Goldman Sachs upgraded Netflix stock from neutral to buy on Monday. The banking giant also raised its 12-month price target from $100 to $120, signifying 20% potential upside.

In late February, Netflix (NFLX) was poised to acquire Warner Bros. Discovery (WBD) for nearly $83 billion. Then Paramount Skydance (PSKY) swooped in with an offer of roughly $110 billion.

As a result, Netflix walked away from the deal. And that might have been the best move Netflix could make (or not make).

So, why the upgrade from Goldman? And is now a good time to consider buying Netflix stock? Let’s dig in.

Netflix Stock Plunges After Initially Acquiring Warner Bros. in December

On December 5, 2025, Netflix announced it had acquired Warner Bros. Discovery. That day, the stock closed at $100.24. By December 10, Netflix shares had sunk to $92.71… a roughly 7.5% drop.

By February 12 of this year, Netflix shares were down to $75.86 – a sharp decline of nearly 25% since the initial merger news.

Why the plunge?

Analysts had a few reasons to believe the acquisition of Warner Bros. would hurt Netflix more than it would help.

- The reported purchase price could result in growing debt and put a clamp on Netflix’s free cash flow.

- Netflix has always been considered an entertainment innovator because of its “build vs. buy” strategy. Buying Warner Bros. Discovery would run counter to that strategy, raising doubts about Netflix’s long-term roadmap.

- Any media acquisition of this magnitude draws intense regulatory scrutiny and uncertainty, which could cast a potentially negative spotlight on Netflix throughout the acquisition process.

That scrutiny actually began immediately after the December 5 merger announcement. There was talk of a Department of Justice review of the deal amid “heavy skepticism” from President Donald Trump’s administration.

And lawmakers in Congress voiced concerns about whether this deal would create a streaming monopoly that might slash jobs and raise subscription prices.

The scrutiny continued through much of February, enough to keep Netflix shares in the $75 to $80 range.

Netflix Stock Soars After Walking Away From WBD Deal

Then on February 26, Netflix officially declared that it was pulling out of the Warner Bros. Discovery deal upon learning about the Paramount Skydance offer.

In a statement, Netflix co-Chief Executive Officers Ted Sarandos and Greg Peters said:

The transaction we negotiated would have created shareholder value with a clear path to regulatory approval. However, we’ve always been disciplined, and at the price required to match Paramount Skydance’s latest offer, the deal is no longer financially attractive, so we are declining to match the Paramount Skydance bid.

Wall Street’s response? Netflix stock spiked 10% in extended trading that day, closing at $82.74.

Analysts and investors widely applauded Netflix’s decision to back out of the deal. And that sentiment remained for more than a month. Netflix hit $100.19 during intraday trading on March 5.

But more headwinds were in store for Netflix.

Netflix Shares Tumble After Initial Wave of Optimism

Unfortunately for Netflix, reality set in once the market’s initial celebration of the abandoned deal died down.

Why the quick shift in sentiment?

For one, analysts took a step back to reassess Netflix after the deal fell through. Yes, Netflix would have faced a host of challenges, which we covered earlier, had it finalized its deal to purchase Warner Bros. Discovery.

But Netflix also would have owned WBD’s massive catalog of titles as well as a formidable streaming platform in HBO Max. Combined, it would be difficult for any competitor to top what Netflix and its new assets could offer.

Now, Netflix faces the same challenge its competitors would have faced if Netflix successfully acquired Warner Bros. Paramount Skydance is set to get the WBD catalog and HBO Max on top of its own services, which include Paramount+ and Pluto TV streaming, Showtime, CBS, Comedy Central, MTV, Nickelodeon, and, of course, Paramount Pictures.

As a result, Netflix’s streaming competition just got much stiffer.

Analysts also found other reasons to be nervous about Netflix’s prospects.

Costs for sports rights and talent for Netflix’s original productions continue to rise. And Netflix forecasted $20 billion in content expenditures for 2026, raising concerns about the company’s margin and profitability for the year.

