AI, bitcoin, autonomous technology… these topics have been dominating the market headlines. A major reason why is their volatility.

For example:

- Advanced Micro Devices (AMD) closed at $259.68 on January 23. On February 5, it closed at $192.50.

- On September 10 of last year, Oracle (ORCL) closed at $328.33. On February 5, ORCL closed at $136.48.

- Microsoft (MSFT) closed at $481.63 on January 28. Just over a week later, it closed at $393.67 on February 5.

That’s tech investing in a nutshell. And it’s why some investors are hopping off the tech rollercoaster and onto something far more stable…

Namely, consumer staples. Think food, beverages, personal care items, and cleaning supplies.

They may not be the most exciting stocks, but investors can rely on the stability that consumer-staples companies offer. Because no matter the economic conditions, we need those products daily.

That’s why consumer-staples stocks represent such a solid bet. They’re durable, reliable, and set up for long-term success… not short-term bursts.

Why Consumer-Staples Stocks Are Known for Stability

Consumer-staples stocks are the companies that make, package, and sell these items.

For food, they consist of grocery stores, big-box stores, drugstores, and distributors. With beverages, there are soft-drink makers, brewers, winemakers, and distillers (yes, alcohol is considered a consumer staple).

For household products, it’s the companies making and selling cleaning supplies and laundry essentials. Personal care covers hair products, skin care, dental hygiene, and cosmetics. Even tobacco products are considered consumer staples.

The demand for these types of products is noncyclical, so it remains consistent even during challenging economic times.

Why? Because we need these products.

These are not discretionary items purchased with disposable income. They’re the essentials we buy before we spend on anything else. And that keeps demand steady.

That consistent demand often drives consumer-staples stocks to outperform cyclical stocks, like tech, during times of economic stress. And most of these companies pay consistent dividends thanks to steady revenue and cash flow, no matter the economic conditions, making them popular defensive plays among investors.

The “Blue Chip” Consumer-Staples Leaders

Today, we’ll focus on some “blue chip” consumer-staples stocks… companies you likely know well. They all have long, successful track records. And they own, make, and sell many of the household brands you use and trust.

These stocks also deliver consistent dividends to their shareholders, making them solid anchors in many investors’ portfolios.

Procter & Gamble (PG)

You’re probably at least somewhat familiar with the company. But you certainly know Procter & Gamble’s brands: Tide, Pampers, Gillette, Downy, Bounty, Charmin, Puffs, Old Spice, Cascade, Dawn, Febreze, Swiffer, Crest, Oral-B, Vicks, Olay… and there are plenty more.

P&G’s brand portfolio is nearly unrivaled. The company has a reputation for being highly influential (one of Time magazine’s 2025 100 Most Influential Companies) and forward-thinking (one of Fortune‘s America’s Most Innovative Companies).

And the 2024 Advantage Report Global Scorecard ranked P&G the No. 1 manufacturer for the 10th straight year.

P&G has established itself as a Dividend King – a company that has increased its dividend payout for at least 50 consecutive years. It has been 69 straight years for P&G, one of the longest streaks of consecutive annual dividend increases ever. (P&G paid $9.9 billion in dividends during fiscal 2025.)

