The lithium market is often volatile, much like the element itself.

A look at the price of lithium carbonate – the compound used in lithium-ion batteries – illustrates as much.

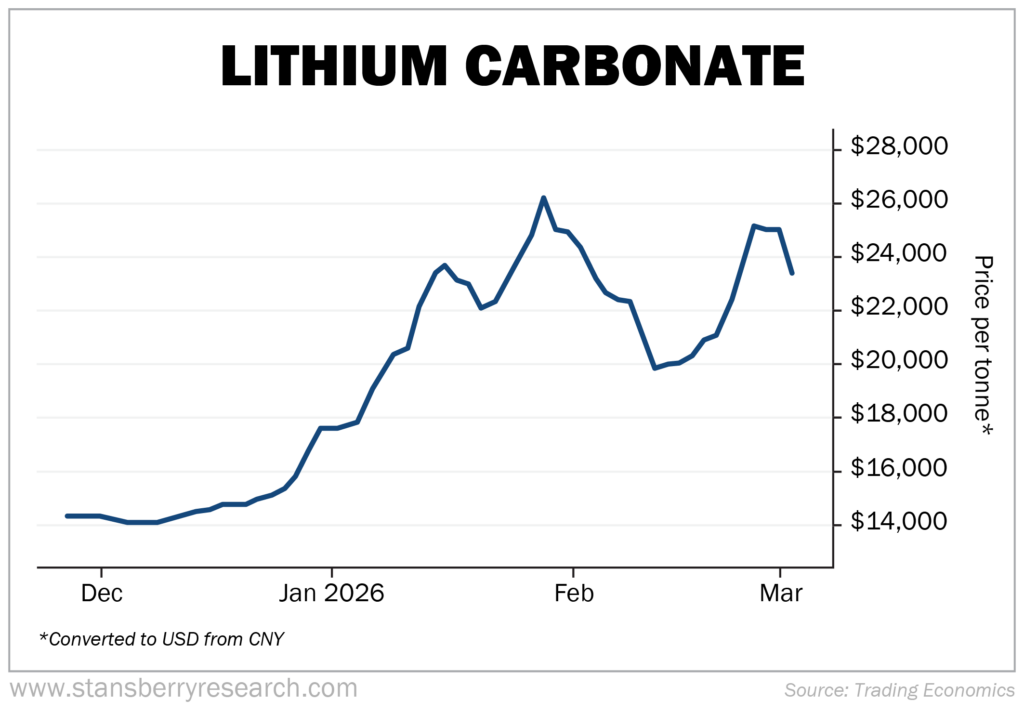

On December 31, lithium carbonate’s price hovered around $17,392. By January 26, the price had soared to $26,463 before plummeting to $19,733 on February 6. At the time of this writing, lithium carbonate has rebounded to $23,182.

The demand for lithium should keep rising as production of electric vehicles (“EVs”) and energy storage systems for data centers continues to increase.

There’s an important date on the horizon, however, that could impact the global lithium supply chain.

On April 1, China is cutting value-added tax (“VAT”) export rebates for batteries and similar components from 9% to 6%. By January 1, 2027, China plans to eliminate VAT export rebates altogether.

Why is this important? Because the majority (roughly 70%) of lithium refining and processing happens in China, which controls a critical piece of the supply chain. Even the world’s leading producer of raw lithium ore, Australia, exports virtually all of it (98%) to China for refining.

China’s policy will cause a global ripple effect. Costs will increase for importers as the 3% VAT rebate cut is passed onto them by Chinese lithium producers. In other words, China is essentially raising its “export tax” of refined lithium and finished battery products… likely resulting in higher battery prices.

In reaction to China’s VAT rebate change, battery buyers and importers will undoubtedly place more orders before April 1 to take advantage of the full 9% VAT rebate before it’s cut.

But that’s just one reason lithium stocks are attracting so much attention in 2026.

What Is a Lithium Stock?