To counter those concerns, Netflix raised subscription prices and focused more on generating advertising revenue. Starting on March 26, the streaming giant upped its monthly rates by $1to $2 across all its plans.

Between March 5 (the day Netflix walked away from the deal) and the end of the month, Netflix shares had fallen 3%.

But Netflix bounced back.

Goldman Sachs Upgrade Propels Netflix Stock Again

After Goldman’s upgrade announcement, Netflix stock jumped roughly 2% during morning trading on April 6, cracking $100 for the first time since March 5.

Goldman analyst Eric Sheridan stated that Netflix should achieve double-digit revenue growth over the next three to four years thanks to a variety of factors:

- High-margin ad revenue, which is projected to double to $3 billion this year (and to at least $8 billion by 2030), thanks to Netflix’s proprietary in-house ad-tech platform that kicked off in late 2025

- Those aforementioned price hikes, which could add another $1.7 billion in annual revenue

- Expectations that Netflix will put capital toward content development, including an increased focus on live entertainment (such as NFL Christmas Day games, WWE Raw wrestling, boxing, Major League Baseball Opening Day, comedy shows, the Screen Actors Guild Awards, and other live content)

- The return of significant capital (perhaps up to 25% of Netflix’s market cap) to shareholders over the next few years, driven in part by the hefty $2.8 billion “breakup fee” Netflix received from Paramount Skydance

Goldman’s Sheridan also predicts Netflix will achieve 250 basis points of annual generally accepted accounting principles (“GAAP”) operating income margin expansion over the next three years.

Those projections bode well for Netflix’s stock.

Is Netflix’s Stock a Buy?

Over the past five years, Netflix shares have increased roughly 81%.

Even over the past year, despite plenty of highs and lows, Netflix is up nearly 14%.

These are generally the types of gains you see from forward-thinking companies with strong customer bases and consistently solid financials.

In Netflix’s case, its performance is fueled, in part, by its ad-supported model.

On the surface, skepticism about a plan counting on ads to increase subscriber count would be a normal reaction.

But the plan worked.

Netflix’s ad-supported plans were created in the wake of Netflix losing roughly 1.2 million subscribers in the first half of 2022. That included nearly one million alone in 2022’s second quarter – the largest subscriber loss in Netflix’s 25-year history.

But subscribers, motivated by the lower monthly price of ad-supported plans, started to buy in. By early 2023, the company’s ad-supported tier had five million active users globally. By May 2024, that number hit 40 million. And by the end of 2025, there were around 190 million monthly active viewers subscribed to ad-supported plans.

Netflix’s ad-supported plans accounted for roughly 45% of total household viewing hours in the United States in 2025, up from 34% in 2024, according to Comscore’s 2025 State of Streaming report.

The concept was simple, but brilliant… if not entirely original. Netflix had long resisted offering ad-supported plans, even as its competitors were implementing them.

But Netflix was hemorrhaging subscribers, and something had to give.

Netflix gambled on the idea that, while most people don’t like ads, they will tolerate them for a lower monthly price.

Netflix won that bet. Its ad plan has unquestionably been a success.

The company stands to make even more from ad revenue moving forward. Not only from its ever-growing base of ad-supported plan subscribers. But because Netflix created its own ad-tech platform. And that eliminated Netflix’s need to share revenue with Microsoft (MSFT) for its ad sales, as it had been doing.

The result is improved margins, better ad value, and exponential ad-revenue growth, as we noted.