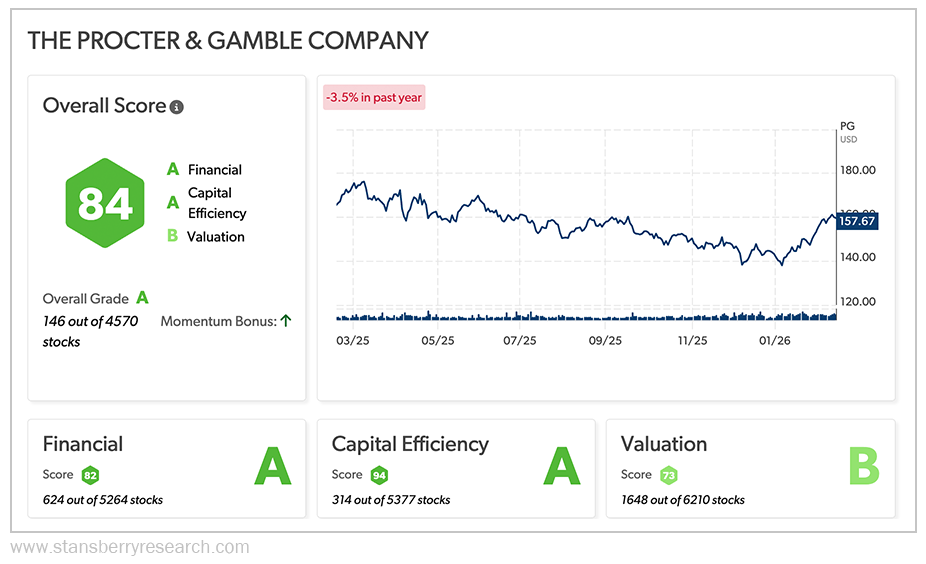

P&G’s stock did take a hit in January due to challenging market conditions. But it rebounded from its 52-week low of $137.62 to trade at roughly $160 by February 13.

The decades of increasing dividend payouts show how resilient P&G has been through all types of economies. And its Stansberry Score, a tool that helps investors determine the quality and long-term value of a stock, reflects a highly respected and resilient company.

Stansberry grades PG as an overall “A”… ranking the company within its top 150 stocks, giving PG an “A” in Financial and Capital Efficiency and a “B” in Valuation.

General Mills (GIS)

Another recognizable and highly respected company, General Mills can claim “ownership” of both the breakfast-cereal bowl and the pet-food bowl. Its breakfast brands include huge names like Cheerios, Lucky Charms, Chex, Cinnamon Toast Crunch, and Cocoa Puffs. Meanwhile, Blue Buffalo is General Mills’ flagship pet brand.

Of course, General Mills offers an even wider range of consumer staples. Baking brands like Pillsbury, Betty Crocker, and Bisquick are all owned by the company. And shopper favorites like Green Giant, Nature Valley, Häagen-Dazs, and Old El Paso are also part of the General Mills portfolio.

But right now, General Mills is focused on its pet segment, with Blue Buffalo as the revenue driver. Why? Because the trend of “humanizing” pets and pet food is a consistently growing, multibillion-dollar movement.

Today, people don’t simply treat pets as animals. They’re seen more as “fur babies” and faithful companions. And, as such, they deserve food more befitting of humans… not mush from a can or pellets from a bag.

More pet parents are spending on premium food made with “human grade” natural or organic ingredients to improve their pets’ wellness and health.

So much so that research from Technavio has projected the U.S. fresh pet food market to grow by $3.2 billion at a compound annual growth rate (“CAGR”) of 21.2% through 2029. And General Mills is well positioned to take advantage of this growth.

By early 2026, General Mills had achieved its goal of placing 5,000 coolers in retail stores to hold Blue Buffalo’s new “Love Made Fresh” line. And in 2024, it acquired Whitebridge Pet Brands and European pet brand Edgard & Cooper to expand its pet portfolio.

General Mills is all-in on pet food as a consumer staple. And research backs up the company’s bet. A recent survey from Talker Research revealed that 65% of pet owners would cut their own lifestyle budgets before cutting their pet’s. And 66% responded that they shell out for high-quality pet food.

That equals consistent, economy-proof revenue for General Mills.