A lithium stock is a company that participates in the lithium supply chain. This includes mining, refining, recycling, or developing the lithium used in batteries and energy storage systems.

Investing in lithium stocks isn’t a straightforward endeavor because they’re exposed to various parts of the supply chain.

There are the lithium miners and extractors. And the refiners that process lithium into battery-grade materials. There are also battery makers and manufacturers like EV and consumer-electronics companies that use the finished components in their products.

And each of these segments varies in stock performance because they each represent a different link of the supply chain.

For example, lithium mining stocks are commodity plays that experience high volatility due to fluctuating raw material prices. But the companies developing and building lithium batteries are more akin to tech stocks, because their prices are driven by margins and volume.

Let’s dig into the lithium supply chain to better understand the different types of investments available.

The Lithium Supply Chain Explained

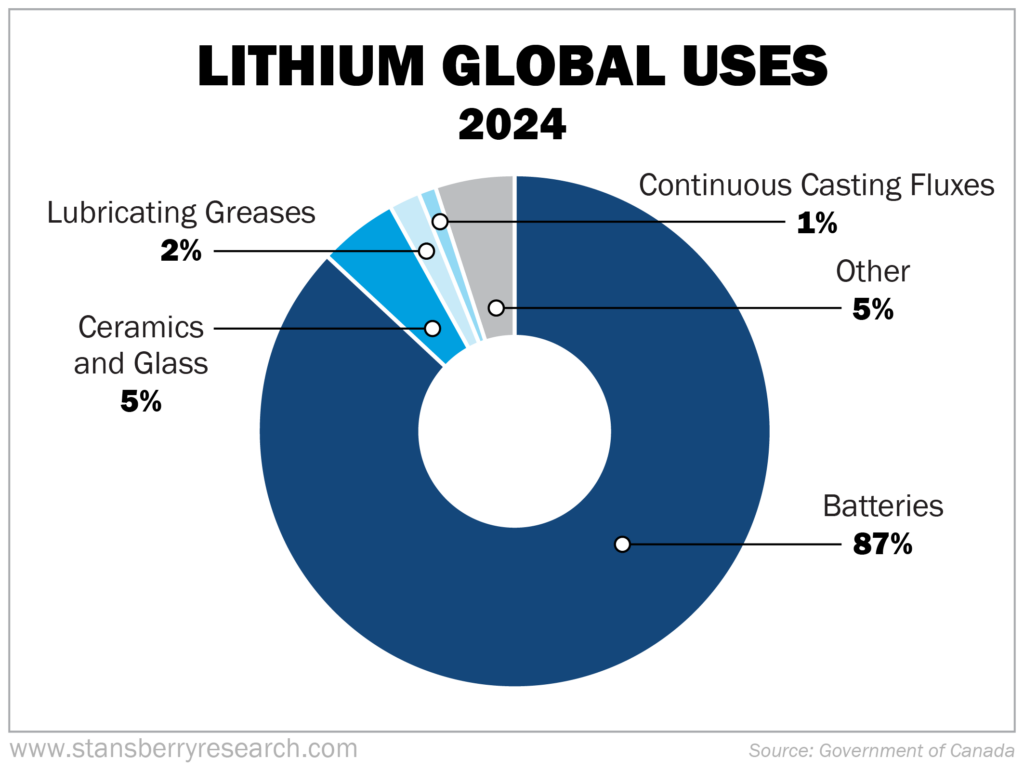

Batteries represent – by a huge margin – the leading global use of lithium (87%). With that in mind, let’s examine each segment of the lithium supply chain.

Because different companies operate in different parts of the supply chain, it’s important to understand how each segment responds to demand shifts, pricing, and policy.

Let’s start at the beginning…

Stage 1: Upstream – Mining Hard Rock and Extracting Brine

This is the first step of the process, when mining companies extract lithium from the ground. Lithium mining happens either through hard-rock spodumene mining or lithium brine extraction.

