. No physical metal needs to change hands for hedging to work.

Typically, less than 1% of expiring contracts stand for delivery. And if the futures price were artificially low, then that percentage would be a lot higher.

Of course, a lot of speculation also takes place on the COMEX. And the CME Group wants even more of this volume.

In 2025, CME Group partnered with retail broker Robinhood (HOOD) to launch futures trading. Now, you can trade gold and silver futures through the Robinhood app.

There’s so much demand for paper silver that the CME Group is also launching a 100-ounce silver futures contract in early February. This contract is directed at retail traders and will only be cash settled.

Many doomsayers act like CME Group is somehow getting killed as precious metals go through the roof. Rather, the recent surges in silver and gold have been great for CME Group’s business.

Every time a derivative contract trades, the exchange gets a small fee. So, whether commodities go up or down, CME Group benefits. Plus, trading volumes tend to rise with volatility.

In other words, the “house” always wins.

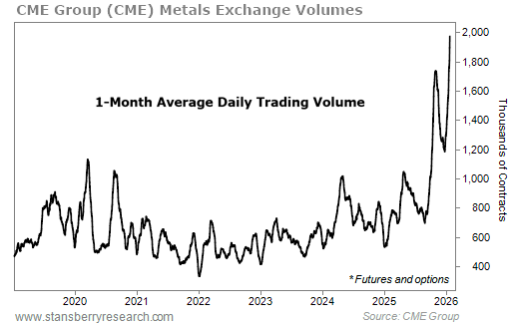

The following chart shows rolling 1-month average daily volumes (“ADV”) for CME Group’s metals segment (including futures and options).

These derivatives volumes include trading in silver, gold, platinum, and palladium, as well as base metals, such as copper.

On January 26, the day silver first reached $117 per ounce, combined metals volumes reached a record of nearly 3.4 million contracts. And 1-month ADV has exploded to nearly 2 million contracts, thanks in large part to frenetic trading in silver and gold derivatives.

CME Group’s metals franchise is on fire.

The grand suppression conspiracy theory about silver is convenient.

However, the paper silver market isn’t collapsing. Margin hikes aren’t market manipulation. And there’s plenty of silver in the COMEX vaults.

So, what does all this mean for investors today?

Don’t Be Surprised When Silver Crashes

Silver’s bull market is underpinned by simple economics…

Silver mining supply has stagnated. Meanwhile, demand grows from industrial uses, such as solar panels and electric vehicles. Our Commodity Supercycles team has been covering this growing imbalance in the silver market for years.

There are other reasons to be bullish on silver, including a global sovereign debt problem and a relative weak U.S. dollar.

However, as they often say in commodities markets, the cure for high prices is high prices.

And let’s be honest… Silver’s recent move is extreme. It reeks of panic buying and speculation. And if history is any guide, the farther and faster it rises, the larger the fall will be.

Have a plan, trade safely, and resist the fear of missing out… especially if you’re a long-term investor.

When silver’s momentous surge does come to an end and the price crashes, people will blame the paper shorts and the banking cartel. But it’s just normal volatility in the notoriously wild commodities markets.

Good investing,

Alan Gula, CFA

Editor’s Note: Gold has already shattered records this year…

But Stansberry Senior Partner Dr. David “Doc” Eifrig says history shows it could be on the verge of its biggest bull run in over half a century.

His research shows it could be triggered by a major event, eerily similar to what happened in the 1970s. It’s NOT inflation, fed rate cut expectations, escalating geopolitical tensions, or anything you’re likely expecting.

And Doc believes you MUST own shares of his top gold stock.

He says you could 10x your money without touching a risky miner or a boring exchange-traded fund.

It’s the centerpiece of Doc’s full gameplan for this wild market, with extraordinary upside potential.

Click here for the full details on this developing gold story.