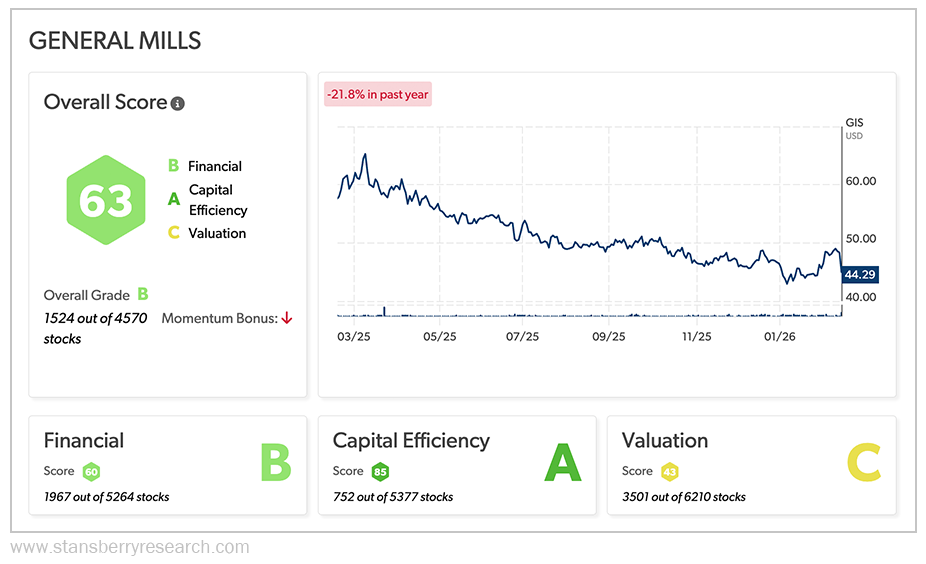

On February 17, General Mills lowered fiscal 2026 sales and profit guidance, which pushed GIS shares down nearly 7%. This lower share price caused its dividend yield to rise… as of February 19, the dividend yield was roughly 5.4%. This led some analysts to classify GIS as undervalued. The stock trades at a lower price-to-earnings (“P/E”) ratio of around 10 when compared with the food industry’s roughly 44.1 P/E ratio.

This all contributes to GIS’s undervaluation. And that means investors can grab General Mills at a discounted price.

The Stansberry Score for GIS doesn’t undervalue the stock as much as other analysts, giving it a “C” in Valuation. But it’s strong elsewhere, with an “A” in Capital Efficiency and a “B” in Financial.

General Mills is a consumer-staples stock by any definition. But it’s also a bit of a contrarian play thanks to its high dividend yields caused by lower stock prices rather than strong dividend growth. That makes GIS an attractive, value-oriented option for longer-term income… counter to bearish market sentiment.

Philip Morris International (PM)

Classifying tobacco products as consumer staples may seem odd. But tobacco has one thing in its favor… addictiveness. For that reason, tobacco items are considered staples.

Philip Morris International is the leading cigarette manufacturer in the U.S., thanks in large part to its massive Marlboro brand. However, PM’s prescient decision to pivot away from cigarettes is what sets the tobacco giant apart from its competition today.

In 2008, PM began exploring smoke-free alternatives to cigarettes. Since then, the company has invested $16 billion in the research, development, and marketing of smoke-free products. In fact, Philip Morris International is aiming to be primarily smoke-free by 2030.

It’s fair to wonder whether a tobacco company can succeed as a smoke-free business. But PM has figured out a way. Here’s proof:

- As of December 31, 2025, 42% of PM’s total global net revenue came from smoke-free products. It’s aiming for at least 66% by 2030.

- PM estimates around 43 million legal-age consumers use its smoke-free items.

Currently, PM’s portfolio of smoke-free products includes heated tobacco (also known as “heat-not-burn”) line IQOS, VEEV e-cigarettes (vapes), and ZYN nicotine pouches. And, like cigarettes, these smoke-free items are considered consumer staples because they all contain nicotine.

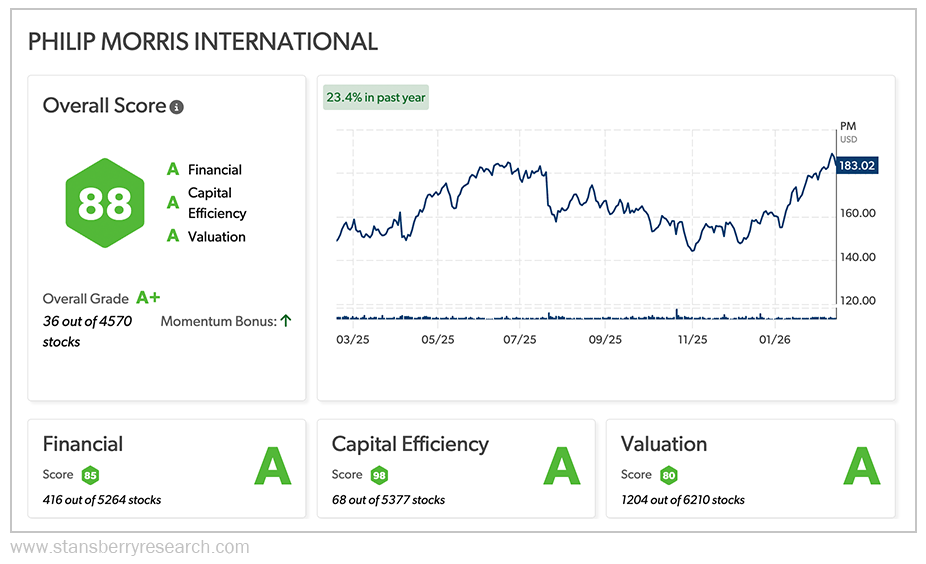

The push toward a primarily smoke-free business is paying off for PM… and its investors. The company has offered significant dividend yields (between 3.28% and 3.6% over the past year) thanks to its industry-leading profitability (roughly $40.6 billion in total revenue and $27.3 billion in gross profit for fiscal 2025) and its successful shift toward smoke-free items.