A quick explanation of each type:

- Hard-rock spodumene mining:This process involves mining lithium-rich spodumene ore from clusters of rocks and crystals. After mining, the ore is, per Lithium Harvest, “crushed, concentrated, roasted, and leached to obtain lithium concentrate.”

- Lithium brine extraction: There are a few ways to extract lithium from the brine found underground beneath salt flats and in geothermal reservoirs.

- Solar evaporation extraction: Lithium-rich brine is pumped into evaporation ponds. Sunlight then evaporates the water over a one- or two-year period, leaving behind concentrated lithium salts.

- Direct lithium extraction (“DLE”): With this process, lithium is extracted directly from brine sources or evaporation ponds.

- Extraction from geothermal brine: Geothermal power plants already pump brine from underground reservoirs to generate renewable energy. Lithium can be extracted from this same brine.

Once the raw lithium is extracted, miners often sell it to third-party refiners for processing. The success of lithium mining companies relies on a simple formula… If lithium prices rise, mining companies’ profits rise. If prices fall, profits shrink.

And, because lithium commodity prices are so volatile, lithium mining stocks follow suit.

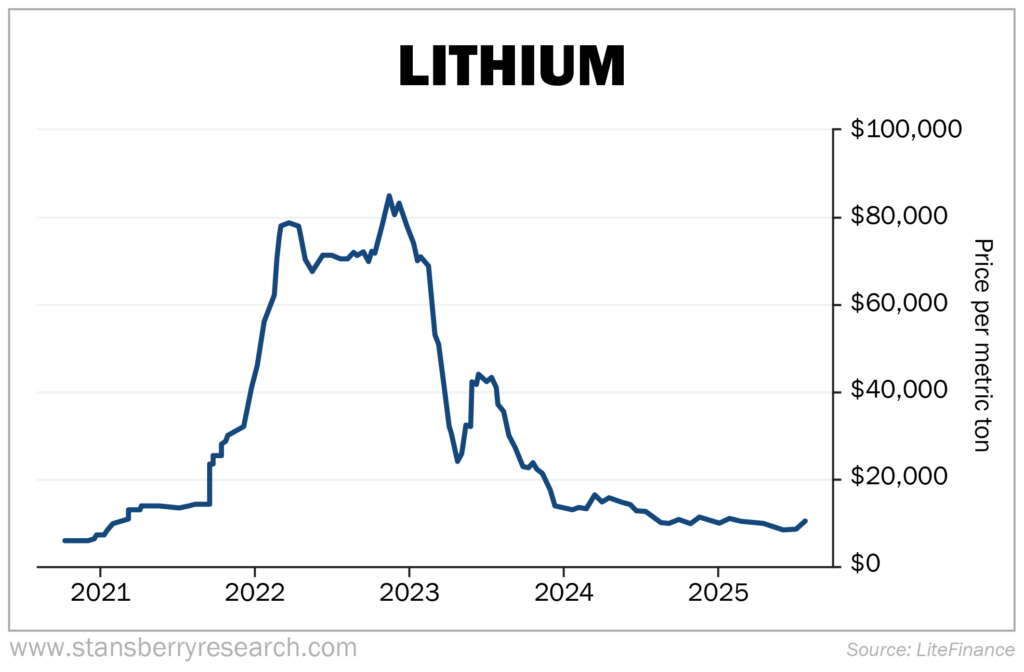

That volatility is why lithium mining is generally considered the riskiest part of the supply chain. Mining stocks are subject to significant peaks and valleys, something investors must consider. Just look at the roller coaster lithium prices have been riding since 2021.

What Investors Should Watch In 2026

In 1996, the U.S. Geological Survey’s (“USGS”) Mineral Commodity Summaries (“MCS”) proclaimed the United States as the world’s dominant producer of lithium.

How things have changed in 30 years.

Now, the U.S. imports more than half of the lithium it consumes, according to the USGS 2026 MCS.