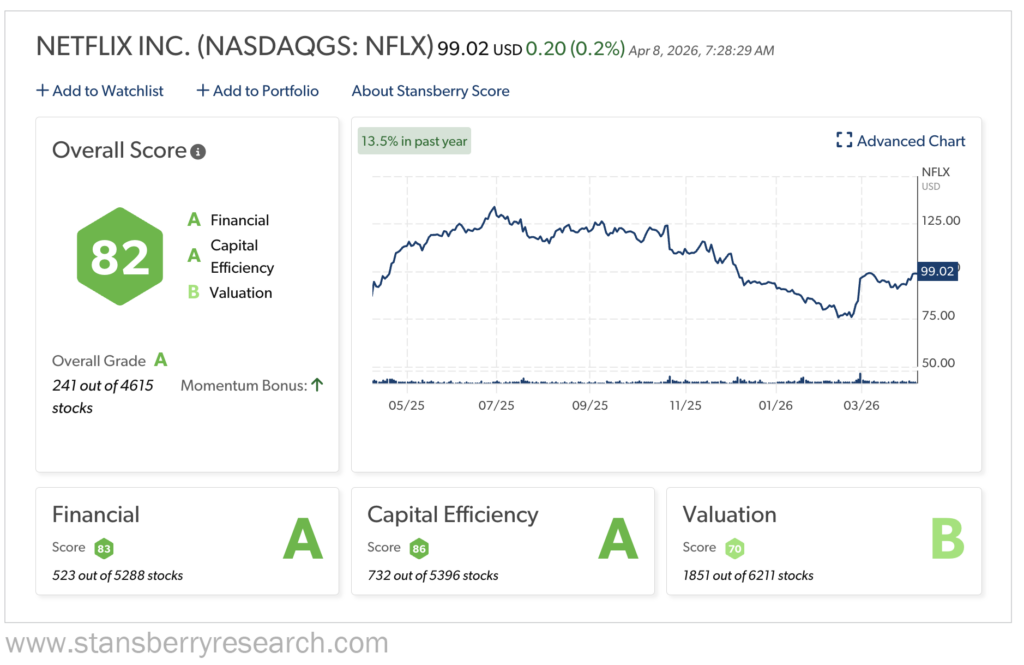

This is all reflected in Netflix’s Stansberry Score, which measures the long-term investment quality of a stock. Netflix ranks within the top 250 stocks overall, out of 4,600 total.

The company’s financials and capital efficiency are excellent (“A”). It’s easy to see why, considering Netflix earned roughly $45.2 billion in revenue in 2025, a 16% year-over-year (“YOY”) increase. Its net income was nearly $11 billion, and its operating margin grew three points YOY to 29.5%.

As noted earlier, Netflix’s ad revenue passed the $1.5 billion mark, a 2.5 times YOY jump. And the entertainment titan hit a milestone of 325 million paid subscribers last year.

The momentum continued into 2026. Here are some of Netflix’s projected first-quarter 2026 earnings report figures (they’ll be announced on April 16):

- Roughly $12.16 billion in revenue, a YOY increase of more than 15%

- 32.1% operating margin, up 40 basis points YOY

- $0.76 earnings per share (“EPS”), a YOY increase from $0.66

- Double the ad revenue of 2025 to $3 billion

So, does Netflix look like a good buy right now? Analysts are generally bullish, with a consensus rating of Buy based on the forecast of a 20% stock price increase in the next year.

As with any stock, however, proceed with caution. While Netflix certainly seems poised for a stellar 2026, it’s important to consider that the streaming giant has historically been a somewhat volatile stock.

Because its price reacts to subscriber growth (or loss), high levels of spending on content, and relentless competition from rival streaming services, Netflix is subject to swings. Just something to keep in mind if you’re looking to invest.

Netflix is resilient, however. Not many companies can walk away from a multi-billion-dollar mega-deal and exit the scenario in better shape. But that’s exactly what Netflix did.

Regards,

David Engle

Editor’s Note: Whitney Tilson — the hedge fund manager CNBC called “The Prophet” — says America has reached its “Ripping Point.“ The old financial order is being torn apart, and he believes most investors have no idea what’s coming in the next six months. He’s named the stocks he thinks will be destroyed in the chaos — and the ones he believes will soar. Watch his free presentation while it’s still available.

Recent Articles

IBM Wins Big With Trump’s Billion-Dollar Quantum Computing Bet – Here’s Why the Stock Soared

Broadcom’s AI-Chip Outlook Flashed a Major Warning Signal to Semiconductor Investors