PM’s Stansberry Score is stellar. It earns an “A+” overall grade and ranks within Stansberry’s top 40 stocks. It has straight “A” scores in Financial, Capital Efficiency, and Valuation.

While its competitors still rely on flagging cigarette sales, Philip Morris International wisely pivoted… and it’s paying off. Income-focused investors seeking consistent dividend increases and long-term growth should have PM on their watch lists.

Retail and Distribution Consumer Stocks

Affordability is on the minds of most Americans these days. According to a University of Michigan study, consumer confidence over the past few months is at its lowest point since the height of the inflation crisis in June 2022.

Even top earners aren’t immune to affordability struggles. A recent Harris poll noted that nearly 33% of six-figure earners consider themselves stretched, struggling, or drowning financially.

During challenging times, consumers often look to stretch their budgets with bargains and value-priced items. A couple of businesses stand out in this regard.

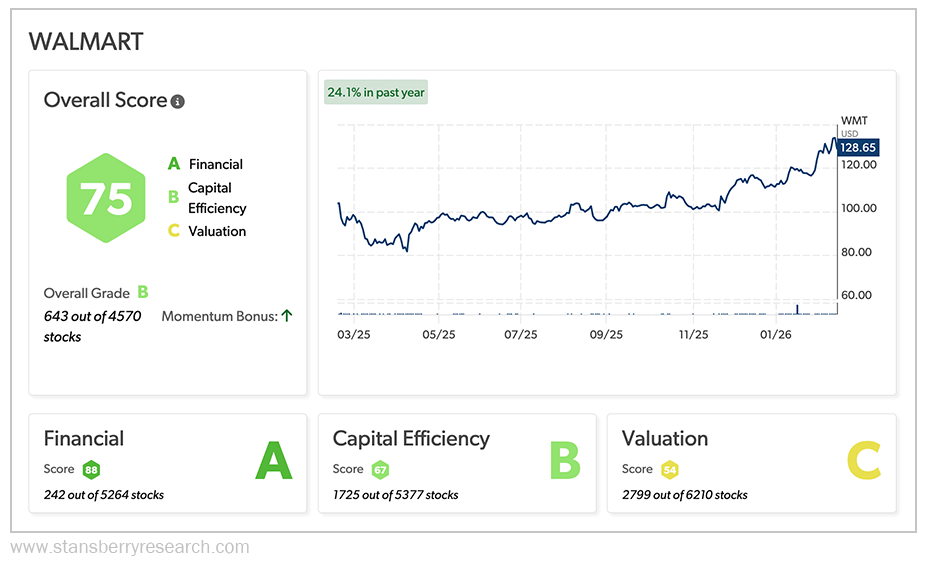

Walmart (WMT)

When the economy flags, Walmart thrives. During the third quarter of fiscal year (“FY”) 2026, Walmart’s U.S. sales spiked roughly 5% as more consumers shopped for value-driven deals. But it’s not just lower- and middle-income shoppers looking for great deals at Walmart.

“We continue to benefit from higher-income families choosing to shop with us more often,” said Walmart’s president and CEO, Doug McMillon, during the company’s fiscal third-quarter earnings call.

In fact, according to RetailWire, “wealthier shoppers have been pushing Walmart’s growth for several years, with many attributing the gains to consumers trading down amid inflationary pressures.”

McMillon noted that shoppers from households earning $100,000-plus accounted for 75% of Walmart’s market share gains in Q3 2025.

When it comes to prices, Walmart just gets it. The retail giant pledged to keep prices from rising as long as possible, even if it meant absorbing higher costs brought on by President Trump’s tariffs.

Walmart’s grocery business helps set it apart from other retailers. During Q3 of fiscal 2026, Walmart initiated around 7,400 rollbacks – the company’s signature 90-day price reductions – and more than half were on groceries.

It’s these prices and values that entice middle-income – and even high-income – shoppers to spend at Walmart. This type of trade-down shopping gives the company a solid defensive moat that can protect its business even during difficult economic conditions.