Today, Chile owns the largest lithium reserves in the world, with roughly 9.3 million metric tons. Australia (7 million), Argentina (4 million), and China (3 million) are next on the list.

Australia is considered the world’s top producer of lithium, as most Australian lithium is extracted from hard-rock mines.

Mining companies are pushing to expand their access to lithium, however… particularly in North America. According to Market Data Forecast, North America has the highest growth rate in the lithium market, with an estimated compound annual growth rate (“CAGR”) of 25.5%.

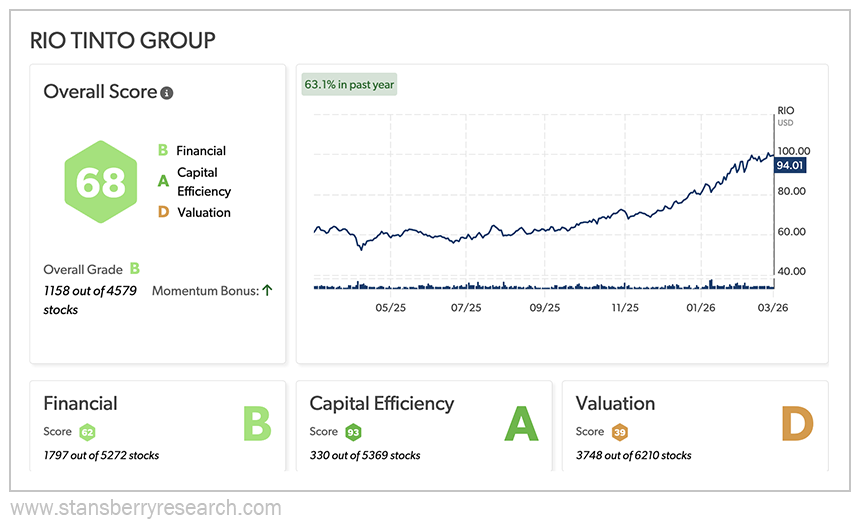

Top Stock to Watch: Rio Tinto (RIO)

Rio Tinto is a major global mining company focused on four core elements: iron ore, copper, aluminum, and lithium. As the company seeks to grow its lithium portfolio by more than 2.5 times by 2028, it’s looking at North America as a key area of expansion.

In March 2025, Rio Tinto acquired Arcadium Lithium for $6.7 billion. Through this acquisition, Rio Tinto also gained a 50% stake in Nemaska Lithium (the other 50% was controlled by the Quebec government).

In February, through equity investments made by Rio Tinto and the government of Quebec, Rio Tinto took over majority control of Nemaska. It’s also investing more than $300 million in Nemaska’s lithium projects to become a major EV battery player in North America.

Rio Tinto is also developing the Galaxy hard-rock lithium project in the James Bay region of Quebec. This endeavor aims to produce up to 40,000 metric tons of lithium carbonate equivalent in spodumene concentrate annually.

A look at Rio Tinto’s Stansberry Score (a tool that helps determine the quality and long-term value of thousands of stocks) shows solid overall performance for the stock, with a “B” grade.

Its Capital Efficiency is excellent (“A”) and its Financial grade is strong (“B”), evidenced by the company’s $16.8 billion operating cash flow and its reliability as a high-yield dividend stock (annual dividend of $4.00 per share).

A recent development worth monitoring… on February 5, Rio Tinto and Glencore, another global miner, walked away from a $260 billion merger that would have created the largest mining company in the world. We’ll see how Rio Tinto rebounds from that disappointing outcome.

Stage 2: Midstream – Refining Raw Lithium Into Battery Material

Next in the lithium supply chain is the refining stage. This occurs once refiners procure raw lithium from miners and process it into the finished material – lithium carbonate and lithium hydroxide – that battery manufacturers use.

As I mentioned, most lithium refining and processing occurs in China. And there is plenty of profit to be made by refining lithium. These companies’ profit models are driven by the high-demand, low-supply bottleneck.

This allows refiners to maximize their profit margins by charging a premium price on the finished products versus what they paid for the raw materials.

What Investors Should Watch In 2026

Lithium mining volume currently exceeds large-scale lithium refining, resulting in the critical supply chain bottleneck that comes from most raw lithium being sent to China for refining and processing.

As demand for lithium increases, it puts further pressure on the bottleneck. This is why some countries are aiming to create their own supply chains by both mining and refining lithium.

Australia, as the world’s leading lithium producer, has much to gain by refining the material domestically, rather than sending 98% of it to China.

The U.S. government is also pushing for more reliance on a domestic lithium supply chain. Last January, the U.S. Department of Energy (“DOE”) awarded Ioneer Rhyolite Ridge a nearly $1 billion loan guarantee to develop a lithium-carbonate processing facility in Nevada. This facility is expected to support the production of roughly 370,000 EV batteries a year.

The DOE also awarded a $225 million grant for Standard Lithium (SLI) and Equinor (EQNR) to build a lithium extraction and processing facility in the Smackover Formation – a source of lithium-rich brines – in southwestern Arkansas. This facility aims to produce 22,500 metric tons of battery-grade lithium carbonate per year starting in 2028.

Consistent global domestic lithium supplies would help stabilize the supply-demand imbalance. And that, theoretically, would dramatically reduce the lithium market’s volatility.

If more countries (besides China) can build domestic lithium supply chains, it could be a game changer.

Top Stock to Watch: Sociedad Química y Minera de Chile (SQM)

With an estimated 18% market share as of 2024, SQM is one of the world’s top producers of lithium. SQM extracts lithium from the Salar de Atacama salt flat and brine mine in Chile. With that lithium, SQM produces lithium carbonate and hydroxide for use in batteries.

Despite Chile’s vast lithium resources, SQM is expanding production beyond South America and into Australia and China.

For the first nine months of 2025, SQM reported $404.4 million in net income… a massive year-over-year rebound from its $524.5 million loss in 2024.

Total revenue dipped nearly 6% year over year to $3.25 billion. And gross profit dropped from roughly $1.03 billion in the first nine months of 2024 to just more than $904 million.

Despite the downturn in revenue and gross profit, SQM reached record lithium sales volume during the third quarter. It reported net income of $178.4 million for the period (a 36% year-over-year increase) and $1.17 billion in revenue (a roughly 9% year-over-year improvement).

SQM’s shares hit a 2025 high of $72.56 on December 26 (closing at $71.64). And by January 23, its price reached $86.00 (closing at $85.43). SQM, as of March 4, currently sits at around $72.00.

Its Stansberry Score is a solid “B,” with strong Capital Efficiency (“A”) and Financial (“B”) ratings.