As far as investing in Walmart, the company is in outstanding financial shape thanks to a $1 trillion market cap and robust revenue. Walmart topped $680 billion in revenue in the first three quarters of fiscal 2026.

But there is some concern around its valuation. WMT shares are pricey, so there could be a pullback ahead.

Walmart’s Stansberry Score reflects these sentiments. Overall, the stock is solid, earning a strong “B.” This is driven by its excellent Financials (“A”) and solid Capital Efficiency (“B”). But its Valuation gets a “C.”

Its trailing-12-month (“TTM”) P/E ratio is astronomical – especially for a retailer – at nearly 47, suggesting significant overvaluation. (For comparison, the S&P 500’s five-year average is 25.)

Yes, WMT is a “safe haven” stock, and it’s treated as such by investors. That’s one reason its valuation is so high. But Walmart’s revenue growth is typically in the single digits, leading some investors to believe its shares are overpriced.

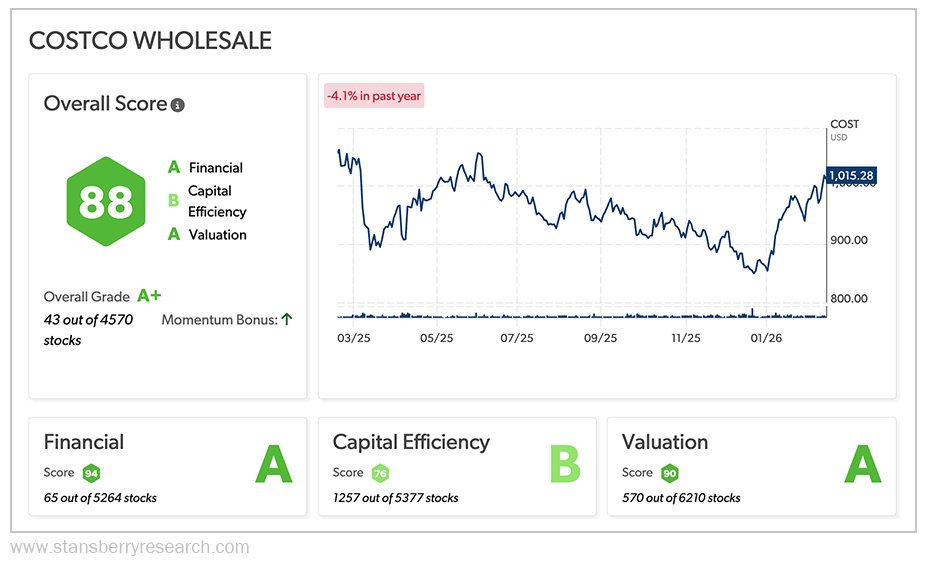

Costco Wholesale (COST)

Costco and Walmart share some similarities. They both appeal to value-driven shoppers. They’re both consistently profitable. Both companies have loyal customer bases. And they’re both considered defensive safe havens by investors.

But there are a few notable differences. For one, Costco solely operates on a membership-based model. This makes the company a defensive stock for a different reason than Walmart: Costco can rely on membership fees – not just the items it sells – to generate reliable revenue.

Walmart does use a membership model with its Sam’s Club wholesale stores and its Walmart+ offering. But the Walmart+ member base of 28.4 million as of January pales in comparison with Costco’s roughly 145.2 million cardholders in fiscal 2025. Even with Sam’s Club members added in (estimated at around 69 million in 2023), Costco’s membership count is significantly higher.

One more similarity… Costco’s P/E ratio is extremely high – even higher than Walmart’s. Costco’s TTM P/E ratio is more than 55, which is eyebrow-raising. But there’s a reason for that. Costco’s high P/E ratio is driven by investors who are willing to pay more for a stock that relies on a high-margin membership model, intense brand loyalty (members renewed at a 92.2% rate in the U.S. and Canada in the most recent quarter, international expansion, and consistent earnings growth that’s often approaching or well into the double-digit range.

Walmart, on the other hand, works within tighter margins. And it can’t depend on the same level of membership fees or revenue growth that Costco does.

The result? COST is worth its lofty price tag as a premium stock, while WMT is overvalued.

COST’s Stansberry Score bears that out. Overall, COST ranks well within the top 50 stocks with an “A+” grade. That’s backed up by its outstanding scores (“A”) for Financial and Valuation and a “B” in Capital Efficiency.