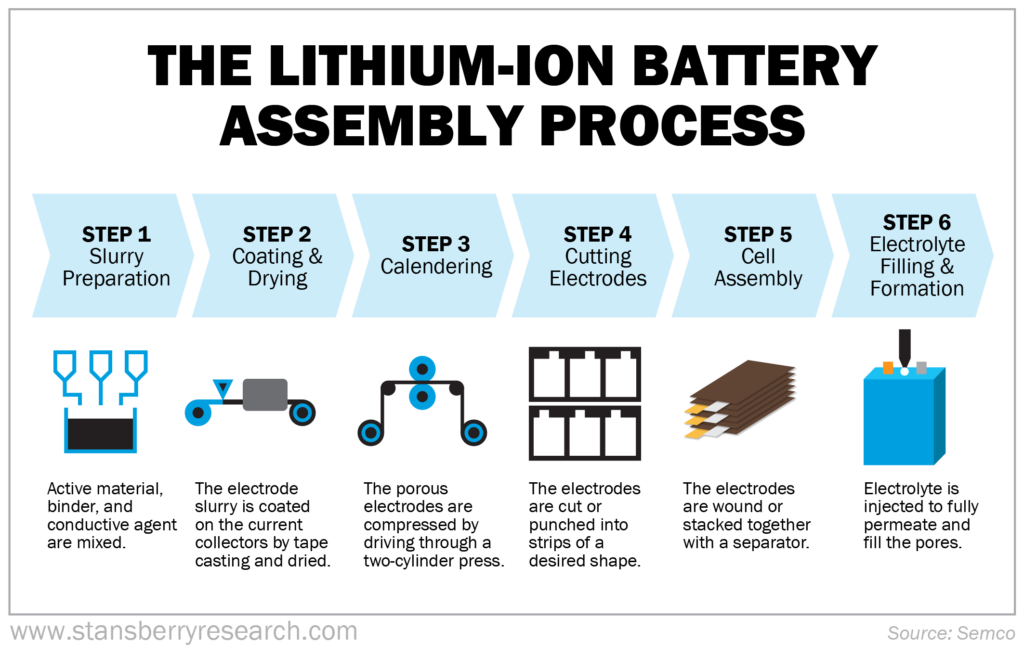

Stage 3: Downstream – Manufacturing and Assembling Batteries

With refined lithium in hand, battery manufacturers can begin the building process.

It’s very scientific and complicated, so we won’t get too into the weeds. Instead, we’ll let this chart explain the process.

The result is five types of lithium-ion batteries:

- Lithium cobalt oxide

- Lithium manganese oxide

- Lithium iron phosphate

- Lithium nickel cobalt manganese oxide

- Lithium nickel cobalt aluminum oxide

The battery manufacturers then sell their finished products to original equipment manufacturers (“OEMs”) in the automotive, energy storage, and electronics industries.

Most battery manufacturers rely on high-volume, long-term contract sales to OEMs as their primary revenue and profit source.

EV makers, energy storage providers, and consumer-electronics brands making smartphones, tablets, laptops, and other rechargeable devices are the most common buyers.

Between the price of materials and the process of manufacturing electrodes and finishing cells, the cost of making lithium-ion batteries is high. That makes volume and operational efficiency critical to a battery manufacturer’s bottom line.

What Investors Should Watch In 2026

The use of 4680 batteries is surging. These batteries, developed by Tesla (TSLA) in 2020, offer higher energy density, which translates to improved range for EVs. Tesla has been using 4680 batteries in its Model Y EVs on and off for four years and in its Cybertrucks since 2023.

Though Tesla was the first major adopter of this technology, competition has since become stiff. Other companies are now developing or manufacturing 4680-format battery cells, including Panasonic, LG Energy Solution, Samsung SDI, and CATL.

The battle for market share between these companies – and others – is worth monitoring.

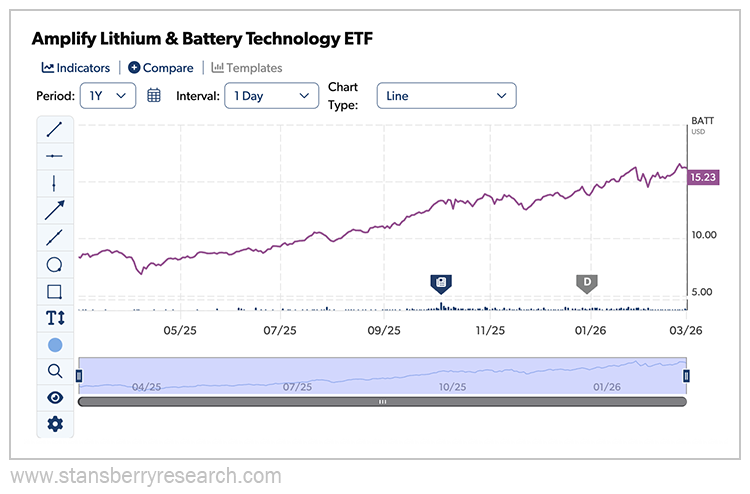

Top Stock to Watch: Amplify Lithium & Battery Technology Fund (BATT)

Because most lithium-ion batteries are made in China (more than 80%, according to the International Energy Agency), investing in the companies manufacturing these batteries can be challenging.

The Amplify Lithium & Battery Technology exchange-traded fund (“ETF”), however, provides an affordable opportunity for investors to get in on the lithium battery supply chain.

BATT’s portfolio of companies – which includes Tesla, BHP, Contemporary Amperex Technology, BYD, and TDK – generates revenue from the development, production, and use of lithium battery technology. This includes battery storage solutions, battery metals and materials, and EVs.

A look at BATT’s chart shows steady growth over the past year. Shares closed at $8.85 on February 26, 2025, and they closed at $16.56 on February 25 of this year.

Stage 4: End of Life – Recycling Used Lithium Batteries

The end of a lithium battery’s “life” isn’t necessarily its “death.” The battery lives on in the final stage of the lithium supply chain: the recycling of its materials.

Lithium battery recycling serves two purposes.

One, it reduces the number of improperly disposed batteries, which become hazardous waste.

Two, end-of-life lithium-ion batteries still hold valuable – and important – minerals needed to produce new batteries. Recycled batteries are shredded, screened, and treated to reclaim what’s left of their lithium, cobalt, and nickel. And that helps reduce the need for new raw materials.

Battery recyclers make their money by selling those recovered materials back into the supply chain. They obtain the various minerals through what is known as black mass production. Black mass, according to Green Li-ion, is a “dark, granular material that remains after lithium-ion batteries are shredded during recycling. It contains a valuable mix of metals, including: lithium, cobalt, nickel, manganese, [and] graphite.” Instead of sourcing new raw materials, manufacturers can use black mass as a faster, cleaner, and cost-effective supply source.

Another revenue source for battery recyclers is the significant fees they charge electronics manufacturers and EV companies to take their spent battery packs and dispose of them properly.

These fees vary widely, but lithium cobalt oxide (smartphones, tablets, laptops), lithium nickel manganese cobalt oxide (EVs, grid storage), and lithium nickel cobalt aluminum oxide (Tesla EVs, industrial equipment) batteries have the highest recycling values.

Battery recyclers also bring in revenue from government subsidies, compliance credits, and various incentives. These include tax credits, grants, loans, and even direct-to-consumer incentives, which bring more batteries to recycling businesses.

What Investors Should Watch In 2026

Three words: Electric. Vehicle. Batteries.

It’s simple… As more EV batteries are produced, more will require recycling. And with EV adoption rates surging, battery recycling companies are anticipating a major influx of EV batteries as they reach the end of their lives in the coming months and years.

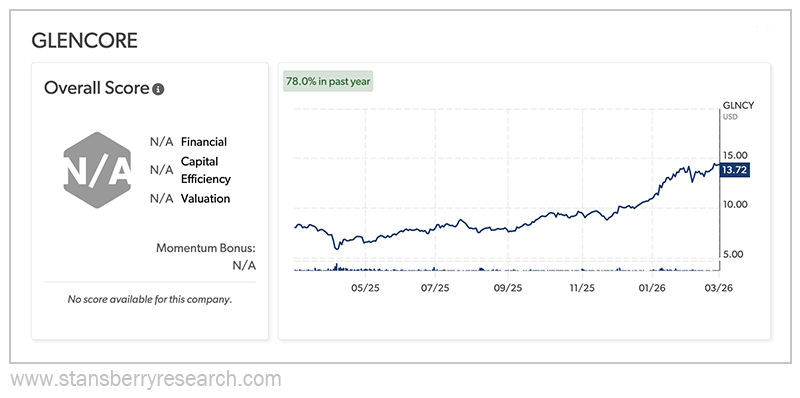

Top Stock to Watch: Glencore (GLNCY)

Switzerland-based Glencore is one of the world’s largest natural resource companies. It produces, processes, distributes, and markets more than 60 commodities, including metals and energy products.