Consumer Staples ETFs for Diversification

If you’re seeking more diversification in your investments, there are a couple of exchange-traded funds (“ETFs”) worth looking into.

Consumer Staples Select Sector SPDR Fund (XLP)

This ETF is ideal if you want to invest in some consumer-staples giants without investing in each company individually.

XLP is a solid bet, as its 36 stocks are heavily focused on companies like Procter & Gamble, Costco, Coca-Cola (KO), Philip Morris International, PepsiCo (PEP), Mondelez International (MDLZ), and other safe-haven companies. The fund surged to $90.00 on February 13, before closing at $89.51… its all-time closing high. XLP’s low expense ratio of 0.08% and strong dividend yield of around 2.5% make this ETF a smart, diversified way to invest in consumer staples without tying too much risk to one individual stock.

Vanguard Consumer Staples Index Fund (VDC)

If you’re really looking to diversify, the Vanguard Consumer Staples Index Fund includes more than 100 stocks. Not just the giants, like those in XLP (many of which are also in the VDC fund), but also mid- and small-cap companies like Utz Brands (UTZ), Seneca Foods (SENEA), and Honest (HNST).

VDC’s expense ratio of 0.09% is similar to XLP’s, while its dividend yield has hovered in the 2% to 2.5% range for about a year. And like XLP, VDC reached two all-time highs on February 13, peaking at $244.00 and closing at $242.63.

VDC is perfect for investors who want to bet on a bigger slice of the consumer staples sector, from established giants to smaller companies still finding their way.

Consumer Staples Trends to Watch in 2026

Even defensive stocks like consumer staples are subject to risk. Here’s what investors should watch for throughout 2026:

Valuation Risk

- Keep an eye on high P/E ratios. If those valuations aren’t supported by rapid earnings growth, those stocks could plummet.

- Defensive stocks like consumer staples can become overvalued as more investors pile into them during challenging times.

Input Cost Pressures

- Costs are increasing across the board. Tariffs, material costs, fuel prices, supply shortages, rising wages, and labor shortages are contributing to the rising costs of making, packaging, shipping, and selling goods.

- While strong brands are better able to shield customers from these increasing costs, it’s important to watch whether some businesses reach a breaking point.

Pricing Power vs. Volume

- Retailers like Walmart have successfully fended off price increases, even as their operating costs grow, but how long will that last before these companies are forced to raise prices? If that happens, will consumers keep flocking to stores like Walmart and Costco?

- This puts consumer staples retailers in a difficult position. Either they maintain low prices while paying more for goods, which severely impacts their profit margins, or they raise prices accordingly and risk losing volume and customer loyalty, which also hurts profitability.

Interest Rates and Dividend Sensitivity

- Keep a close eye on interest rates. If they rise, companies are faced with increased borrowing costs that can cut profitability and impact their stock prices.

- Plus, when interest rates rise, safer investments like Treasury bills and bonds can become more attractive to investors. And that creates competition between dividend stocks and other types of investments.

Bottom Line: Balancing Growth with Stability in 2026

Consumer-staples stocks aren’t likely to deliver sudden bursts of growth. Instead, they offer reliable demand and pricing power to investors who seek long-term gains.

No one is going to get rich quick from consumer-staples stocks. But they should consistently produce strong dividend yields that can help you stay rich down the road.

If you’re looking for a solid anchor for your portfolio, consumer-staples stocks are proven winners that withstand market volatility and endure – or even thrive – during difficult economic periods. They may not generate the same headlines as flashier tech stocks, but consumer-staples stocks are the ones that will weather the storm.

Regards,

David Engle

Editor’s note: What should you invest in right now?

A renowned former hedge fund founder and his research team have found what they believe is the next big tech trend that could make investors rich.

It’s a breakthrough they’re calling “Helios” – and if you haven’t yet heard of it, you soon will.

Over the next few years, it could impact the food you eat… the water you drink… the places you live and work… and even the prices you pay for airfare, gas, electricity, and household goods.

“Helios” is going to cause a lot of people to lose money, too. Dozens of well-known businesses could go bankrupt.

But if you own a stake in this new tech, the positive effects will far outweigh the negatives. Get the facts for yourself. Make sure you’re not on the wrong side of this trend. Click here to see this new analysis…