But a growing piece of Glencore’s business is its end-of-life lithium-ion battery and electronics recycling segment. It sources recyclable materials from OEMs and processors and markets the recovered materials directly to its industrial customers.

In 2025, Glencore acquired Canadian battery recycler Li-Cycle Holdings for $43.6 million. This strategic maneuver strengthened Glencore’s position in the lithium-ion battery recycling sector.

Glencore had a mixed 2025 fiscal year. Highlights included a 7% year-over-year revenue increase to $247.5 billion, and a huge rebound in net income – from a roughly $1.6 billion loss in 2024 to a positive $363 million in 2025. It did see a drop in adjusted EBITDA, however, down 6% to $13.5 billion.

Back to the aborted Rio Tinto/Glencore merger… Glencore shares plunged as much as 10.8% once the failed merger was reported.

Glencore was this close to being half of the world’s largest mining company. Now it’s left to build a multibillion-dollar copper mine on its own and manage its dependence on the coal industry.

Both issues would have been remedied by the merger. So, we’ll see how the company responds to the development.

Glencore stock has grown at a modest rate over the past year, with its share price at roughly $8 last February 26 and its price as of February 25 at $14.48.

Risks Lithium Investors Should Consider

Here’s a high-level look at the potential risks of investing in lithium.

- Price volatility:Remember, lithium is a commodity, and commodity stocks are highly volatile. This is primarily due to geopolitical events, supply-demand imbalances, and climate-related factors. We’ve already seen sharp price swings this year. But that’s par for the course with lithium.

- Oversupply: Rapid lithium supply increases in China, Africa, and Australia contributed to an oversupply in 2025, a historically difficult year for the lithium industry. Prices of lithium carbonate in North Asia dropped to four-year lows as a result. But lithium rebounded near the end of 2025. And the risk of oversupply in 2026 isn’t nearly as significant thanks to improved supply discipline and the growing demand for energy storage systems and EVs.

- Supply chain and policy: With most lithium processing happening, American battery companies and companies that import batteries for their products are fully exposed to the impacts of trade policy changes and export rules. President Donald Trump’s tariffs, for example, sent costs soaring for lithium batteries coming from China. By August of last year, the combined tariff rate for EV batteries increased from 7.5% to 58%, with some analysts predicting EV battery tariffs could reach 173% and non-EV battery tariffs might hit 156%.

The lithium battery industry got a very brief reprieve on February 20, when the U.S. Supreme Court overturned Trump’s use of the International Emergency Economic Powers Act to impose his tariffs. The battery industry celebrated the news and was poised to seek refunds on an estimated $133.5 billion it collectively paid in duties. Then, just a few days later, Trump announced he would impose a new worldwide tariff of 15% to reinstate a portion of what the Supreme Court had previously overturned.

It’s these types of events that bear watching throughout the year.

Positioning for the Next Phase of the Lithium Cycle

This year could be a big one for lithium. It’s already showing signs of rebounding from a challenging 2025, and demand continues to grow for lithium batteries.

Lithium presents investors with a wide range of investment opportunities. Each stage of the supply chain – from mining to recycling – comes with its own risks and rewards, so it’s important to approach lithium investing with that knowledge.

If you’re considering investing in lithium, think strategically about which link of the supply chain best matches your investment goals and risk tolerance. No matter where on the supply chain you land, lithium investing appears primed to pay off in the long run.

Regards,

David Engle

Editor’s note: Rare earths and other critical mineral stocks have exploded – you could have doubled your money 28 different times in 2025.

But now the man ranked in 2020 as America’s No. 1 stock picker says the White House is set to buy a whole new group of stocks in the biggest government buying spree in history.

Here’s the name and ticker of every stock that could be next.